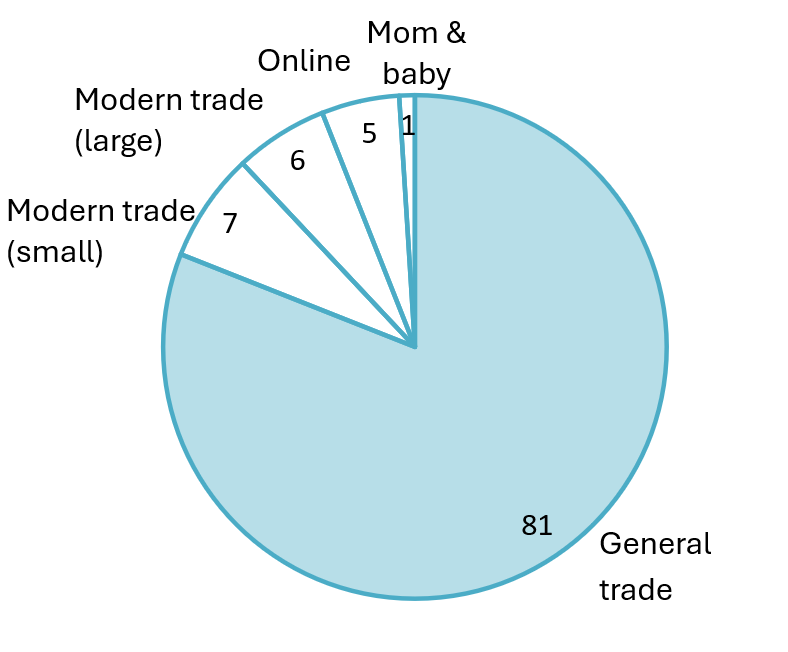

The scale of Vietnam's general trade network remains remarkable, with a contribution nationwide of up to 81% to the FMCG sales.

15May2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

Vietnam’s General Trade (GT) channel — the sprawling network of neighborhood grocery stores, small distributors, and independent agents that has long been the backbone of FMCG distribution — is entering one of its most consequential restructuring phases. Driven by an unprecedented tax policy overhaul taking effect in 2026, a relentless squeeze from modern trade formats and e-commerce, and tightening consumer wallets, the GT landscape is set for a significant “filtering” that will reshape how brands reach Vietnamese consumers. This article examines what is happening, why it matters, and what businesses and researchers can expect beyond 2026.

The GT channel: Still dominant, but under pressure

The scale of Vietnam’s general trade network remains remarkable. According to Nielsen IQ, GT still accounts for 70% of total retail activity, with a contribution nationwide of up to 81% to the FMCG sales [1].

FMCG sales by channels (2025)

|

Sales growth

|

Source: NIQ

Yet the cracks are widening. General trade commands a large amount of offline FMCG sales by value, yet posted just 1% growth in 2025, while online channels surged 20% on only 5% of total sales. Modern trade, which includes organized formats like supermarkets, convenience stores, and mini markets, grew 6 – 9 times the GT rate. The data confirms the structural alarm: the GT channel retains its scale dominance today, but the growth engine has decisively shifted to modern trade and E-commerce. Meanwhile, the GT channel is facing a new and more structural challenge: fiscal formalization.

For decades, Vietnam’s household businesses paid taxes under a “lump-sum” model, where tax authorities simply assigned a fixed annual tax figure. This system was administratively easy but notorious for opacity, with significant underreporting of actual revenues. That era is now over.

On May 4, 2025, the Politburo issued Resolution 68-NQ/TW on private economic development, which required the abolition of the lump-sum tax method for business households no later than 2026. Resolution 198/2025/QH15 made this effective from January 1, 2026, with household businesses now required to self-declare, self-calculate, and self-pay taxes based on actual revenue.

Recently, the revised Vietnam household business tax raised the tax-exempt revenue threshold from 100 million VND to 1 billion VND per year, 10 times the initial level, meaning around 235,800 businesses benefited with 2.164 trillion VND corporate income tax exempted in total [2]. The new system classifies operators into four tiers based on annual revenue, each carrying a distinct compliance burden:

Table 1. Vietnam household business Tax classification updated on 29 April, 2026

| Group 1 | Group 2 | Group 3 | Group 4 | |

| Annual Revenue | ≤1B VND (~38K USD) | Over 1B – 3B VND (38K~115K USD) | Over 3B – 50B VND (115K~1.9M USD) | Over 50B VND (~1.9M USD) |

| VAT | ✗ Exempt | Calculation based on revenue

(% VAT rate × specified revenue) |

||

| Pay quarterly | Pay quarterly | Pay monthly | ||

| Personal Income Tax (PIT) | ✗ Exempt | § Option 1: (Revenue − Expenses) × 15%

§ Option 2: (Revenue – Taxable threshold) × PIT Rate |

(Revenue − Expenses) × 17% | (Revenue − Expenses) × 20% |

| E-Invoice | Encouraged | Mandatory | ||

| Accounting system | Simple account book | Full accounting books – micro/small enterprise or household business standard | ||

B&Company compiled from Law Library [3] and Government Electronic Newspaper [4]

The compliance burden still exists, especially for middle tiers. A VCCI survey found that more than 70% of household businesses are concerned about complex procedures; nearly 70% fear the risk of penalties; over 60% consider compliance costs high and worry about not being able to keep up with regulatory updates [5]. For small grocery stores operators already running on thin margins, the added administrative load of digital accounting, e-invoice software, and quarterly tax filings may simply tip the economics toward closure.

Key factors narrowing the General Trade channel besides tax

The decline of Vietnam’s General Trade channel is not a single-cause story. Tax formalization in 2026 acts as a pressure accelerator — but the structural erosion has been building for years, driven by three forces that are reshaping why and how Vietnamese consumers shop.

Rising household incomes are changing shopping expectations:

Vietnam’s middle class has expanded rapidly, with the estimation of 74% Vietnamese population entering the consuming class in 2030, rising from 40.8% in 2020[6]. As incomes rise, shoppers increasingly prioritize product variety, hygiene standards, price transparency, and the overall shopping experience, criteria that the average grocery store, with its narrow assortment and informal environment, struggles to meet. Higher-income households are not abandoning convenience; they are simply raising the bar for what “convenient” means.

Modern trade formats are winning the convenience battle:

Mini-marts and convenience store chains, like WinMart+, Circle K, GS25, FamilyMart, etc. have aggressively expanded into residential neighborhoods, directly overlapping with the grocery store’s traditional catchment. These formats offer air-conditioned shopping, standardized pricing, loyalty programs, and extended hours. For the neighborhood shopper, the marginal effort difference between a grocery store and a nearby convenience store has nearly disappeared, but the experience gap has not.

Online shopping is redefining “cheap and easy”:

Platforms like Shopee, TikTok Shop, and Lazada have made home delivery faster and often cheaper than buying in-store, particularly for packaged FMCG staples. Younger shoppers increasingly default to apps for routine purchases, eroding the traditional grocery store’s core transaction: the small, frequent, proximity-driven top-up buy.

In this context, the 2026 tax reform is less a disruption than a formalization of pressures already in motion — one that may, for some marginal operators, become the administrative threshold that tips the decision to close.

Forecasting outlet contraction post-2026: A “natural filter” in action

The question is no longer whether GT outlet numbers will contract, but whether contraction will accelerate, and what emerges on the other side.

The precedent from adjacent sectors is instructive. The first half of 2025 saw over 50,000 F&B outlets close across Vietnam, with total numbers falling 7.1% year-on-year, and declines exceeding 11% in both Hanoi and Ho Chi Minh City. The GT channel faces a comparable convergence of pressures: rising compliance costs from the 2026 tax reform, sustained competition from convenience chains, and an accelerating shift of routine purchases to online platforms. For mid-tier operators — those earning VND 1–3 billion annually and newly subject to full VAT, PIT, and e-invoice obligations — the margin math after formalization may simply not work. In absolute terms, if even 15–20% of the roughly 1.4 million GT outlets exit or consolidate over the next three years, that represents 200,000–280,000 fewer active points of sale — a significant reshaping of how FMCG brands reach Vietnamese consumers at the last mile.

Yet contraction does not mean collapse, and the same pressures accelerating closures are simultaneously pushing surviving operators toward more sustainable models. Several transformation pathways are already visible:

Digitized restocking via B2B platforms:

The applications like OneShop (formerly named VinShop), POS365, Sapo, etc. enable grocery store owners to order products directly at discounted prices, digitizing supply chains (purchasing, shipping, inventory and financial management, etc.) and improving margins for compliant operators.

Some small businesses switched to digital retail platforms to integrate their management processes

Hybrid GT-MT formats:

Programs like MM Mega Market’s “Good Price” project[7], which helps investors transform traditional grocery stores into modern retail models, helping independent grocery owners upgrade their store layouts, planograms, and supplier terms to meet modern trade standards — effectively creating a third category between informal grocery stores and organized retail chains. Similarly, Saigon Co.op and Aeon Vietnam’s development of modern grocery formats, including assisting local, small-scale producers in reaching international standards, is creating a pathway for formalization rather than extinction.

Distributor consolidation:

As smaller agents exit, mid-sized distributors are absorbing their routes and retail accounts, building scale that makes compliance and investment in sales force automation more economically viable.

The GT channel of 2028 will likely be smaller in outlet count but structurally stronger in the outlets that remain: better-stocked, digitally connected, and formally compliant. For FMCG brands, that shift cuts both ways, fewer doors to call on, but each door backed by more reliable data and more predictable ordering behavior.

How B&Company can support

Navigating the GT restructuring requires more than macro analysis — it demands local knowledge. With 15+ years on the ground in Vietnam, B&Company offers the full toolkit brands and distributors need to navigate GT restructuring:

– Enterprise-level quantitative trade surveys to track outlet counts and channel health by province;

– In-depth interviews and ethnographic shop-alongs with grocery owners and distributors to understand the real economics behind closures and platform adoption;

– Mystery shopping to monitor brand visibility and stock compliance at the outlet level;

– Market entry feasibility studies for brands rethinking their distribution strategy post-2026;

– and Access to the Vietnam Enterprise Database — 1,000,000+ enterprises mapped to district and ward level, for pinpointing at-risk distribution nodes.

As the filtering wave accelerates beyond 2026, the brands that will win in Vietnam’s general trade channel are those that understand the channel not as a static map, but as a living system under transformation. Precise, timely research is the foundation of that understanding.

Read more

Increase of the middle class in rural areas of Vietnam: The driver for modern retail

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 1,000,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 28 3910 3913 |

[1] https://en.vneconomy.vn/structural-bottlenecks-to-vietnams-retail-market.htm

[2] https://thoibaotaichinhvietnam.vn/chinh-phu-duoc-quyet-dinh-nguong-doanh-thu-mien-thue-du-kien-1-ty-dongnam-196307.html

[3] https://thuvienphapluat.vn/ma-so-thue/phap-luat-thue/cach-tinh-thue-cho-4-nhom-ho-kinh-doanh-tu-nam-2026-396377-218030.html

[4] https://xaydungchinhsach.chinhphu.vn/toan-van-nghi-dinh-so-141-2026-nd-cp-nang-nguong-doanh-thu-khong-phai-chiu-thue-len-1-ty-dong-119260504154326455.htm

[5] https://en.vcci.com.vn/vcci-news/vcci-prioritize-reducing-the-complexity-of-tax-accounting-and-e-invoice-regulations-for-household-businesses-117075

[6] https://www.mckinsey.com/~/media/mckinsey/featured insights/future of asia/insights/the new faces of the vietnamese consumer/the-new-faces-of-the-vietnamese-consumer-vt.pdf

[7] https://vietnamnews.vn/economy/1717713/grocery-stores-embrace-new-look-strengthening-support-for-manufacturers.html

Related article

SUBSCRIBE NEWSLETTER