This article analyzes the state of Vietnam's cold chain logistics market, focusing on the specific dynamics within food and pharmaceutical sectors.

11Jun2026

Highlight content / Highlight Content JP / Highlight content vi / Industry Reviews / Latest News & Report

Comments: No Comments.

Abstract

This article analyzes the current state of Vietnam’s cold chain logistics market, focusing on the specific supply and demand dynamics within the food and pharmaceutical sectors. It outlines the market’s heavy concentration in the South and the logistical hurdles of North-South transportation. By examining how Japanese companies are strategically investing through M&A, new facility construction, and automation, the report identifies practical expansion opportunities for foreign investors aiming to capture high-margin segments and optimize supply chain routes in Vietnam.

Overview of Cold Chain in Vietnam

Vietnam’s cold chain logistics market is experiencing steady growth, driven by a strong export economy and shifting domestic consumption. The overall market is valued at approximately USD 5 BUSD in 2023, in which the south holds the highest market share (60%)[1]. This concentration is primarily due to the region’s strong agricultural output and proximity to major export ports. However, a deeper look into specific sub-categories reveals complex supply and demand gaps.

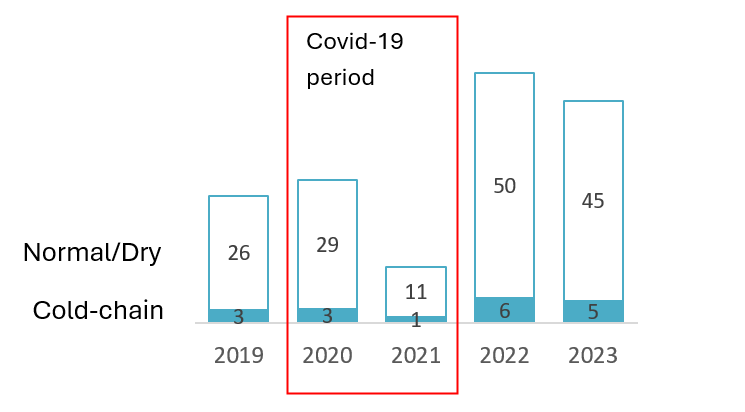

Revenue of the Logistics sector

Unit: billion USD

Source: B&Company calculation based on Enterprise Database on VSIC code from 49 to 52 (exclude passenger transportation VSIC code) and In-depth Interviews with Experts about Logistic sector market share

The Food Industry Demand & Supply Situation

In the food sector, cold chain demand remains unfulfilled for both transportation and warehousing. This need is expected to grow further as consumers increasingly prefer processed and frozen foods. The highest demand is concentrated in the Southern region—encompassing the Central areas, the Southeast, and the Mekong Delta—due to the dense presence of food processing and fishery companies, as well as the naturally warm weather characteristics that require strict temperature control.

Besides shifting domestic consumption patterns, another significant driver for cold chain expansion is Vietnam’s booming agricultural output and export requirements.

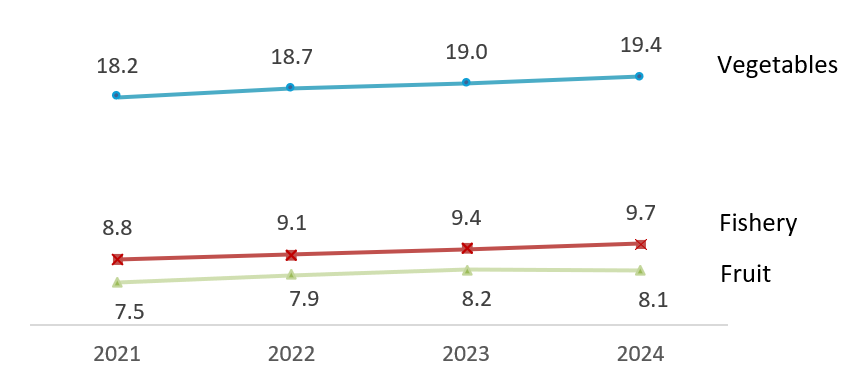

Production of some Vegetables, Fruits, and Fishery, 2021 – 2024

Unit: mil tons

Source: National Statistics Office

Vietnam produces tens of millions of tons of fruits, vegetables, and fishery products annually. However, this massive volume of agricultural production contrasts sharply with the current infrastructure capacity, leading to severe post-harvest food loss. Currently, up to 25% of agricultural products are lost before reaching processing factories or distribution centers, causing an estimated economic loss of USD 3.9 billion annually.[2]

On the supply side, most cold-chain logistics providers are located in the South, primarily operating around Ho Chi Minh City, Binh Duong, and Dong Nai. This heavy regional concentration has led to severe competition, forcing companies to invest in new and modern facilities, such as refrigerated trucks and advanced temperature control systems, to gain a sales advantage. Meanwhile, the Northern market remains quite fragmented and is only just starting to develop its cold storage infrastructure.

A major operational hurdle for logistics companies is nationwide transportation. Big logistics companies equipped with IT systems and distribution centers (DCs) have better utilization in truck rotation, giving them the ability to operate nationwide. However, not many companies provide the whole transportation route from the North to the South. This is due to a high cost of goods sold (COGS) and a high percentage of empty miles on return trips, which lead to low profit margins. To operate efficiently and utilize their fleets, companies would benefit from having distribution centers in the central region of the country.

The Pharmaceutical Industry Demand & Supply Situation

The pharmaceutical sector presents a different landscape with strict operational requirements. The demand for cold storage and transportation is increasing specifically for temperature-sensitive products, mostly vaccines, while other products such as medical biologics and insulin can often be stored in normal temperature conditions. Demand is particularly high in the North and South, where most pharmaceutical manufacturers are concentrated. Pharmaceutical companies generally operate their own in-house logistics fleets, and outsourcing to external carriers is used only when additional capacity is required.

Supply in this sector is heavily constrained. There is limited participation from small and medium-sized enterprises (SMEs) due to strict temperature control and storage technology requirements, as well as Good Storage Practice (GSP) standards, which demand significant investment to ensure service quality. Consequently, large pharmaceutical companies tend to partner with major logistics providers that offer comprehensive 3PL services to leverage existing cold chain infrastructure. At the same time, leading pharmaceutical distributors are also heavily investing in their own cold chain facilities to guarantee product safety. Examples include leading downstream pharmaceutical players such as FPT Long Châu and VNVC, which have invested in their own GDP/GSP-compliant warehouses, cold storage facilities, refrigerated transport, and temperature monitoring systems to ensure product safety

Investment of Japanese Companies

Japanese companies have recognized these structural challenges as a strategic entry point. Rather than competing in crowded, low-margin segments, they focus their investments on introducing advanced technology, high compliance standards, and strong capital backing to solve Vietnam’s specific supply chain bottlenecks.

Major Cold-Chain Logistic Japanese Companies[3][4][5][6][7]

| Company | Establishment Year | Offerings | Key feature |

| Konoike Vinatrans | 1996 | Frozen and refrigerated warehousing, marine cargo, temperature-controlled trucking. | · First Japanese logistics company in Vietnam

· Their facilities are HACCP, SSOP, and GMP certified. |

| SG Sagawa Vietnam | 1997 | General, bonded, and cold warehousing, international air/sea freight, domestic express delivery. | · Offer a fully integrated 3PL network across Vietnam |

| Meito Vietnam | 2014 | Multi-temperature commercial cold storage, handling, and distribution center operations. | · Operates a massive 30,000-pallet capacity across multiple warehouses in the South, creating a highly optimized network for logistics |

| CLK Cold Storage | 2015 | Refrigerator/Freezer Warehouse Business (Bonded Warehouse included.) Consigned Freight Forwarding Business, Distribution Consulting Business. |

· Offer Four-temperature-zone warehousing (frozen, refrigerated, chilled, and ambient)

· Utilize energy-saving technology and high-tech solutions for cold storage, such as solar panel systems, intensive moisture–proof measures, etc. |

| Nichirei TBA Logistics | 2023 | Commercial cold storage, blast freezing, repacking, and nationwide refrigerated trucking. | · Features a 10-room cold storage system with a capacity of approximately 20,000 pallets and a 3,000 sqm buffer room. Capable of providing cold storage rental services that meet all capacity needs for frozen and chilled goods across various temperature ranges (from -25°C to 22°C) |

Source: B&Company’s synthesis

Recent Investment Trends in the Cold Chain

In recent years, the investment strategy of Japanese companies in Vietnam’s logistics sector has shifted toward deep integration, automation, and targeted market expansion.

Mergers, Acquisitions, and Strategic Alliances: A clear trend is the use of M&A to rapidly acquire local networks rather than building them from scratch. A prime example is Mitsubishi Logistics Corporation, which successfully acquired a 20.5% equity stake in Indo Trans Logistics Corporation (ITL), officially making the Vietnamese logistics giant an equity-method affiliate in 2023.1 By combining Mitsubishi’s capital with ITL’s massive domestic infrastructure—which includes over 100,000 cold chain pallet locations—the partnership efficiently bypassed the time-consuming process of building a nationwide network[8][9]

Greenfield Mega-Facilities and Automation: To combat rising operational costs and labor shortages, new Japanese investments are heavily focused on greenfield mega-facilities equipped with advanced automation. Yokohama Reito (Yokorei) is currently constructing a USD 52 million, 4.5-hectare automated refrigerated warehouse in Long An province, slated to begin commercial operations by March 2025. Similarly, Igarashi Reizo recently broke ground on a USD 24 million cold storage project in Tay Ninh Province. Scheduled for completion in early 2027, this facility explicitly aims to bring Japan’s most advanced robotic and automated storage technologies to Vietnam, helping to sustainably enhance the local supply chain while reducing long-term energy and labor costs.[10][11]

Opportunity for Expansion

The current supply-demand gaps and the successful models introduced by Japanese firms highlight several clear expansion opportunities for investors.

First, establishing intermediate distribution hubs in the Central region is a highly practical opportunity. Since full North-South transportation routes suffer from high COGS and empty return trips, building modern cross-docking or cold storage facilities in central provinces will allow logistics providers to optimize their truck rotations, reduce empty miles, and significantly improve profit margins.

Second, the fragmented Northern market presents a prime target for food logistics expansion. While the South suffers from fierce competition among existing providers, the North is still developing. Investors who build high-quality cold storage facilities near Hanoi or Bac Ninh can capture the growing demand for processed foods and e-commerce deliveries with much less direct competition.

Finally, the pharmaceutical logistics sector offers a lucrative niche for well-capitalized foreign companies. Because strict GSP standards and high technology costs prevent local SMEs from entering this space, international logistics firms can leverage their advanced temperature-monitoring systems and compliance expertise. By offering reliable, comprehensive 3PL services, these providers can attract large pharmaceutical manufacturers in both the North and South, gradually shifting them away from expensive in-house fleets toward outsourced logistics solutions.

Read more

Vietnam’s Cold Storage market: Strategic investment opportunities

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 1,000,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 28 3910 3913 |

[1] B&Company calculation based on Enterprise Database on VSIC code from 49 to 52 (exclude passenger transportation VSIC code) and In-depth Interviews with Experts about Logistic sector market share

[2] The Investor (2023). Yokorei builds $52 mln Vietnam cold storage facility as sector set to soar. <<Asess>>

[3] Konoike Website <<Assess>>

[4] Sagawa Vietnam Website <<Assess>>

[5] Meito Vietnam Website <<Assess>>

[6] CLK Cold Storage Website <<Assess>>

[7]VNexpress (2023). Nichirei Logistics Group establishes new joint venture company in Vietnam. <<Assess>>

[8] Indo Trans Logistics Corporation Website. <<Assess>>

[9] Mitsubishi Logistics Corporation Website <<Assess>>

[10] The Investor (2023). Yokorei builds $52 mln Vietnam cold storage facility as sector set to soar. <<Asess>>

[11] VCCI (2025). Japan’s Igarashi Reizo builds $24 mln cold storage project in southern Vietnam <<Assess>>

Related article

SUBSCRIBE NEWSLETTER