25/01/2024

Đánh giá ngành / Tin tức & Báo cáo mới nhất

Bình luận: Không có bình luận.

Thị trường bảo hiểm nói chung và bảo hiểm nhân thọ nói riêng tại Việt Nam đã trải qua một cuộc khủng hoảng vào năm 2023. Không chỉ phải đối mặt với suy thoái kinh tế chung, ngành bảo hiểm còn phải đối mặt với khủng hoảng truyền thông và mất lòng tin của khách hàng. Điều này càng làm gia tăng tác động đáng kể đến toàn bộ ngành. Tuy nhiên, ngành bảo hiểm đã từng bước vượt qua những thách thức này, tái cấu trúc để nâng cao chất lượng dịch vụ.

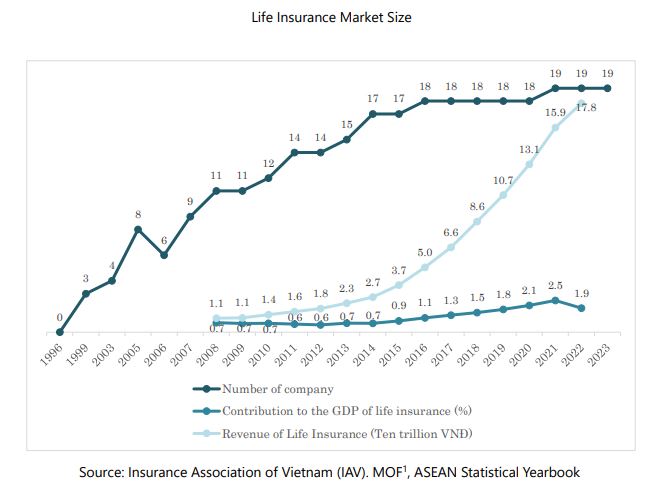

Thị trường bảo hiểm nhân thọ Việt Nam đã mở rộng đều đặn kể từ khi tự do hóa vào năm 1999, ngay cả trong cuộc khủng hoảng tài chính. Trước đây, Bảo Việt (https://www.baoviet.com.vn/insurance/ )thống trị thị trường với tư cách là công ty bảo hiểm duy nhất. Thị trường mở rộng với sự tham gia của vốn nước ngoài, với tám công ty bảo hiểm vào năm 2005 và tính đến tháng 5 năm 2023, Việt Nam có 19 công ty bảo hiểm nhân thọ

Nhìn lại cuộc khủng hoảng kinh tế năm 2013, toàn thị trường bảo hiểm tiếp tục tăng trưởng 14% (trong đó bảo hiểm phi nhân thọ tăng 7% và bảo hiểm nhân thọ tăng mạnh 23%). Tuy nhiên, tính đến tháng 11/2023, thị trường bảo hiểm phi nhân thọ chỉ tăng trưởng khiêm tốn 2%, trong khi bảo hiểm nhân thọ giảm 11,6%. Tuy nhiên, sau 10 năm, quy mô thị trường bảo hiểm tại Việt Nam đã mở rộng đáng kể, doanh thu bảo hiểm nhân thọ tăng hơn 6 lần, toàn ngành bảo hiểm đã tái đầu tư vào nền kinh tế, ước đạt 757.652 nghìn tỷ đồng, tăng khoảng 13% so với cùng kỳ năm ngoái.[2]

Nhìn lại cuộc khủng hoảng kinh tế năm 2013, toàn thị trường bảo hiểm tiếp tục tăng trưởng 14% (trong đó bảo hiểm phi nhân thọ tăng 7% và bảo hiểm nhân thọ tăng mạnh 23%). Tuy nhiên, tính đến tháng 11/2023, thị trường bảo hiểm phi nhân thọ chỉ tăng trưởng khiêm tốn 2%, trong khi bảo hiểm nhân thọ giảm 11,6%. Tuy nhiên, sau 10 năm, quy mô thị trường bảo hiểm tại Việt Nam đã mở rộng đáng kể, doanh thu bảo hiểm nhân thọ tăng hơn 6 lần, toàn ngành bảo hiểm đã tái đầu tư vào nền kinh tế, ước đạt 757.652 nghìn tỷ đồng, tăng khoảng 13% so với cùng kỳ năm ngoái.[2]

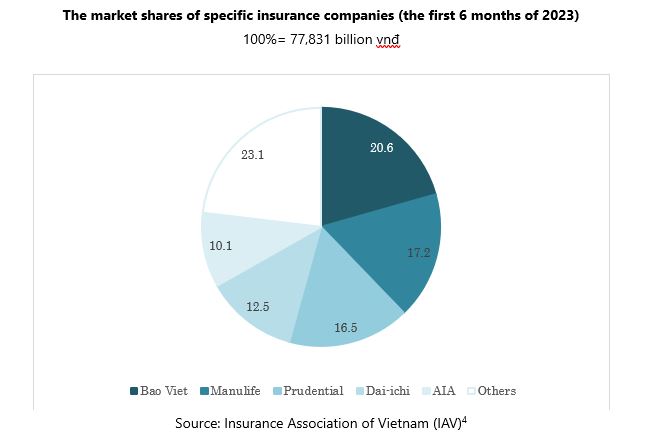

Xét trong 6 tháng đầu năm 2023, số lượng hợp đồng bảo hiểm phát hành mới trong 6 tháng đầu năm 2023 đạt 1.028.402 hợp đồng (sản phẩm chính), giảm 31,3% và tổng doanh thu phí bảo hiểm toàn thị trường ước đạt 77.831 nghìn tỷ đồng, giảm 7,9% so với cùng kỳ năm ngoái. Sự sụt giảm về số lượng hợp đồng mới và doanh thu phí bảo hiểm nhân thọ trên toàn thị trường là hệ quả của sự mất lòng tin bắt nguồn từ cuộc khủng hoảng gần đây. Nhiều khách hàng đã khiếu nại do các vụ việc liên quan đến tiền gửi tiết kiệm và đầu tư được chuyển đổi thành hợp đồng bảo hiểm hoặc khoản vay tín dụng và họ đã bị ép buộc mua bảo hiểm nhân thọ thông qua nhiều chiêu trò khác nhau[3].

Bảo Việt tiếp tục duy trì vị thế dẫn đầu thị trường trong lĩnh vực bảo hiểm nhân thọ với thị phần 20,1%. Tuy nhiên, theo sát là hai đơn vị có thị phần khá sát sao là Manulife (17,2%) và Prudential (16,5%), tiếp theo là Dai-ichi (12,5%) và AIA (10,1%). Theo sau top 5 là 14 công ty, cùng nhau chia sẻ tổng thị phần là 23,1%.

Ở một mức độ nào đó, sự vào cuộc của lãnh đạo Chính phủ có vai trò ổn định thị trường bảo hiểm. Bộ Tài chính cũng đã trình Chính phủ nhiều luật để điều chỉnh, giám sát, thanh tra hoạt động kinh doanh trong ngành bảo hiểm, ví dụ như Luật Kinh doanh bảo hiểm số 08/2022/QH15 và các Nghị định liên quan như Nghị định số 46/2023/NĐ-CP, Nghị định số 67/2023/NĐ-CP

Ở một mức độ nào đó, sự vào cuộc của lãnh đạo Chính phủ có vai trò ổn định thị trường bảo hiểm. Bộ Tài chính cũng đã trình Chính phủ nhiều luật để điều chỉnh, giám sát, thanh tra hoạt động kinh doanh trong ngành bảo hiểm, ví dụ như Luật Kinh doanh bảo hiểm số 08/2022/QH15 và các Nghị định liên quan như Nghị định số 46/2023/NĐ-CP, Nghị định số 67/2023/NĐ-CP

Năm 2024 vẫn được dự báo là một năm đầy thách thức đối với nền kinh tế nói chung và ngành bảo hiểm nói riêng. Tuy nhiên, đây cũng là cơ hội để các công ty bảo hiểm nhân thọ phát triển cả về chiều sâu và chiều rộng, nâng cao năng lực cạnh tranh để tồn tại trên thị trường. Đây chính là quá trình của thị trường giúp thúc đẩy thị trường phát triển lành mạnh và hiệu quả [5] . Hiện nay, dân số Việt Nam đang già hóa nhanh chóng, dẫn đến nhu cầu về các gói bảo hiểm phù hợp với người cao tuổi. Nhóm này có nhu cầu và nhận thức về bảo hiểm, nhưng hiện nay, họ đang gặp khó khăn trong việc tham gia [6] . Các công ty bảo hiểm nên đưa ra các sản phẩm chuyên biệt và mở rộng quy trình thẩm định cho những khách hàng mắc các bệnh lý như tiểu đường, cholesterol cao, huyết áp cao, v.v. Ngoài ra, nên mở rộng các gói bảo hiểm đặc biệt để giải quyết nhu cầu của những cá nhân khuyết tật hoặc có vấn đề về sức khỏe tâm thần. Hiện nay, những cá nhân có bệnh lý nền gặp khó khăn trong việc tiếp cận các gói bảo hiểm do mức độ rủi ro cao đi kèm. Theo quy định của pháp luật về bảo hiểm, những hồ sơ này thường bị các công ty bảo hiểm từ chối.

Bài viết này đã được đăng trong chuyên mục “Đọc xu hướng Việt Nam” của ASEAN Economic News. Vui lòng xem bên dưới để biết thêm thông tin

|

Công ty TNHH B&Company Công ty nghiên cứu thị trường của Nhật Bản đầu tiên tại Việt Nam từ năm 2008. Chúng tôi cung cấp đa dạng những dịch vụ bao gồm báo cáo ngành, phỏng vấn ngành, khảo sát người tiêu dùng, kết nối kinh doanh. Ngoài ra, chúng tôi đã phát triển cơ sở dữ liệu của hơn 900,000 công ty tại Việt Nam, có thể được sử dụng để tìm kiếm đối tác kinh doanh và phân tích thị trường. Xin vui lòng liên hệ với chúng tôi nếu bạn có bất kỳ thắc mắc hay nhu cầu nào. info@b-company.jp + (84) 28 3910 3913 |

Đọc các bài viết khác

[/vc_column_text][/vc_column][/vc_row]

- Tất cả

- Hành chính

- Nông nghiệp

- Phát sóng / Báo chí

- Xây dựng & Bất động sản

- Tư vấn

- Kinh tế

- Giáo dục & Đào tạo

- Giải trí & Truyền thông

- Thực phẩm & Đồ uống

- Chăm sóc sức khỏe

- Khu công nghiệp

- Đầu tư

- CNTT & Công nghệ

- Bán lẻ & Phân phối

- Hội thảo

- Du lịch & Khách sạn

- Buôn bán