In Q1 2026, total merchandise trade in Vietnam was up 23% YOY. Exports increased to USD 122.9 billion, while imports rose to USD 126.6 billion.

22Jun2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

Vietnam entered 2026 with a striking trade picture: exports continued to expand strongly, but imports grew even faster, pushing the country back into a trade deficit.

In Q1 2026, total merchandise trade reached USD 249.5 billion, up 23.0% year-on-year. Exports increased by 19.1% to USD 122.9 billion, while imports rose 27.0% to USD 126.6 billion. This resulted in a trade deficit of roughly USD 3.6 billion, reversing the surplus seen in the same period of 2025.

At first glance, this may appear as a weakening external position. However, a closer look reveals a more important story: Vietnam is not slowing down—it is importing aggressively to expand production capacity.

For foreign investors, Q1 2026 reflects a classic “pre-production expansion phase” in a manufacturing-driven economy rather than a demand-driven imbalance.

A deficit driven by investment, not consumption

The most important feature of Vietnam’s import structure is its composition. Production inputs accounted for 93.9% of total imports, while consumer goods made up only 6.1%.

This indicates that import growth is primarily linked to industrial expansion, not household demand. In other words, Vietnam is importing to produce rather than to consume.

The clearest signal comes from foreign-invested enterprises (FDI). Imports by the FDI sector surged 45.3% year-on-year to USD 91.4 billion, while imports by domestic enterprises declined.

This divergence is important. It suggests that most of the import growth is concentrated in global manufacturing value chains—electronics, machinery, components and materials—where FDI firms are expanding capacity or preparing new production cycles.

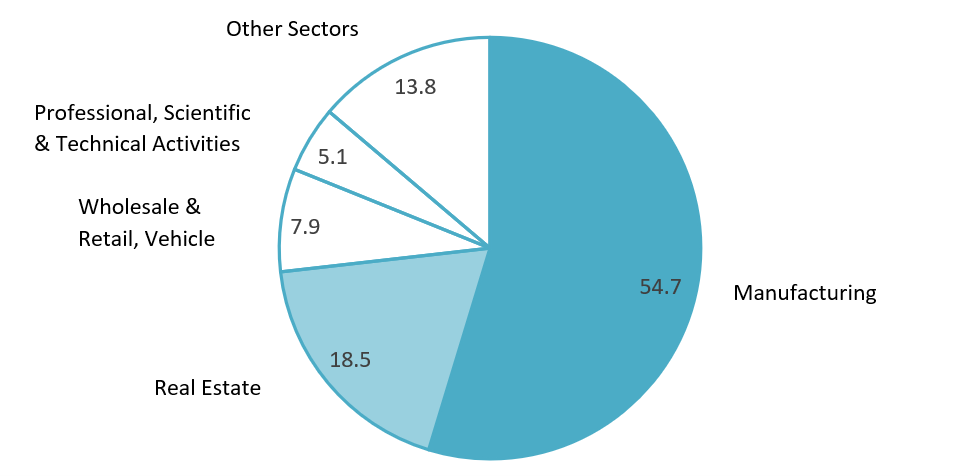

Breakdown of registered FDI in 2025 by sector

Unit: %, 100% = USD 38 billion

Source: FIA Vietnam

In practical terms, imports today often become exports in the next 3–6 months. The deficit is therefore not purely a macro weakness but part of an investment-driven production pipeline.

However, it also highlights a structural issue: Vietnam remains heavily dependent on imported inputs, especially in higher-value manufacturing segments.

Manufacturing expansion is accelerating export complexity

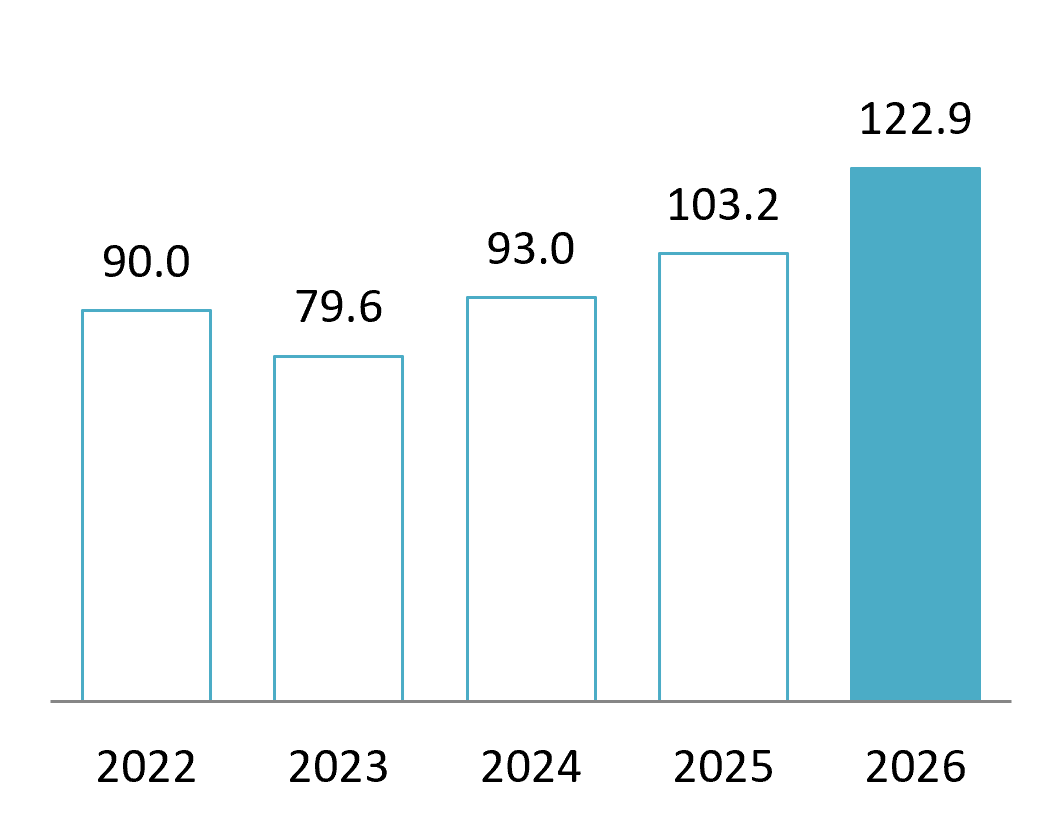

Exports in Q1 2026 reached USD 122.9 billion, with manufactured and processed goods accounting for 89.9% of total export value.

Export value in the first quarter of 2022–2026

Unit: Billion USD

Source: National Statistics Office

Vietnam’s export structure continues to move deeper into electronics and machinery-led industries:

– Electronics, computers and components: ~USD 30.7 billion (+45.5%)

– Phones and components: ~USD 16.7 billion

– Machinery, equipment and spare parts: ~USD 15 billion

Together, these three groups account for roughly half of total exports.

This confirms Vietnam’s position as a critical node in global manufacturing networks, particularly in electronics assembly and industrial production.

However, this growth is not fully supported by domestic supply chains. Imports of electronics and components reached nearly USD 47.6 billion in the same period, significantly exceeding exports of similar categories.

This gap shows Vietnam’s current position in the value chain: strong in assembly, packaging, and export manufacturing, but still reliant on imported semiconductors, components, and advanced materials.

For investors, this creates two layers of opportunity:

First, continued investment in final manufacturing and assembly for export markets.

Second, and increasingly important, is investment in supporting industries that supply this manufacturing base.

These include:

– Electronic components and precision parts

– Industrial automation and machinery

– Testing, inspection, and quality control services

– Industrial logistics and supply chain solutions

– Local supplier development and technical upgrading

The second category is becoming more strategically important as Vietnam’s export scale grows.

Trade structure reflects a dual dependence model

Vietnam’s trade geography remains highly concentrated.

The United States remains the largest export destination, with USD 39.0 billion in Q1 2026 exports. Demand from the US continues to anchor Vietnam’s electronics, machinery, and consumer goods exports.

On the import side, China dominates supply, accounting for approximately USD 50.1 billion, followed by South Korea at USD 18.7 billion.

This creates a structural “dual dependency”:

– Export demand is driven by developed markets (US, EU, Japan)

– Import supply is concentrated in Asia (China, Korea, Taiwan)

This model has supported rapid growth but also introduces vulnerability. Any disruption in upstream supply chains or downstream export demand directly affects Vietnam’s industrial cycle.

For foreign investors, this structure has two implications.

First, Vietnam is highly integrated into global trade flows, making it attractive as an export platform.

Second, supply chain resilience and sourcing strategy become critical success factors when operating in Vietnam.

Companies entering Vietnam increasingly need a supply chain design strategy, not just a manufacturing footprint.

FDI continues to dominate exports—and shape industrial direction

FDI enterprises remain the backbone of Vietnam’s export economy.

In Q1 2026, FDI firms generated USD 98.5 billion in exports, accounting for 80.1% of the national total. Export growth in this segment reached 33.3% year-on-year.

By contrast, the domestic sector’s exports declined significantly.

This widening gap reinforces a key structural characteristic of Vietnam’s economy: export competitiveness is heavily driven by multinational corporations rather than domestic industrial champions.

The implication for investors is twofold.

On one hand, Vietnam offers a highly efficient export platform supported by global corporations with established supply chains. On the other hand, local industrial depth remains uneven, especially in high-precision manufacturing and upstream components.

This creates an environment where foreign investors are not only exporters but also ecosystem builders.

Companies that develop local suppliers, training systems, and production capabilities tend to gain stronger long-term efficiency advantages.

Key developments shaping the investment environment in Q1 2026

Strong FDI inflows continue

Registered FDI reached approximately USD 15.2 billion, up 42.9% year-on-year, while disbursed capital increased to USD 5.4 billion.

This reflects continued investor confidence, particularly in manufacturing, electronics, and infrastructure-related sectors.

Production cycle remains in expansion mode

Vietnam’s manufacturing PMI remained above 50 throughout the quarter, indicating continued expansion in output and new orders, although momentum softened slightly toward March.

This aligns with rising imports of machinery and components, suggesting ongoing capacity expansion rather than contraction.

Cost pressure is increasing

Manufacturers reported rising input and logistics costs, particularly in energy and transportation. In several cases, orders were accelerated to hedge against future cost increases.

For investors, this signals that Vietnam’s cost advantage should no longer be viewed as static. Operational efficiency and supply chain design are becoming more important than wage differentials alone.

Technology-linked trade is expanding faster than local capability

Growth in electronics exports is accelerating faster than domestic supply chain development. This gap between export output and local input capacity is widening.

This trend represents one of the most important medium-term investment opportunities in Vietnam: upgrading local supporting industries.

What should foreign investors conclude?

Vietnam’s trade performance supports a positive investment outlook, but the headline growth rate should not be considered in isolation.

First, investors should determine where they can participate in the manufacturing ecosystem. Opportunities may be particularly strong in components, industrial services, automation, logistics and supplier development.

Second, location selection should be based on access to customers, ports, supplier clusters, infrastructure and skilled labour—not only land or wage costs.

Third, investors should build a sourcing strategy that balances imported inputs with progressive localization. Full localization may not be immediately feasible, but excessive reliance on one country or supplier can create operational and trade-related risks.

Finally, companies should pay closer attention to origin documentation, supply-chain transparency and local value creation. As Vietnam’s exports to major markets increase, manufacturers are likely to face greater scrutiny regarding where products and components are actually produced.

B&Company supports foreign investors through market assessment, sector and supply-chain analysis, location studies, customer and supplier research, and local partner searches in Vietnam. These services can help companies identify where they can participate most effectively in Vietnam’s evolving trade and manufacturing ecosystem.

Read more

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 1,000,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 28 3910 3913 |

Related article

SUBSCRIBE NEWSLETTER