Vietnam pharmaceutical market has maintained a steady annual growth rate of 6% to 8% in 2023-2028, being one of the fastest growing in Asia.

08Apr2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

Vietnam’s pharmaceutical market is one of the fastest-growing in Southeast Asia. According to the Drug Administration of Vietnam (DAV) under the Ministry of Health, the country’s pharmaceutical market has maintained a steady annual growth rate of 6% to 8% for the period 2023-2028[1]. The total market value is projected to increase from around USD 2.7 billion in 2015 to approximately USD 8 billion by 2026, making Vietnam one of the fastest-growing pharmaceutical markets in Asia[2].

Growth Drivers of Rising Pharmaceutical Demand in Vietnam

Demand for pharmaceuticals in Vietnam is rising strongly, driven by population ageing and expanding health insurance coverage. In 2024, the number of people aged 60 and above reached 14.2 million, accounting for around 14% of the population, and this figure is projected to increase to 29.2 million by 2050[3]. An ageing population also means a higher prevalence of chronic diseases such as diabetes, cardiovascular diseases, and cancer, which in turn increases demand for both treatment and preventive medicines. In addition, more than 95% of Vietnam’s population is now covered by health insurance, enabling more people to access both domestic and imported medicines[4]. At the same time, rising income levels and improvements in the healthcare system, including broader access to medical examination and treatment services, are also pushing up pharmaceutical spending.

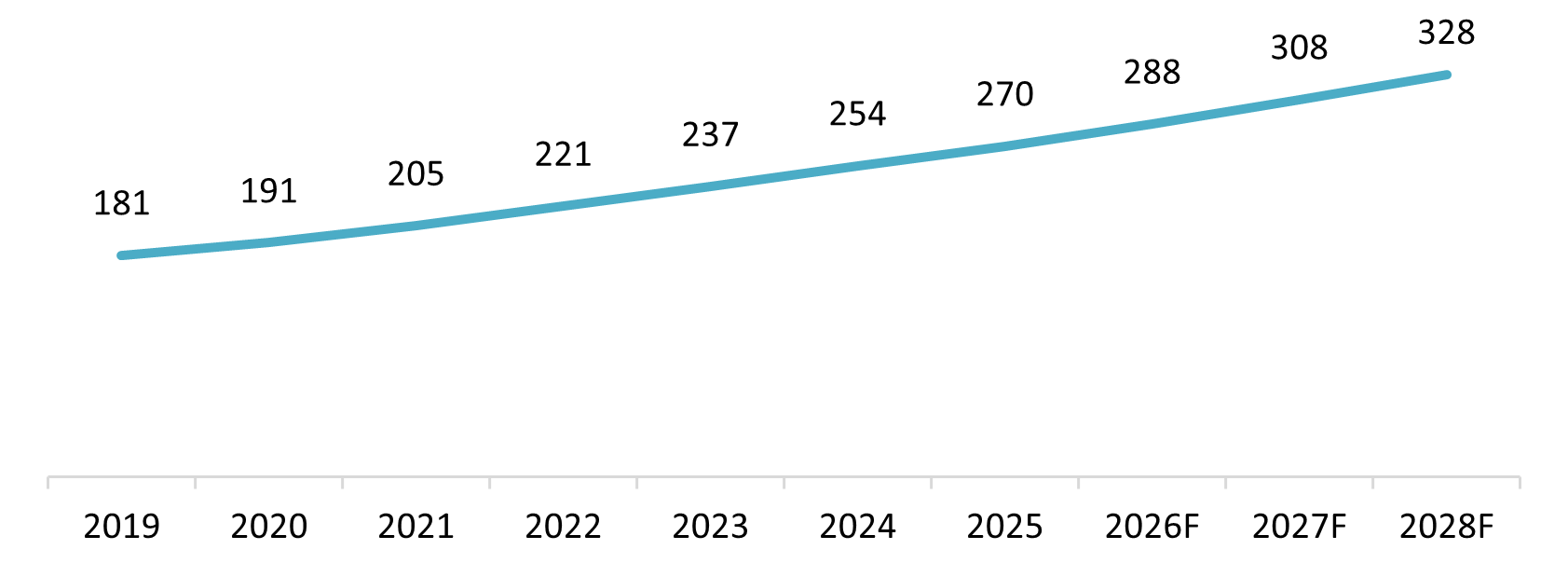

Average Healthcare Expenditure per Capita, 2019–2028F

Unit: USD

Source: Vnexpress

Vietnam’s per capita healthcare expenditure reached USD 270 per year in 2025, equivalent to around VND 7.3 million, with most of this spending allocated to medicines. This figure is forecast to rise to USD 328 (nearly VND 9 million) over the next three years[5]. As living standards improve, consumers are also expected to demand better treatment quality, driving stronger demand for branded drugs, next-generation medicines, and more specialized high-cost treatments.

Vietnam’s Pharmaceutical Supply Base: Expanding Capacity but High Import Dependence

From the supply perspective, the distribution network has expanded nationwide, helping ensure medicine availability across regions. At present, Vietnam has nearly 8,000 wholesalers and 95,600 retail outlets, including more than 40,500 pharmacies, 54,000 drug counters, and nearly 800 medicine cabinets at commune health stations[6]. Despite this wide retail footprint, modern pharmacy chains still had a relatively low penetration rate of below 10% in 2024, indicating that the market remained largely dominated by traditional independent stores (90%)[7]. Industry players include both domestic and multinational companies.

Main retail players in Vietnam pharmaceutical industry

| No. | Name | Founded | Origin | Store count | Key highlights |

| 1 | FPT Long Chau | 2007 | Vietnam | 2,417 pharmacies (as of year-end 2025) | Largest pharmacy chain in Vietnam by store count; also expanding into a broader healthcare ecosystem with vaccination centers. |

| 2 | Pharmacity | 2011 | Vietnam | 1,049 stores (as of year-end 2025) | One of the earliest modern pharmacy chains in Vietnam; strong nationwide urban presence and a broad OTC / health & wellness portfolio. |

| 3 | An Khang Pharmacy | 2002 | Vietnam | 419 pharmacies (as of April 2026) | Part of Mobile World Group (MWG); focuses on a modern pharmacy format with official products and standardized service. |

| 4 | Trung Son Pharma | 1997 | Vietnam | 200+ pharmacies (as of April 2026) | A long-established chain with strong coverage in the Mekong Delta and Ho Chi Minh City; positioned as a leading regional pharmacy player. |

| 5 | Phano Pharmacy | 2007 | Vietnam | 37 stores (as of March 2025) | An early pioneer in modern pharmacy retail; publicly described as the first chain in Vietnam to meet GPP, GSP, and GDP standards. |

B&Company’s synthesis

Vietnam’s modern pharmacy retail market is led overwhelmingly by domestic players, with FPT Long Chau standing out as the clear market leader by a wide margin. Pharmacity and An Khang also maintain notable nationwide footprints, while smaller chains such as Trung Son Pharma and Phano remain more limited in scale or regionally concentrated. Overall, the market is becoming more modernized, but it is still highly uneven, with store expansion concentrated mainly in a few major chains.

Long Chau Pharmacy Chain – Vietnam’s largest pharmacy retail network, serving one-third of the population

Source: Thanhnienviet.vn

Vietnam currently has around 243 GMP-WHO-certified pharmaceutical manufacturing plants, more than 1.5 times the 2015 figure of 158 plants. Among these 243 GMP-WHO-certified facilities, 29 plants meet higher standards such as GMP-EU or PIC/S. In terms of capacity, domestic production now meets around 60% of pharmaceutical demand by volume and 46% by value. Meanwhile, pharmaceutical exports reached approximately USD 312 million in 2025, ranking fourth in Southeast Asia. Notably, around 75% of this export value was generated by FDI enterprises, highlighting the growing role of joint ventures and foreign investment in the sector[8].

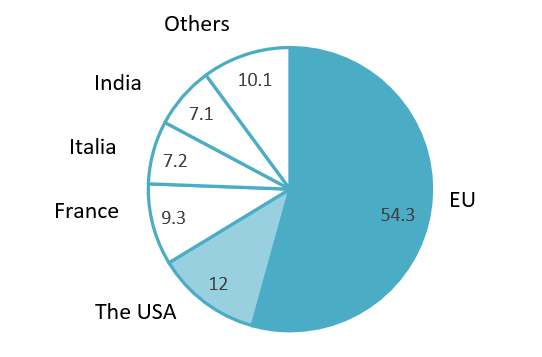

However, Vietnam is still mainly able to produce common and essential medicines with a moderate level of technological application, including 13 out of 13 essential drug categories and 11 out of 12 vaccine categories. As a result, the country still relies heavily on imports of pharmaceutical ingredients, specialty drugs, patented medicines, and high-tech pharmaceutical products. In addition, more than 90% of active pharmaceutical ingredients are still imported. In 2025, Vietnam’s total pharmaceutical import value reached nearly USD 4.3 billion[9].

Vietnam’s Largest Pharmaceutical Import Markets in 2025

Unit: %, 100% = USD 4.3 billion

Source: Doanhnghieptiepthi.vn

It can be seen that the EU is Vietnam’s largest source of pharmaceutical imports, far exceeding the US and other markets. This suggests that Vietnam’s import structure remains heavily concentrated on a few major partners, particularly those with well-developed pharmaceutical manufacturing capabilities. To further develop its pharmaceutical industry, Vietnam needs not only to diversify its sources of supply to reduce dependency risks, but also to strengthen and upgrade domestic manufacturing capacity in order to participate more deeply in higher value-added segments.

Key Policies and Regulations Supporting the Future Development of Vietnam’s Pharmaceutical Industry

Recent policy developments suggest that Vietnam is not only setting long-term goals for its pharmaceutical industry, but also gradually putting in place the legal and regulatory tools needed to realize them. From industrial development strategies to amendments in the Pharmacy Law and implementing decrees, the policy framework is becoming more specific, execution-focused, and investor-relevant.

| No. | Document name | Effective Date | Main Content | Key highlights | Remarks |

| 1 | Decision 1165/QD-TTg | 09/10/2023 | Approving the National Strategy for the Development of Vietnam’s Pharmaceutical Industry to 2030, with a vision to 2045 | – By 2030:

– By 2045: proactively produce specialty drugs, new drugs, original branded drugs, vaccines, biologics, and pharmaceutical ingredients. |

Creates a long-term policy commitment for segments such as high-quality generics, APIs, vaccines, biologics, and technology transfer, while helping investors clearly see the Government’s priorities in import substitution and increasing localization. |

| 2 | Law 44/2024/QH15 | 01/07/2025; some provisions on extension of marketing authorization and several wholesale-related provisions took effect from 01/01/2025. | An amendment to the Pharmacy Law aimed at attracting investment, enabling new business models, improving drug price transparency, and supporting pharmaceutical industry development.

|

– Establishes a legal framework for pharmaceutical e-commerce.

– Adds pharmacy chains as a separate type of pharmaceutical business model. – Introduces a mechanism for disclosing projected wholesale prices for prescription drugs. – Provides special investment incentives and support for large-scale pharmaceutical projects of at least VND 3,000 billion, focusing on new drugs, original branded drugs, orphan drugs, first generics, high-tech drugs, vaccines, biologics, and pharmaceutical substances. |

This law makes the market more investable by paving the way for omnichannel pharmacy models, supporting M&A and pharmacy chains, and offering particular benefits to investors entering domestic manufacturing, R&D, technology transfer, and high-value medicines. |

| 3 | Decree 163/2025/ND-CP | 01/07/2025 | A decree implementing the amended Pharmacy Law, detailing key conditions, procedures, and regulatory mechanisms for its enforcement. | – Specifies licensing conditions and procedures for several new pharmaceutical business models, such as clinical trial services, bioequivalence testing, and pharmacy chains.

– Establishes a mechanism for disclosing projected wholesale prices for prescription drugs. – Clarifies the legal basis for procedures related to importation, circulation, and pharmaceutical management. |

This decree helps reduce ambiguity in implementation, as compliance requirements, dossiers, and procedures are made clearer. For investors, this is a positive signal because the market is not only opening up in policy terms, but also becoming more concrete in execution. |

B&Company’s synthesis

Strategic Implication for foreign investors

Vietnam presents an increasingly investable pharmaceutical market, not only because demand is rising, but because policy reforms are gradually reducing market-entry barriers and creating clearer incentives for localized, higher-value production. For foreign investors, this means the opportunity is shifting from pure export-to-Vietnam models toward deeper participation in manufacturing, technology transfer, and distribution partnerships.

However, the opportunity is not uniform across the value chain. While Vietnam offers strong growth potential, investors may face challenges in high-value segments due to limited local supporting capacity, continued reliance on imported inputs, and the need to navigate a still-evolving regulatory and compliance environment.

For foreign investors considering entry into Vietnam’s pharmaceutical market, several strategic priorities should be taken into account:

– Focus on high-potential segments such as specialty drugs, biologics, vaccines, high-quality generics, and APIs, where domestic supply gaps remain significant.

– Enter through partnerships such as joint ventures, technology transfer, or selective M&A with local manufacturers and pharmacy chains to reduce entry risks.

– Build local capabilities in manufacturing, regulatory affairs, and market access rather than treating Vietnam solely as a sales market.

– Closely monitor policy implementation, especially in licensing, pricing, e-commerce, and pharmacy chain management, to ensure compliance and scale effectively.

Read more

Pharmaceutical market in Vietnam: Landscape, key players and regulatory overview

Pharmacy chain business situation in Vietnam in 1st quarter 2025: An Khang reports a loss

[1] https://dhgpharma.com.vn/sites/default/files/2025-04/7.%20BC001%20Bao%20cao%20HDQT%20nam%202024%20-%20KH%202025_0.pdf

[2] https://vietnamnews.vn/economy/1733064/pharmaceutical-exports-reach-312-million-viet-nam-ranks-fourth-in-southeast-asia.html

[3] https://www.trade.gov/market-intelligence/vietnam-pharmaceutical-industry-updates

[4] https://baohiemxahoi.gov.vn/tintuc/Pages/linh-vuc-bao-hiem-y-te.aspx?ItemID=26139&CateID=169

[5] https://vnexpress.net/chi-phi-cho-y-te-cua-nguoi-viet-nam-tang-thang-dung-4997605.html

[6] https://vietnamnews.vn/economy/1733064/pharmaceutical-exports-reach-312-million-viet-nam-ranks-fourth-in-southeast-asia.html

[7] https://www.mbs.com.vn/media/iaxk55mz/banle_20243012_eng.pdf

[8] https://vietnamnews.vn/economy/1733064/pharmaceutical-exports-reach-312-million-viet-nam-ranks-fourth-in-southeast-asia.html

[9] https://doanhnghieptiepthi.vn/nam-2025-viet-nam-nhap-khau-gan-43-ty-usd-duoc-pham-161260210151632463.htm

Related article

SUBSCRIBE NEWSLETTER