Thị trường giao đồ ăn tại Việt Nam đã đạt đến bước ngoặt vào năm 2025, hướng tới cuộc cạnh tranh khốc liệt về chất lượng dịch vụ và hiệu quả.

13/01/2026

Tin tức & Báo cáo mới nhất / Vietnam Briefing

Bình luận: Không có bình luận.

Thị trường giao đồ ăn Việt Nam đã đạt đến bước ngoặt vào năm 2025 khi cục diện trở nên tập trung hơn sau sự rút lui của Gojek. Trong khi GrabFood và ShopeeFood hiện đang dẫn đầu, những gương mặt mới như Xanh SM Ngon đang chuyển trọng tâm cạnh tranh từ việc giảm giá đơn thuần sang tốc độ và độ tin cậy trong hoạt động. Bất chấp nhu cầu ngày càng tăng, các nhà hàng đang phải đối mặt với áp lực ngày càng lớn từ phí dịch vụ và chi phí quảng cáo, ngay cả khi các mô hình sử dụng khác biệt rõ rệt xuất hiện giữa Hà Nội và Thành phố Hồ Chí Minh. Cuối cùng, thị trường đã vượt ra khỏi sự mở rộng đơn thuần để trở thành một cuộc chiến khốc liệt về chất lượng dịch vụ và hiệu quả.

Tổng quan thị trường

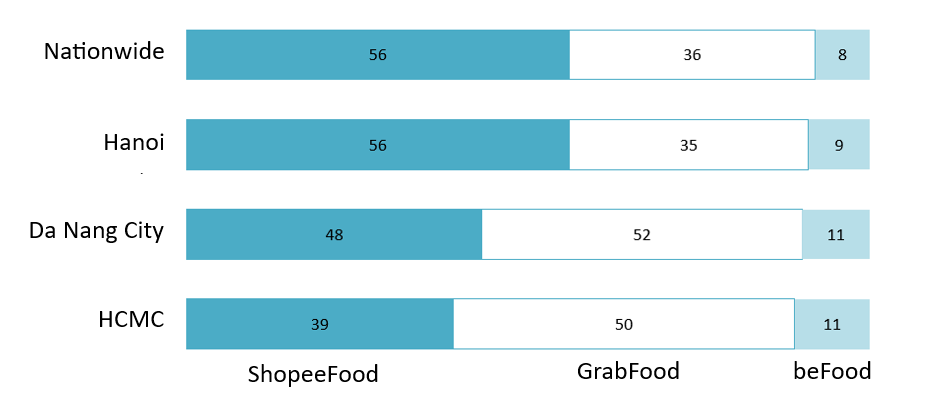

Theo ước tính của Statista và VECOM, doanh thu thị trường giao đồ ăn tại Việt Nam năm 2025 đạt gần 3 tỷ USD, tăng khoảng 151 tỷ 3 nghìn tỷ USD so với năm 2024.[1] Lĩnh vực này cũng được định hình bởi sự phân hóa rõ rệt theo khu vực, với vị trí dẫn đầu thị trường thay đổi dựa trên văn hóa và logistics địa phương. Theo khảo sát tháng 4 năm 2025, tại Hà Nội, ShopeeFood duy trì thị phần thống trị với 56%. Ngược lại, GrabFood dẫn đầu tại Thành phố Hồ Chí Minh với khoảng 50% thị phần, nơi đội ngũ tài xế khổng lồ và thuật toán vượt trội đáp ứng nhịp sống nhanh hơn của thành phố phía Nam. BeFood cũng đạt hiệu suất mạnh nhất tại Thành phố Hồ Chí Minh, với 11% thị phần so với 9% tại Hà Nội.[2].

Vietnam’s online food delivery market in April 2025

Đơn vị: % số người trả lời

Nguồn: NielsenIQ, Decision Lab

Theo đại diện ShopeeFood Việt Nam, số lượng đơn hàng trong quý 3 năm 2025 đã tăng hơn 301 tỷ TP3T so với cùng kỳ năm ngoái, với nhu cầu cao nhất đến từ nhân viên văn phòng và sinh viên. Đặc biệt, ShopeeFood thu hút mạnh mẽ thế hệ Z (16-24 tuổi), tận dụng lợi thế tích hợp với hệ sinh thái Shopee rộng lớn hơn và các chương trình giảm giá mạnh mẽ để trở thành lựa chọn mặc định cho các dịp “ăn vặt” như trà sữa trân châu và đồ ăn đường phố. Ngược lại, GrabFood lại chiếm ưu thế trong nhóm người làm việc chuyên nghiệp lớn tuổi (35+) và các gia đình, phân khúc tạo ra giá trị đơn hàng trung bình (AOV) cao hơn thông qua các đơn hàng trọn bữa.3Đối với những người dùng này, độ tin cậy của dịch vụ và tốc độ giao hàng được ưu tiên hơn so với sự nhạy cảm về giá cả.

Xu hướng thị trường

Thị trường giao đồ ăn tại Việt Nam đang bước vào giai đoạn hợp nhất rõ rệt hơn. Việc Gojek rút khỏi thị trường vào tháng 9 năm 2024 đã làm giảm số lượng các đối thủ cạnh tranh quy mô lớn, đẩy thị trường hướng tới cấu trúc tập trung hơn vào năm 2025. Với số lượng các ông lớn giảm đi, cạnh tranh ngày càng được định hình bởi khả năng duy trì quy mô và củng cố vị thế, thay vì chỉ đơn thuần mở rộng sự hiện diện.

Bất chấp sự chuyển đổi cấu trúc này, sự tăng trưởng của dịch vụ giao đồ ăn vẫn chủ yếu dựa vào các chương trình khuyến mãi, và tình hình kinh tế ngày càng trở nên khó khăn hơn đối với cả nền tảng và nhà hàng. Giảm giá và miễn phí vận chuyển tiếp tục đóng vai trò trung tâm trong việc thúc đẩy số lượng đơn đặt hàng, và các nền tảng không muốn cắt giảm các ưu đãi vì người dùng có thể chuyển đổi ứng dụng một cách dễ dàng. Do đó, các chương trình khuyến mãi vẫn là đòn bẩy quan trọng đối với nhu cầu ngay cả khi áp lực lợi nhuận ngày càng gia tăng.

Về phía người bán, chi phí liên quan đến nền tảng có thể tăng lên nhanh chóng. Các nhà hàng thường phải trả hoa hồng khoảng 251 TP3T, cộng thêm thuế, và thường chi thêm 10–151 TP3T doanh thu cho quảng cáo trong ứng dụng để duy trì sự hiện diện—đôi khi thậm chí lên đến 10–201 TP3T trong các lĩnh vực cạnh tranh hơn. Trong một số trường hợp, khi kết hợp phí, quảng cáo và tham gia các chương trình giảm giá, tổng gánh nặng liên quan đến nền tảng có thể lên tới khoảng 40–451 TP3T doanh thu. Điều này tạo ra tình huống người bán có thể xử lý nhiều đơn hàng hơn nhưng lại giữ lại lợi nhuận ít hơn đáng kể.

Những áp lực này đang buộc nhiều nhà hàng phải điều chỉnh chiến lược hoạt động của mình. Một số tăng giá thực đơn để bù đắp chi phí tăng cao, trong khi những nhà hàng khác ưu tiên các mặt hàng có lợi nhuận cao hơn như đồ uống và đồ ăn nhẹ để bảo vệ khả năng sinh lời. Đồng thời, ngày càng nhiều nhà bán lẻ đang cố gắng xây dựng các kênh bán hàng trực tiếp cho khách hàng để giảm sự phụ thuộc vào quảng cáo trả phí trong ứng dụng và giành lại quyền kiểm soát mối quan hệ với khách hàng.

Trong khi đó, cuộc cạnh tranh đang chuyển dịch từ cuộc chiến giá cả thuần túy sang chất lượng dịch vụ và tốc độ giao hàng. Một cuộc khảo sát quý 1 năm 2025 trên khắp các thành phố lớn của Việt Nam cho thấy chỉ có 261.000 người dùng lựa chọn ứng dụng chủ yếu dựa trên giá thấp. Thay vào đó, gần một nửa số khách hàng (471.000 người dùng) ưu tiên giao hàng nhanh, và 411.000 người dùng tập trung vào tính chuyên nghiệp của tài xế và độ chính xác của đơn hàng. Điều này cho thấy giá rẻ nhất không còn đủ để thu hút người dùng đô thị, vì độ tin cậy và tốc độ ngày càng định hình giá trị cảm nhận.

Để đáp ứng điều này, các nền tảng đang định hình lại hoạt động nhằm đáp ứng kỳ vọng dịch vụ cao hơn. Ví dụ, Xanh SM Ngon tạo sự khác biệt bằng cách cam kết không gộp đơn hàng, nhằm giữ cho món ăn luôn nóng và giảm thiểu sai sót khi giao hàng thông qua phương pháp một người giao một đơn hàng. Tương tự, GrabFood đang tận dụng trí tuệ nhân tạo (AI) để dự báo nhu cầu và thử nghiệm các mô hình giao hàng mới nhằm giảm thời gian giao hàng trung bình xuống khoảng 20 phút, đặc biệt là vào giờ cao điểm buổi sáng và buổi tối.

Người chơi chính

Đến giữa năm 2025, thị trường giao đồ ăn tại Việt Nam bị chi phối bởi ba tên tuổi chính: ShopeeFood, GrabFood và BeFood. Với hai công ty dẫn đầu (ShopeeFood và GrabFood) kiểm soát hơn 901.300 tỷ USD thị trường, lĩnh vực này hiện đang có mức độ tập trung cao. Thêm vào đó, Xanh SM Ngon chính thức ra mắt dịch vụ giao đồ ăn tại TP. Hồ Chí Minh vào ngày 23 tháng 7 năm 2025, với chính sách không gom đơn hàng, một tính năng khác biệt quan trọng được thiết kế để mang lại trải nghiệm khách hàng tối ưu.

Ứng dụng giao đồ ăn tại Việt Nam

| STT | Thương hiệu | Quốc gia | Nhập cảnh Việt Nam | Mô tả ngắn gọn |

| 1 | ShopeeFood | Singapore | 2015 | ShopeeFood, nền tảng giao đồ ăn trước đây có tên là “Now”, được tích hợp trực tiếp vào hệ sinh thái thương mại điện tử của Shopee. |

| 2 | GrabFood | Malaysia | 2018 | Một dịch vụ giao đồ ăn nằm trong ứng dụng đa dịch vụ Grab, tập trung vào công nghệ điều phối tài xế tối ưu và mạng lưới đối tác nhà hàng rộng khắp. |

| 3 | BeFood | Việt Nam | 2022 | Dịch vụ giao đồ ăn của ứng dụng gọi xe “Be” tại Việt Nam tập trung vào trải nghiệm thân thiện với người dùng và giá cả cạnh tranh cho khách hàng. |

| 4 | Xanh SM Ngon | Việt Nam | 2025 | Một đơn vị mới gia nhập thị trường giao đồ ăn bằng GSM, hoạt động trên nền tảng xe điện thân thiện với môi trường 100%. |

Nguồn: Tổng hợp của B&Company

Ý nghĩa

Thị trường giao đồ ăn tại Việt Nam tiếp tục tiềm ẩn nhiều rủi ro tăng trưởng, nhưng bản chất của cơ hội đang thay đổi. Khi thị trường ngày càng tập trung vào một số ít nền tảng quy mô lớn, cạnh tranh ngày càng được định hình bởi chiều sâu của hệ sinh thái (nguồn cung nhà cung cấp, năng lực hậu cần, khả năng giữ chân người dùng và tính nhất quán của dịch vụ). Đối với các doanh nghiệp mới tham gia và các doanh nghiệp hỗ trợ, điều này không tự động dẫn đến việc gia nhập dễ dàng hơn; thay vào đó, nó cho thấy rằng thành công sẽ dễ đạt được hơn khi các sản phẩm/dịch vụ bổ sung cho các nền tảng hiện có hoặc giải quyết các điểm nghẽn cụ thể trong chuỗi giá trị, thay vì cố gắng sao chép hoàn toàn các mô hình thị trường quy mô lớn.

Trong bối cảnh này, một số lĩnh vực cơ hội vẫn khả thi. Việc hỗ trợ các nhà bán lẻ—chẳng hạn như cung cấp các công cụ tốt hơn để quản lý thực đơn, dự báo nhu cầu và quản lý quan hệ khách hàng—có thể giúp các nhà hàng hoạt động hiệu quả hơn trong bối cảnh chi phí liên quan đến nền tảng ngày càng tăng. Bao bì và bảo quản chất lượng thực phẩm (ví dụ: giữ nhiệt và ngăn ngừa tràn đổ) cũng có thể trở nên quan trọng hơn khi người tiêu dùng đặt trọng tâm lớn hơn vào độ tin cậy của dịch vụ giao hàng. Song song đó, đổi mới trong lĩnh vực hậu cần (tối ưu hóa tuyến đường, quy tắc gom hàng và dự đoán nhu cầu) có thể tạo ra cơ hội cho các nhà cung cấp dịch vụ cải thiện tốc độ và độ chính xác mà không cần chỉ dựa vào các khoản trợ cấp lớn hơn.

Đồng thời, thị trường đang bước vào giai đoạn hạn chế về tài chính hơn. Khuyến mãi vẫn là động lực chính thúc đẩy đơn đặt hàng, và các nền tảng phải đối mặt với sự đánh đổi giữa việc duy trì khối lượng đơn hàng và cải thiện hiệu quả kinh tế trên mỗi đơn vị sản phẩm. Trong khi đó, các nhà hàng tiếp tục phải gánh chịu một loạt chi phí liên quan đến nền tảng—hoa hồng, thuế và nhu cầu quảng cáo trả phí trong ứng dụng để đảm bảo khả năng hiển thị—thường bị cộng thêm bởi việc tham gia các chiến dịch giảm giá. Tình trạng này có thể dẫn đến khối lượng đơn hàng cao hơn nhưng lợi nhuận thấp hơn đối với các nhà bán lẻ, điều này có thể ảnh hưởng đến sự sẵn lòng phụ thuộc nhiều vào các kênh nền tảng trong dài hạn và có thể làm tăng rủi ro mất khách hàng ở phía cung ứng.

* Nếu bạn muốn trích dẫn bất kỳ thông tin nào từ bài viết này, vui lòng ghi rõ nguồn và cung cấp liên kết đến bài viết gốc để tôn trọng bản quyền.

| Công ty B&Company

Là công ty Nhật Bản đầu tiên chuyên về nghiên cứu thị trường tại Việt Nam từ năm 2008. Chúng tôi cung cấp nhiều dịch vụ đa dạng bao gồm báo cáo ngành, phỏng vấn ngành, khảo sát người tiêu dùng, kết nối kinh doanh. Ngoài ra, gần đây chúng tôi đã xây dựng cơ sở dữ liệu hơn 900.000 công ty tại Việt Nam, có thể được sử dụng để tìm kiếm đối tác và phân tích thị trường. Vui lòng liên hệ với chúng tôi nếu bạn có bất kỳ thắc mắc nào. info@b-company.jp + (84) 28 3910 3913 |

[1] https://thoibaonganhang.vn/mua-sam-va-dat-do-an-online-bung-no-thoi-quen-tieu-dung-so-nam-2025-173233.html

[2] https://dtinews.dantri.com.vn/vietnam-today/vietnams-food-delivery-market-booms-20250710142707966.htm

Bài viết liên quan

ĐĂNG KÝ NHẬN BẢN TIN