ベトナムのフードデリバリー市場は2025年に転換点を迎え、サービスの質と効率をめぐる激しい戦いへと向かっている。

2026年1月13日

最新ニュースとレポート / ベトナムブリーフィング

コメント: コメントはまだありません.

ベトナムのフードデリバリー市場は、Gojekの撤退に伴い市場の集中化が進んだことで、2025年に転換期を迎えました。GrabFoodとShopeeFoodが市場を牽引する一方で、Xanh SM Ngonのような新規参入企業は、競争の軸を単なる値引きではなく、運営のスピードと信頼性へと移行させています。需要の増加にもかかわらず、レストランは手数料と広告費の高騰によるプレッシャーに直面しており、ハノイとホーチミン市では利用パターンに明確な違いが見られます。最終的に、市場は単なる拡大の域を超え、サービスの質と効率性をめぐる熾烈な競争へと移行しました。

市場概況

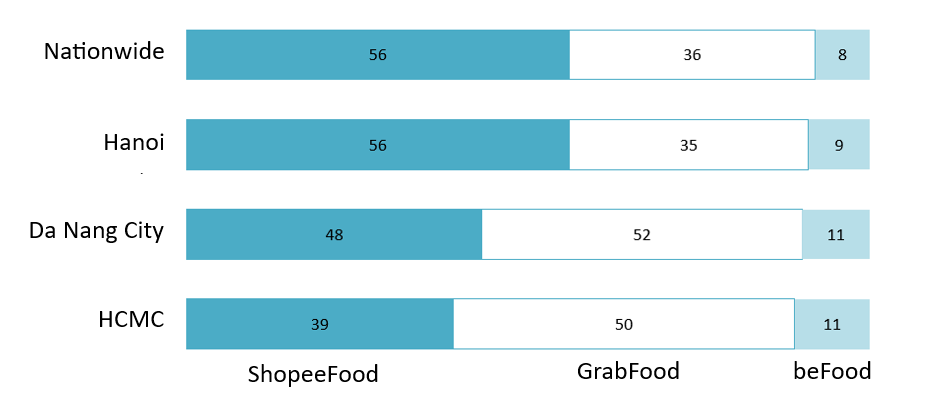

StatistaとVECOMの推計によると、ベトナムの食品配達市場の収益は2025年に約30億米ドルに達し、2024年と比較して約15%増加することになります。[1] このセクターは地域によって大きく二分されており、市場のリーダーシップは地域の文化や物流によって変化しています。2025年4月の調査によると、ハノイではShopeeFoodが56%の圧倒的な市場シェアを維持しています。一方、ホーチミン市ではGrabFoodが約50%の市場シェアでトップに立ち、大規模なドライバー群と優れたアルゴリズムによって、南部の大都市の速いペースに対応しています。BeFoodもホーチミン市で最も好調な業績を上げ、シェアは11%で、ハノイの9%を大きく上回りました。[2].

Vietnam’s online food delivery market in April 2025

単位:%の回答者

出典: NielsenIQ、Decision Lab

ShopeeFoodベトナムの担当者によると、2025年第3四半期の注文数は前年比で30%以上増加し、最も需要が高かったのはオフィスワーカーと学生だった。特にShopeeFoodは、Shopeeエコシステムとの統合と積極的な値引きにより、Z世代(16~24歳)に強く支持されており、タピオカティーや屋台料理といった「軽食」の定番として定着している。一方、GrabFoodは、35歳以上のシニア層やファミリー層を中心として、フルミール注文で高い平均注文額(AOV)を生み出している。3これらのユーザーにとって、サービスの信頼性と配信速度は価格に対する敏感さよりも優先されます。

市場動向

ベトナムのフードデリバリー市場は、より明確な統合の段階に入りつつあります。2024年9月のGojekの撤退により、規模の大きな競合企業の数は減少し、2025年には市場はより集中化した構造へと移行するでしょう。大手企業の減少に伴い、競争は単にプレゼンスを拡大するのではなく、規模を維持し、顧客維持を強化できる企業が優位に立つことがますます重要になります。

こうした構造変化にもかかわらず、フードデリバリーの成長は依然としてプロモーションに大きく依存しており、プラットフォームとレストラン双方にとって経済状況は逼迫しています。割引や送料無料は依然として注文量の増加に中心的な役割を果たしており、ユーザーがアプリを乗り換える際の煩わしさを最小限に抑えられるため、プラットフォーム側はインセンティブの縮小に消極的です。その結果、収益性へのプレッシャーが強まる中でも、プロモーションは依然として需要喚起の重要な手段となっています。

加盟店側では、プラットフォーム関連のコストが急速に積み上がる可能性があります。レストランは、通常約251兆円の手数料に加え、税金を負担することになります。さらに、視認性を維持するために、収益の10~151兆円をアプリ内広告に費やしているのが一般的で、競争の激しいカテゴリーでは10~201兆円に達することもあります。場合によっては、手数料、広告、割引プログラムへの参加などを合わせると、プラットフォーム関連の負担総額は収益の約40~451兆円に達することもあります。その結果、加盟店はより多くの注文を処理できる一方で、利益は大幅に減少するという状況が生じます。

こうしたプレッシャーにより、多くのレストランは運営戦略の調整を迫られています。コスト上昇を相殺するためにメニュー価格を上げる店もあれば、利益率を維持するためにドリンクやスナックといった利益率の高い商品を優先する店もあります。同時に、有料アプリ内広告への依存を減らし、顧客関係をある程度コントロールするために、顧客に直接販売するチャネルの構築を試みる小売業者も増えています。

一方、競争の舞台は純粋な価格競争から、サービスの質と配送速度へと移行しつつあります。2025年第1四半期にベトナムの主要都市で実施された調査によると、低価格を主な理由としてアプリを選んだユーザーはわずか26%でした。一方、顧客のほぼ半数(47%)は迅速な配送を重視し、41%はドライバーの専門性と注文の正確性を重視しています。これは、信頼性とスピードがますます価値を形作るようになり、都市部のユーザーを獲得するには最安価格だけではもはや十分ではないことを示しています。

これを受けて、プラットフォームはより高いサービスへの期待に応えるために業務を再構築しています。例えば、Xanh SM Ngonは、注文をまとめないことを約束することで差別化を図り、料理を温かい状態に保ち、1人の乗客1注文のアプローチで配達ミスを最小限に抑えることを目指しています。同様に、GrabFoodはAIを活用して需要を予測し、特に朝晩のピーク時における平均配達時間を約20分に短縮するための新しい配達モデルをテストしています。

主な登場人物

2025年半ばまでに、ベトナムのフードデリバリー市場はShopeeFood、GrabFood、BeFoodの3社によって独占状態となりました。ShopeeFoodとGrabFoodの2社が市場の90%以上を掌握しているため、このセクターは高度に集中化しています。さらに、Xanh SM Ngonは2025年7月23日にホーチミン市でフードデリバリーサービスを正式に開始しました。このサービスは、最適な顧客体験を提供するために設計された重要な差別化要素である、注文の一括処理をしないポリシーを特徴としています。

ベトナムのフードデリバリーアプリ

| ブランド | 国 | ベトナム入国 | 簡単な説明 | |

| 1 | ショップフード | シンガポール | 2015 | 以前は「Now」として知られていた食品配達プラットフォームであるShopeeFoodは、Shopee eコマースエコシステムに直接統合されています。 |

| 2 | グラブフード | マレーシア | 2018 | Grab マルチサービス スーパーアプリ内の食品配達サービス。最適化されたドライバー配車テクノロジーとレストラン パートナーの広範なネットワークに重点を置いています。 |

| 3 | ビーフード | Vietnam | 2022 | ベトナムの配車アプリ「Be」の食品配達部門は、顧客にとって使いやすい体験と競争力のある価格設定に重点を置いています。 |

| 4 | ザン・SM・ンゴン | Vietnam | 2025 | GSM による食品配達部門の新規プレーヤー。環境に優しい 100% 電気自動車プラットフォームで運営されています。 |

出典: B&Companyの編集

意味合い

ベトナムのフードデリバリー市場は依然として成長の可能性を秘めていますが、その機会の性質は変化しています。市場が少数の小規模プラットフォームに集中するにつれ、競争はエコシステムの深さ(加盟店の供給、物流能力、ユーザー維持率、サービスの一貫性)によってますます左右されるようになっています。新規参入企業や関連企業にとって、これは必ずしも参入を容易にするものではありません。むしろ、本格的なマーケットプレイスモデルを模倣するのではなく、既存のプラットフォームを補完したり、バリューチェーンの特定のボトルネックを解消したりするサービスの方が成功の可能性が高くなることを示唆しています。

このような状況下において、依然としていくつかの機会領域が存在します。メニュー管理、需要予測、顧客関係管理のためのツール強化といったマーチャント支援は、プラットフォーム関連コストの上昇下でも、レストランの効率的な運営に役立ちます。消費者が配達の信頼性を重視するようになるにつれ、包装や食品の品質保持(例:温度保持やこぼれ防止)も重要性を増すでしょう。同時に、物流のイノベーション(ルート最適化、バッチルール、需要予測)は、より多額の補助金に頼ることなく、スピードと精度を向上させるサービスプロバイダーにとって、新たな機会を生み出す可能性があります。

同時に、市場はより財政的に厳しい局面に入りつつあります。プロモーションは依然として注文獲得の大きな原動力であり、プラットフォームは数量の維持とユニットエコノミクスの向上の間でトレードオフを迫られています。一方、レストランはプラットフォーム関連のコスト(手数料、税金、露出を確保するための有料アプリ内広告など)を負担し続けており、割引キャンペーンへの参加もそのコストを上乗せしています。こうした状況は、注文量は増加するものの、小売業者の収益性は低下する可能性があり、プラットフォームチャネルへの長期的な依存度に影響を与え、供給側の顧客離れリスクを高める可能性があります。

* この記事の情報を引用する場合は、著作権を尊重するため、出典と元の記事へのリンクを明記してください。.

| B&カンパニー

2008年よりベトナムで市場調査を専門とする初の日本企業として、業界レポート、業界インタビュー、消費者調査、ビジネスマッチングなど、幅広いサービスを提供しています。さらに、ベトナム国内の90万社以上の企業を網羅したデータベースを構築し、パートナー企業の探索や市場分析にご活用いただけるようになりました。. ご不明な点がございましたら、お気軽にお問い合わせください。. info@b-company.jp + (84) 28 3910 3913 |

[1] https://thoibaonganhang.vn/mua-sam-va-dat-do-an-online-bung-no-thoi-quen-tieu-dung-so-nam-2025-173233.html

[2] https://dtinews.dantri.com.vn/vietnam-today/vietnams-food-delivery-market-booms-20250710142707966.htm

関連記事

ニュースレターを購読する