In the largest F&B market of Vietnam - Ho Chi Minh City, the retail stock reached a record 1.2 million square meters (+6.26% YoY).

273월2026

최신 뉴스 및 보고서 / 베트남 브리핑

댓글: 댓글 없음.

추상적인

In Vietnam’s largest F&B market – Ho Chi Minh City, the retail stock reached a record 1.2 million sqm (+6.26% YoY), yet over 11% of F&B outlets closed in H1 2025, signaling a market shakeout that is cutting weak operators and sharpening competition. Rental prices span a huge range — USD 80–150/sqm/month in District 1 down to USD 15–35/sqm/month in the outer belt — while Thu Duc City, anchored by Metro Line 1 and nearly 60 thousand daily riders, is redefining the city’s F&B geography eastward. The Special Consumption Tax on sugary beverages (effective January 1, 2026) adds a structural cost headwind, particularly for beverage-heavy formats. In this environment, location precision is one of the main criteria that determines profitability.

HCM Retail Leasing Market: Structure and City-Level Benchmarks

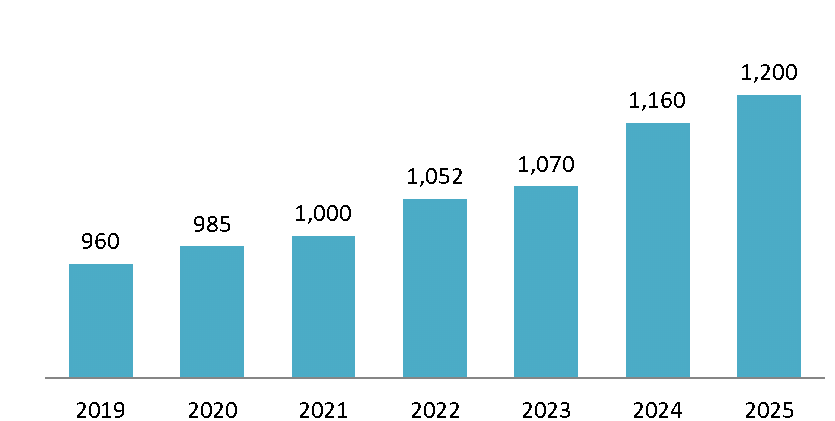

HCMC’s retail market has undergone significant structural expansion over the past decade. As of Q2 2025, the city’s total accumulated retail stock reached 1.2 million sqm — a 6.26% increase year-on-year — with an overall occupancy rate of 93.6%, among the highest recorded across Southeast Asian tier-1 cities [2]. This combination of growing supply and sustained high occupancy reflects the depth of retail demand in HCMC, driven by robust household consumption, inbound tourism recovery, and accelerating urbanization in the outer districts.

Total Accumulated Retail Stock of HCMC (million sqm)

Source: JLL Vietnam, Cushman & Wakefield

At the city-wide level, average asking rents for retail space stood at approximately USD 53.36 per sqm per month in Q2 2025 [2]. However, this blended average conceals sharp spatial divergence. By the end of 2024, HCMC’s City Centre retail segment was projected to reach a net rent of USD 84.5 per sqm per month, while the City Fringe stood at USD 38.4 per sqm per month [3] — a more than twofold difference that reflects the city’s steep spatial pricing gradient. Prime mall space in District 1’s flagship properties commands base rents well above USD 80 per sqm per month, while outer-belt districts such as Tan Phu and Go Vap offer street-level F&B space at USD 15–35 per sqm per month. This pricing bifurcation creates genuinely distinct market tiers for F&B operators at different capital scales and brand positioning levels.

Market Shakeout: A Selective, High-Stakes Environment

Despite the positive supply and occupancy indicators, the operating environment for F&B businesses in HCMC is increasingly demanding. In H1 2025, due to the rising input costs (cited by 35.4% of operators) and new tax policies, including the SCT (21%), with rent inflation ranking fourth at 13.7% [14], F&B outlet counts in HCMC declined by over 11% compared to the same period in 2024 [7]. This fact suggests the shakeout reflects a broad margin compression across the sector rather than a rent-led correction alone, eliminating undercapitalized or poorly located operators. Rather than signalling a structural collapse, this correction is resetting the market toward quality and capital efficiency. For well-resourced new entrants, the shakeout is an opportunity: it reduces competition for prime locations, compresses lease negotiation timelines, and creates a cleaner consumer landscape. This context makes a precise understanding of the rental price map — and the district-level demand fundamentals behind it — more valuable than at any previous point in HCMC’s F&B history.

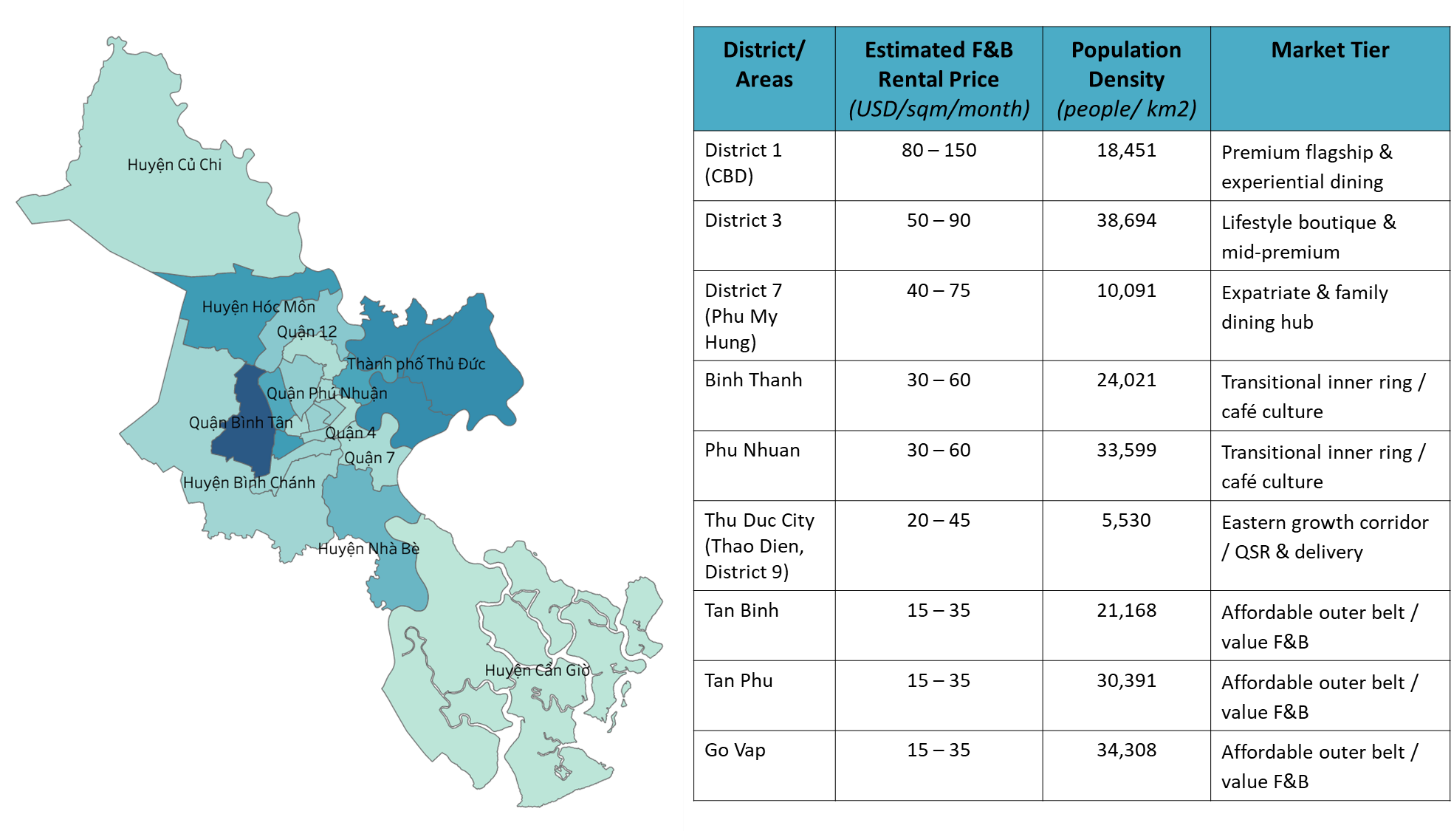

Estimated Retail Leasing Price Ranges by District

The table below summarizes estimated ground-floor F&B rental ranges across HCMC’s key districts and submarkets in 2025–2026, based on available market data from institutional brokers, listing platforms, and published retail reports [2][3][4].

Source: Cushman & Wakefield, Real Estate Asia

District 1 – The Premium CBD Core: District 1 remains HCMC’s most expensive and most visible retail submarket. Along the Dong Khoi, Nguyen Hue, and Le Loi corridors — where tourist footfall intersects with luxury residential and office demand — prime ground-floor F&B space commands between USD 80 and USD 150 per sqm per month, with top-tier mall anchors at Vincom Center Dong Khoi averaging USD 84.8 per sqm per month in Q1 2025 [4]. Premium locations in District 1 frequently operate on waiting lists, underlining the constrained supply of high-street frontage relative to demand. For F&B operators, District 1 is best suited to high-CAPEX flagship or experiential dining concepts that can derive brand value and tourist-driven volume to justify occupancy cost.

District 3 – The Lifestyle and Mid – Premium Submarket: District 3 offers a compelling alternative to District 1’s rental intensity. Its dense residential fabric, boutique commercial streets — particularly Vo Van Tan and Nam Ky Khoi Nghia — and established café culture have made it one of the city’s most organic F&B ecosystems. Rental levels typically range between USD 50 and USD 90 per sqm per month, reflecting strong consumer density without the premium associated with tourist-facing prime locations. District 3 is well-suited to mid-tier dining concepts, specialty cafés, wine bars, and independent brands targeting upper-middle-class local consumers.

District 7 (Phu My Hung) – The Expatriate and Family Hub: District 7’s Phu My Hung township has long served as HCMC’s primary expatriate enclave, hosting a large Korean and Japanese community alongside affluent Vietnamese families. Retail rents in Phu My Hung range from USD 40 to USD 75 per sqm per month, with other parts of District 7 offering prices approximately 20–25% below Phu My Hung levels [5]. Mall anchors SC VivoCity and Crescent Mall generate consistent weekend traffic, while the district’s demographic profile creates stable demand for specialty cuisine concepts — Korean barbecue, Japanese casual dining, international bakery chains — that would face intense competition in District 1 at significantly higher cost.

Binh Thanh and Phu Nhuan – The Transitional Inner Ring: Sitting between the CBD and the city’s outer ring, Binh Thanh and Phu Nhuan offer a transitional pricing tier of approximately USD 30–60 per sqm per month. Phu Nhuan’s Phan Xich Long street has emerged as one of HCMC’s most vibrant café corridors, with a concentration of independent specialty coffee and lifestyle F&B concepts that have drawn comparisons to Tay Ho in Hanoi. Binh Thanh’s high residential density and proximity to the city centre make it well-suited for mid-tier chain rollouts seeking affordable inner-city locations with strong catchment populations.

Thu Duc City – The Eastern Growth Corridor: Formally established in 2021 by merging the former Districts 2, 9, and Thu Duc, Thu Duc City has emerged as HCMC’s most dynamic growth submarket. Property values in well-connected areas such as Thao Dien have risen by 15–20% annually in recent years, yet street-level F&B rents remain approximately 30–40% below District 1 equivalents, typically ranging from USD 20 to USD 45 per sqm per month [5]. The completion of Metro Line 1 — connecting Ben Thanh to Suoi Tien — has materially improved footfall dynamics in the eastern corridor, proofed by the fact that 20.6 million passengers used the Metro Line 1 in 2025, equivalent to 122% of the planned target [13]. Vincom Mega Mall Grand Park (District 9) opened in Q2 2024 with 32,000 sqm of net lettable area and achieved 90% occupancy upon launch [3], confirming the corridor’s demand fundamentals. Thu Duc is structurally well suited to scalable QSR chains, café networks, and delivery-focused kitchen formats.

Tan Binh, Tan Phu, and Go Vap – The Affordable Outer Belt: The city’s northwestern outer belt — Tan Binh, Tan Phu, and Go Vap — offers the most affordable retail entry points in HCMC, with F&B rents typically ranging from USD 15 to USD 35 per sqm per month. These districts are characterized by very high residential density, proximity to Tan Son Nhat International Airport (Tan Binh), and limited premium retail supply. AEON Tan Phu functions as the primary mass-market retail anchor for this corridor, drawing significant consumer volume from across the city’s western catchment. For value-tier F&B brands and domestic chain operators pursuing volume-based models, the outer belt offers cost-efficient network expansion.

District – Level Pricing and F&B Business Potential in 2026

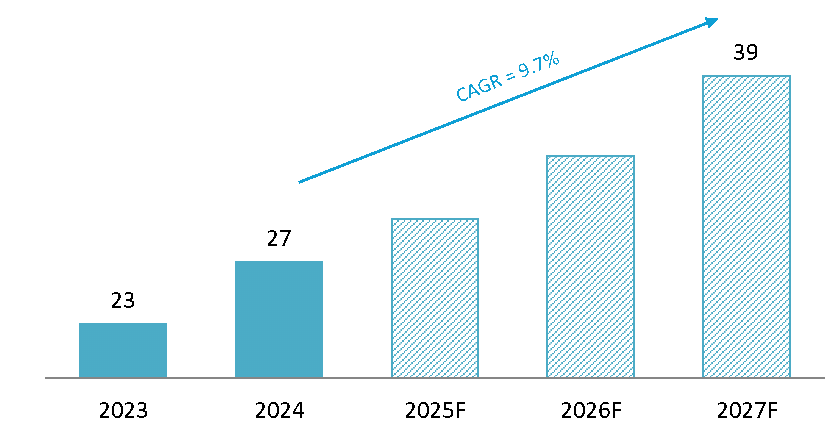

Vietnam’s F&B industry provides a robust macro backdrop for HCMC-based investment. The sector reached USD 27.3 billion in revenue in 2024 — a 16.6% year-on-year increase — with forecasts projecting growth to USD 36.86 billion by 2027 at a compound annual growth rate of 9.7% [6].

Vietnam’s F&B Sector Market Size (Billion USD)

Source: Vietnam Briefing

Regulatory & Cost Pressures

Before assessing district-level opportunities, investors must account for two structural cost headwinds reshaping the sector’s economics in 2026. First, the Special Consumption Tax (SCT) Law, effective January 1, 2026, introduces excise duties on beverages containing more than 5 grams of sugar per 100ml [6] — a direct hit to milk tea chains, juice bars, and beverage-heavy concepts, precisely the formats most prevalent in price-sensitive mid-tier and outer-belt districts. Second, approximately 45.3% of F&B firms have already raised prices in H1 2025 due to rising input costs, rent inflation, and labor pressures [8], compressing margins sector-wide. Together, these pressures make effective rent — measured as a share of projected revenue per sqm — the non-negotiable primary metric for site selection in 2026, ahead of brand prestige or absolute price.

The National Assembly (NA) cast their vote on the revised Excise Tax Law

Source: VietnamNews [12]

F&B Business Potential in Thu Duc area

District-level rental differentiation should directly shape format and capital allocation decisions. In District 1, 5.8 million foreign visitors in 2024 — projected to grow 10% in 2025 [4] — alongside a high-income domestic base, justify premium flagship investment, provided revenue-per-sqm is anchored to realistic occupancy. Districts 3, Binh Thanh, and Phu Nhuan offer rents 40–65% below CBD levels with comparable consumer density, favorable for boutique cafés and mid-tier dining from early operational quarters. District 7’s expatriate enclave supports specialty international formats at a fraction of District 1’s occupancy cost.

Thu Duc City is HCMC’s most compelling F&B expansion target in 2026, driven by three converging fundamentals. First, infrastructure: Metro Line 1 — fully operational between Ben Thanh and Suoi Tien — has directly elevated footfall along the entire eastern corridor, particularly at the An Phu, Phuoc Long, and Binh Thai stations, each anchoring dense residential and office catchments. Second, retail scale: Vincom Mega Mall Grand Park (32,000 sqm NLA) achieved 90% occupancy upon its Q2 2024 launch [3], confirming that large-format consumer demand in Thu Duc is no longer speculative. Third, economics: street-level F&B rents across Thu Duc range from USD 20–45/sqm/month [5] — 55–75% below District 1 equivalents — while the addressable population across the former Districts 2, 9, and Thu Duc now exceeds 1 million residents, with above-average household income growth driven by ongoing tech-park and university cluster development.

For the format strategy, Thu Duc presents three distinct sub-market opportunities. The Thao Dien–An Phu corridor (former District 2) supports boutique cafés, brunch concepts, and international casual dining targeting its high-income expatriate and professional base. The Grand Park precinct (former District 9) — anchored by Vincom Mega Mall — suits QSR chains, bubble tea, and family casual dining, serving its large young-family catchment. For delivery-first operators, Thu Duc is structurally the strongest cloud kitchen location in HCMC: online food delivery in Vietnam is growing at approximately 30% annually, with cloud kitchen formats projected to expand at a CAGR of 19% between 2024 and 2029 [6] — and Thu Duc’s lower rents make the delivery-revenue-to-rent ratio significantly more favorable than any inner-city district.

결론

HCMC’s retail leasing market in 2026 is defined by a pricing spectrum that spans from USD 150 per sqm per month at District 1’s prime high streets to USD 15 per sqm per month in the city’s outer residential belt. This tenfold range is not a market inefficiency — it reflects genuine differences in consumer density, income levels, tourism exposure, and infrastructure maturity across the city’s districts. For F&B investors, this spectrum should be read as a strategic opportunity map: premium flagship in District 1 for brand-building and tourist capture; lifestyle and boutique concepts in District 3 and Phu Nhuan for margin sustainability; specialty international formats in District 7 for expatriate-market capture; and scalable QSR or delivery-first models in Thu Duc for long-term volume growth. With nearly 80,000 sqm of additional retail supply projected to enter HCMC by 2028 [2], competition for prime locations will intensify further — making the case for early-mover positioning in high-potential secondary districts stronger than at any previous point in the city’s retail evolution.

더 읽어보기

* 본 기사의 내용을 인용하고자 하시는 경우, 저작권을 존중하여 출처와 원 기사의 링크를 함께 명시해 주시기 바랍니다.

| 비앤컴퍼니

2008년부터 베트남에서 시장 조사를 전문으로 하는 최초의 일본 기업입니다. 업계 보고서, 업계 인터뷰, 소비자 설문 조사, 비즈니스 매칭을 포함한 광범위한 서비스를 제공합니다. 또한, 최근 베트남에서 900,000개 이상의 기업에 대한 데이터베이스를 개발하여 파트너를 검색하고 시장을 분석하는 데 사용할 수 있습니다. 문의사항이 있으시면 언제든지 문의해주세요. info@b-company.jp + (84) 28 3910 3913 |

참조

- WifiTalents — Vietnam F&B Industry Statistics — https://wifitalents.com/vietnam-food-and-beverage-industry-statistics/

- Cushman & Wakefield — HCMC Retail MarketBeat Q2/2025 — https://www.cushmanwakefield.com/en/vietnam/insights/ho-chi-minh-city-marketbeat/retail-marketbeat

- Real Estate Asia — HCMC Retail Rents Q2/2024 — https://realestateasia.com/commercial-retail/news/ho-chi-minh-city-retail-rents-increase-until-end-2024

- Occupi — Vincom Center Dong Khoi, District 1 — https://getoccupi.com/malls/vincom-center-dong-khoi

- Best Real Estate HCMC — Emerging Neighborhoods 2025 — https://bestrealestatehcm.com/blog/emerging-neighborhoods-hcmc-2025/

- Vietnam Briefing — Foreign F&B Chains in Vietnam’s Growing Market — https://www.vietnam-briefing.com/news/foreign-food-chains-thrive-in-vietnams-growing-fb-market.html/

- B-Company — Mass Closure of F&B Stores H1/2025 — https://b-company.jp/the-trend-of-mass-closure-of-fb-stores-in-the-first-half-of-2025/

- The Investor — Vietnam H1 F&B Revenue Amid Cost Pressures — https://theinvestor.vn/vietnams-h1-fb-revenue-rises-slightly-amid-cost-pressures-d17311.html

- Best Real Estate HCMC, Emerging Neighborhoods 2025 — https://bestrealestatehcm.com/blog/emerging-neighborhoods-hcmc-2025/

- Avison Young Vietnam Q1/2025 Report — https://www.avisonyoung.com/news-releases/-/aynp/view/2025/04/15/avison-young-vietnam-releases-quarterly-report-of-vietnam-real-estate-quarter-i-2025/in/vietnam

- Avison Young Vietnam Q3/2025 Report — https://www.avisonyoung.com/news-releases/-/aynp/view/2025/10/14/quarterly-report-of-vietnam-real-estate-quarter-iii-2025/in/vietnam

- https://vietnamnews.vn/politics-laws/1719562/viet-nam-passes-new-excise-tax-law-to-protect-public-health-and-environment.html

- https://english.thesaigontimes.vn/hcmc-metro-line-1-carries-over-20-5-million-passengers-in-2025/

- https://theinvestor.vn/vietnams-h1-fb-revenue-rises-slightly-amid-cost-pressures-d17311.html

관련기사

사이드바:

뉴스레터 구독