Vietnam's private healthcare expenditure is set for strong growth, with foreign investment driving rapid improvements.

29Aug2025

Latest News & Report / Vietnam Briefing

Comments: No Comments.

Vietnam’s private healthcare sector is evolving rapidly, driven by rising demand, foreign investment, and supportive policies. With B2B clinics benefiting from stable corporate contracts and B2C clinics catering to individual households, both models are increasingly leveraging technology, setting the stage for a more dynamic and competitive private healthcare landscape in the country.

Private healthcare overview

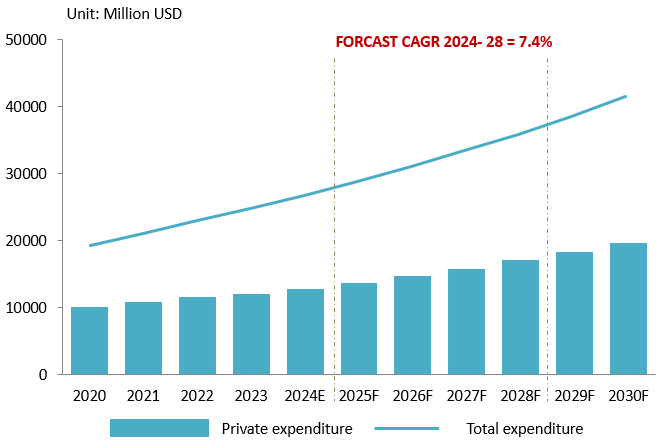

According to the Ministry of Health, Vietnam’s private healthcare sector has shown significant development, with 348 private hospitals making up 24% of the country’s total hospitals and nearly 50,000 licensed clinics. Vietnam’s private healthcare expenditure is set for strong growth, with foreign investment driving rapid infrastructure expansion and service quality improvements in hospitals and clinics. Government policies aimed at easing pressure on overcrowded public hospitals are also creating more space for private sector participation. These factors combined are fostering a more competitive and resource-rich private healthcare ecosystem, with private healthcare spending projected to grow at a CAGR of 7.4% between 2024 and 2028 [1].

Several key trends are driving long-term growth in demand for private healthcare in Vietnam. The expanding middle class, rising disposable incomes, and increased household spending are fueling higher demand for private services. Demographic shifts, with an aging population and growing health awareness, along with greater uptake of preventive care and insurance, further support this growth. Additionally, the trend of Vietnamese patients seeking treatment abroad underscores unmet domestic demand, benefiting private providers.

Healthcare expenditure in Vietnam (2020 – 2030F)

Source: FiinGroup

Current private clinic services

Vietnam’s private healthcare sector encompasses more than large hospitals, with two main clinic models: Administrative/Industrial-focused (B2B) and Residential-focused (B2C).

An example of a private B2C healthcare clinic

Source: Family Medical Practice

B2B clinics, located near administrative centers or industrial zones, provide mandatory health check-ups, occupational health exams, and on-site medical services for companies, government agencies, and factories. Their operations rely on legal compliance and employee welfare programs, with success driven by strong B2B relationships, organized health screenings, and professional service delivery.

An example of a private B2B healthcare clinic

Source: Tomec

B2C clinics, situated near residential areas, function as modern “family doctors,” serving multi-generational households. They offer regular check-ups, chronic disease management, routine screenings, and home-based services, including sample collection, intravenous therapy, and post-operative care. Key success factors include convenient location, doctor reputation, community trust, and comprehensive service offerings that support patient loyalty and long-term brand value.

Technology has become integral across both models. Telemedicine allows B2C clinics to conduct follow-ups, manage chronic conditions remotely, and optimize home care, while B2B clinics provide employees with rapid access to medical advice without disrupting work [3]. Digital tools such as clinic management software, electronic medical records (EMR), online scheduling systems, and patient mobile applications streamline operations, reduce errors, save time, and enhance the overall patient experience, forming a core competitive advantage in Vietnam’s evolving private healthcare landscape [4].

Comparison between B2C and B2B clinics in Vietnam

| Criteria | Residential-Focused (B2C) | Administrative/Industrial-Focused (B2B) |

| Target Customers | Multi-generational households (children, women, elderly) and individuals. | Companies, organizations, factories, and government agencies. |

| Demand Drivers | Personal healthcare needs, convenience, trust, and overcrowding in public hospitals. | Legal requirements, employee welfare policies, and productivity enhancement. |

| Core Service Offerings | Family medicine, general check-ups, home visits for consultations and tests, chronic disease management, and vaccinations. | Corporate health check-ups (contract-based), mobile health screenings, occupational health exams, and on-site medical services. |

| Revenue Model | Pay-per-service (fee-for-service), personal health check-up packages, direct payment, or insurance-based. | Long-term contracts (typically 1 year), payment by package/employee count, steady cash flow. |

| Staff Requirements | Reputable general practitioners, family doctors, pediatricians, obstetricians, and a versatile nursing team (home visits). | Flexible medical team (willing to conduct mobile health screenings), professional B2B sales team with network connections, and project coordinators. |

| Sensitivity to Location | Extremely important. Should be located in high-density areas, easily accessible, with a spacious frontage. | Location is more flexible. Can be near industrial zones or office spaces, but not essential due to mobile services. Logistics convenience is more important. |

| Example | Family Medical Practice | NHAN VIET General Clinic |

Source: B&Company compilation

The B2B private clinic model in Vietnam shows stronger growth than the B2C model due to differences in client acquisition, revenue stability, and competition. B2B clinics benefit from a concentrated and predictable client base, as companies are legally required to provide annual health checks for employees [4]. A single corporate contract can cover hundreds or thousands of people, ensure steady cash flow, and optimize operational costs.

In contrast, B2C clinics serve a fragmented, sporadic market, relying on individual patients whose demand arises mainly during illness. This drives higher marketing costs and inefficiencies from unpredictable patient flow. Moreover, B2C clinics face strong competition from public hospitals, which enjoy established trust and national health insurance coverage, limiting private clinics to minor or convenience-focused services [5]. B2B clinics largely avoid this direct competition by focusing on mandatory corporate health services.

Impact of the New Health Insurance Policy from 2025 on Private Clinics

The 2024 amendments to the Health Insurance Law will have a significant impact on the operations of private clinics, offering both opportunities and challenges.

Opportunities from the New Policy:

– Expansion of benefits for health insurance participants: With the new law, health insurance holders can seek treatment at any primary care or frontline medical facility nationwide, including private clinics registered for health insurance services. This creates an opportunity for private clinics to attract more insured patients.

– Access to specialized care: Patients can be directly referred to specialized healthcare facilities for rare or critical illnesses without going through the usual referral system, allowing private clinics to develop specialized services.

– Expansion of insurance coverage: The new law adds benefits for services like treatment for strabismus and refractive errors for those under 18, which helps private clinics attract a new patient demographic.

Challenges from the New Policy:

– Increased management burden and costs: The implementation of actual cost-based payments for inpatient care and the addition of new services covered by insurance, such as payment for drugs and medical equipment transfer between healthcare facilities, will push private clinics to invest in technology and management processes to comply with insurance requirements.

– Increased compliance requirements: Private clinics will need to improve service quality and ensure compliance with new health insurance payment regulations, while also facing administrative and cost management challenges.

The new policy benefits B2B clinics by ensuring a steady flow of patients through mandatory corporate health services, while B2C clinics may face increased competition from public hospitals, which now offer broader coverage under the insurance scheme. It is essential for private B2C clinics to differentiate themselves through quality, convenience, and specialized services. The article could explore these differences more in-depth and suggest specific strategies for each model.

Implications for investors

Investors must assess regional market dynamics to choose the most suitable investment model, aligning with local demand and characteristics. For example, the B2B model may thrive in industrial zones or areas with high corporate presence, while the B2C model is better suited for densely populated residential areas. Understanding target customer needs and the competitive landscape in each region is crucial to making informed investment decisions.

Investors should prioritize investing in digital tools like clinic management software, EMR, and telemedicine to enhance service delivery, operational efficiency, and compliance with health insurance regulations. Telemedicine can offer remote consultations and chronic disease management, giving clinics a competitive edge. Additionally, heavy investment in digital marketing, telemedicine, and home-based services, along with forming partnerships with insurers, can boost patient flow and credibility. Strategic location and brand positioning are crucial for long-term growth. For B2C clinics, combining family healthcare models with insurance schemes offers comprehensive services, enhancing patient convenience and trust.

The B2B model generates stable and predictable revenue through long-term contracts with corporations and government entities. These contracts, combined with legal health check requirements, ensure consistent demand and provide a reliable cash flow with lower market risks. Success in this model hinges on cultivating strong relationships with corporate clients, delivering high-quality services, and optimizing operational processes. Investors should focus on securing long-term agreements, fostering corporate ties, and considering potential B2C service expansion under the new health insurance regulations to diversify income sources.

The B2C model, which focuses on family and residential healthcare, offers higher service margins, especially with specialized or premium healthcare offerings. It provides opportunities for brand development and patient loyalty. However, the competition is fierce, with both local clinics and hospital chains vying for residential market share. To stand out, clinics must deliver exceptional patient care, establish a strong reputation for their medical professionals, and offer a range of services, including home visits and preventive care.

Conclusion

Vietnam’s private healthcare sector is set for growth, driven by increasing demand and rising healthcare spending. To meet consumer demands, the development of private clinics is seen as a strategic response to the growing need for hand-on accessible and quality healthcare services. Technological advancements such as telemedicine and digital tools will enhance service delivery, while the 2025 Health Insurance Policy changes present new opportunities. Investors should consider both the stability and long-term growth potential of this expanding sector, with a focus on meeting the evolving needs of Vietnamese consumers.

[1] FiinGroup, Vietnam’s Private Healthcare Sector: A Strategic Growth Market for Institutional Investors <Access>

[2] Lao Dong News, Investment opportunities in Vietnam’s middle class <Access>

[3] Long Chau, Telemedicine: Concept, Benefits, and Services Implemented <Access>

[3] Dau Tu News, Digital transformation in hospitals: An inevitable trend in the healthcare industry <Access>

[4] Law on Labor Safety and Hygiene 2015 <Access>

[5] Sacomtec, Success Factors in Private Clinic Management <Access>

[6] Amendments to some articles of law on health insurance <Access>

[8] Ministry of Health, Private healthcare gradually asserts its position in the people’s health care system. <Access>

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 900,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 28 3910 3913 |

Related article

SUBSCRIBE NEWSLETTER