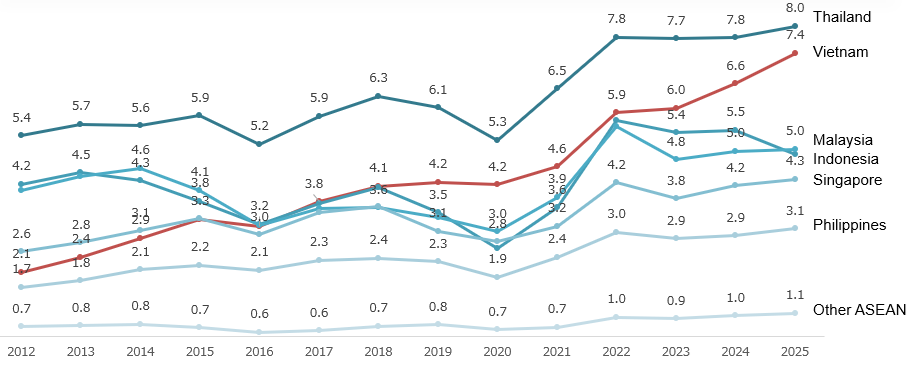

Japan's trade dynamics within ASEAN have evolved considerably, with Vietnam emerging as one of the fastest-growing regional trade partners.

03Jun2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

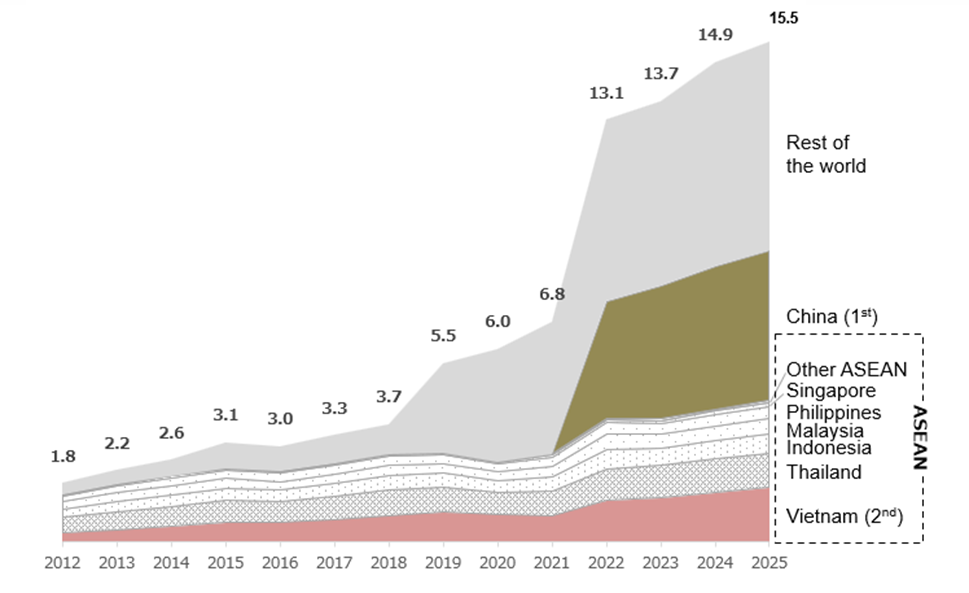

Over the past decade, Japan’s overall trade structure has remained surprisingly stable despite major disruptions such as the US–China trade tensions, the COVID-19 pandemic, supply chain restructuring efforts, and the implementation of new regional trade agreements. From 2012 to 2025, ASEAN consistently accounted for approximately 15% of Japan’s total trading volume (imports + exports), while China maintained around 21%, with the remaining 64% coming from the rest of the world.

However, trade dynamics within ASEAN have evolved considerably, with Vietnam emerging as one of Japan’s fastest-growing regional trade partners. While Thailand has consistently remained Japan’s largest ASEAN trading partner in terms of total trade volume, Vietnam has recorded significantly stronger growth than most neighboring economies over the past decade with average annual growth rate of 10.6%, compared to other countries’ AAGR of 3.6%.

Japan’s trading volume (import + export) with ASEAN countries

Unit: Bil JPY

Source: B&Company synthesis (Japan Customs)

Contributing to Vietnam’s growing importance in Japan–ASEAN trade is the country’s participation in an extensive network of regional trade agreements such as VJEPA, AJCEP, CPTPP, and RCEP compared to many other ASEAN neighbors. As a result, Vietnam ranks among Japan’s leading trading partners in terms of import value utilizing EPA preferential schemes, second only to China and the highest within ASEAN. This indicates that preferential trade frameworks have played a critical role in strengthening Vietnam’s position as a manufacturing and export base within Japan-centered regional supply chains.

Japan’s imports using EPAs by regions and top countries

Unit: Bil JPY

Source: B&Company synthesis (Japan Customs)

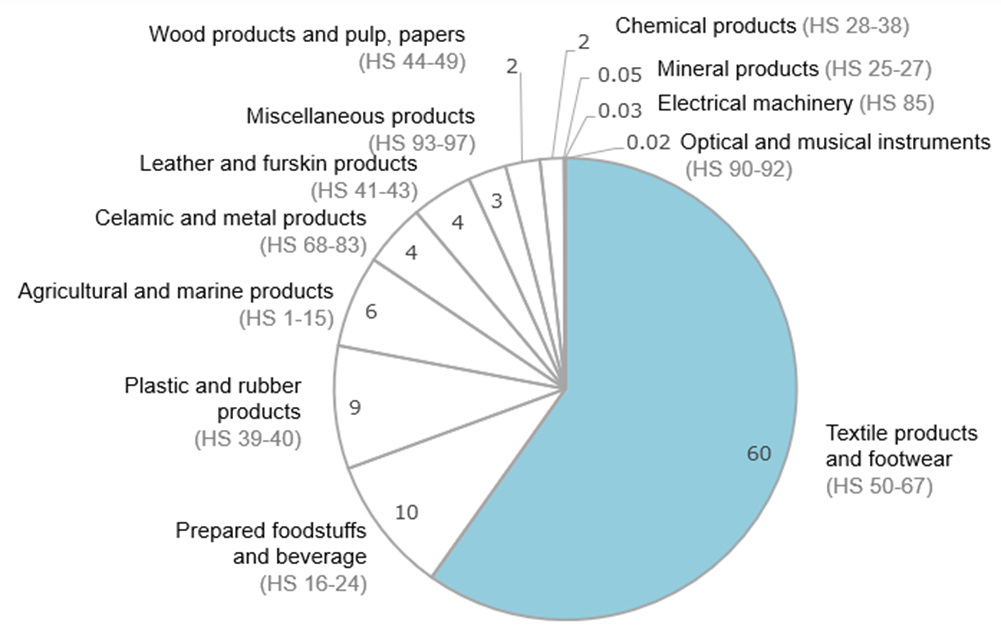

At the same time, the structure of Vietnam’s EPA utilization reveals a potentially important vulnerability. While Thailand’s preferential exports to Japan are relatively diversified across multiple industries, Vietnam’s EPA utilization remains heavily concentrated in textile- and apparel-related products (HS50–67), accounting for approximately 60% of total import value utilizing EPA schemes in 2025. While textile- and apparel-related products already represent one of Vietnam’s largest export categories to Japan, EPA utilization is even more heavily concentrated in these sectors. Electrical machinery (HS85) currently ranks as Japan’s largest import category from Vietnam, followed by industries such as machinery, wood products and paper, miscellaneous products, agricultural and marine products, plastics and rubber, prepared foodstuffs and beverages, chemical products, transport equipment, leather products, and optical instruments. However, compared to textile and apparel products, many of these sectors still account for a relatively limited share of imports utilizing EPA preferential schemes. This suggests that although Vietnam’s export structure to Japan has gradually diversified, the practical benefits derived from EPA frameworks remain concentrated primarily in labor-intensive industries such as garments, footwear, and textiles.

Use of FTAs in imports from Vietnam by sector in 2025

Related article

Log in / Register

Continue without an account

Log in / Register

SUBSCRIBE NEWSLETTER