This article examines the accelerating EV transition across Southeast Asia, identifies structural market opportunities arising from this shift.

12Jun2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

Abstract

For decades, Southeast Asia’s automotive market was defined by Japanese-brand dominance, gasoline two-wheelers, and modest electrification ambitions. That picture has changed dramatically. As of late 2025, ASEAN countries now rank among the highest EV (electric vehicle) adoption markets in the world — overtaking the United States, the United Kingdom, and the European Union on key penetration metrics.¹

This article examines the accelerating EV transition across Southeast Asia, identifies structural market opportunities arising from this shift, and illustrates how regional players, particularly those native to ASEAN, are best positioned to capitalize on them. It concludes with practical implications for investors and market entrants.

Market overview: Southeast Asia EV by the numbers

The ASEAN EV market was valued at approximately USD 4.6 billion in 2025 and is projected to reach USD 6 billion in 2026, before scaling to USD 23.6 billion by 2031, at a compound annual growth rate of 31.6%.² By a separate estimate, the market could generate annual sales opportunities of USD 80–100 billion by 2035, up from just USD 2 billion in 2021.³

The table below summarizes EV market status across ASEAN’s five largest automotive markets as of 2025:

Table 1: Southeast Asia EV market status: 5 key markets (2025)

| Country | EV domestic sales share (2025) | Key policy | Notable investment |

| Vietnam | ~40% | Tax incentives, VAT reduction, public fleet mandates | VinFast (domestic); World Bank forecasts 6.5M jobs by 2050⁴ |

| Thailand | ~20% | “30@30” target (30% Zero Emission Vehicle-ZEV by 2030) | Toyota, BYD, Tesla, and Hyundai plants operational or committed to local production⁵ |

| Indonesia | ~15% | Reduced VAT on EVs, import tariff cuts for local producers | BYD factory, VinFast Subang plant, CATL company battery facility⁶ |

| Malaysia | Growing | EV roadmap under the National Energy Transition | Proton EV line ($19.5M, 20,000 units/year capacity)² |

| Philippines | Early stage | EV Industry Development Act | VinFast e-scooter MoU with first dealer partners⁷ |

B&Company’s synthesis

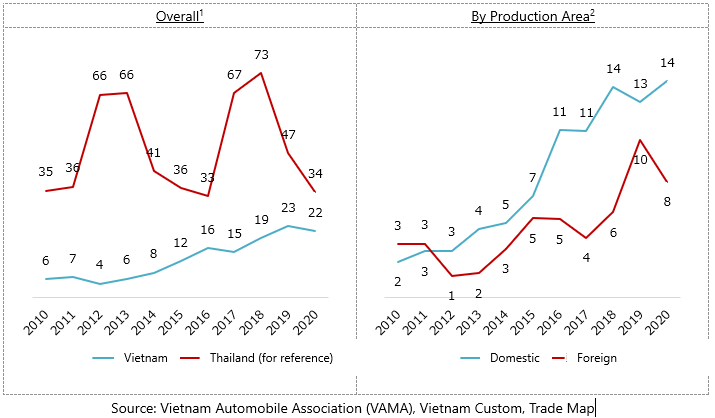

In Southeast Asia, electric car sales grew by nearly 50% in 2024, representing 9% of all car sales across the region. Among 5 five markets highlighted above, Vietnam and Thailand recorded the highest individual shares.⁸

Policy as the engine: Governments are driving the transition

Related article

Log in / Register

Continue without an account

Log in / Register

SUBSCRIBE NEWSLETTER