As Middle East tensions spread, China occupies a pivotal position: as both a major energy consumer and the world’s largest manufacturing hub.

23Apr2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

The latest escalation in the Middle East is no longer merely a regional geopolitical crisis. As tensions spread across key maritime and energy corridors, the shock is being transmitted directly into the global supply chain through higher energy costs, rising freight rates, longer delivery times, and mounting uncertainty for manufacturers worldwide. In this context, China occupies a pivotal position: as both a major energy consumer and the world’s largest manufacturing hub, it has become the principal transmission channel through which a regional conflict can evolve into a global supply chain disruption.

The Middle East conflict and its impact on global supply chains

Viewed through the lens of supply chains, the Middle East conflict is not simply a geopolitical flashpoint, but a direct shock to some of the most critical arteries of global trade. As tensions have spread to the Strait of Hormuz, a maritime corridor that carries roughly one quarter of the world’s seaborne crude oil, as well as significant volumes of natural gas and fertilizers, the consequences of the conflict have rapidly extended far beyond the region itself[1]. What is now at risk is not only the flow of energy, but the entire cost structure underpinning production, transportation, and distribution on a global scale. In modern supply chains, energy is not an external variable; it is a foundational input that shapes nearly every stage of operations[2].

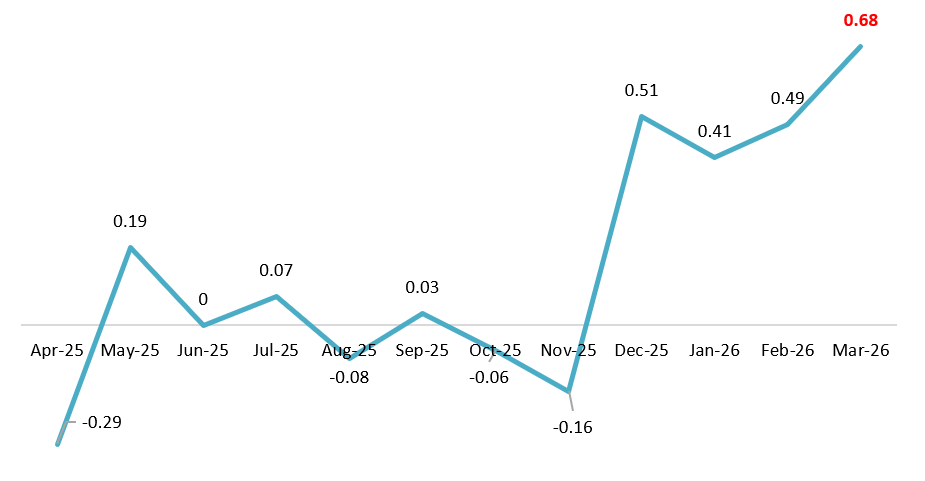

From this chokepoint, the shock propagates in a clear sequence. Disruptions to oil and gas flows push up fuel costs first, then spread to freight rates, insurance premiums, warehousing expenses, and, ultimately, production costs[3]. For this reason, the impact of the current Middle East conflict goes well beyond delays in cargo flows; it is making global supply chains more expensive, more fragile, and more vulnerable to subsequent shocks. The IMF has warned that the conflict could push the global economy toward higher prices and slower growth. At the same time, UNCTAD projects that global merchandise trade growth in 2026 could slow to around 1.5 to 2.5 percent[4], while the New York Fed’s Global Supply Chain Pressure Index rose to 0.68 in March, its highest level since early 2023[5].

Global Supply Chain Pressure Index (April 2025 – March 2026)*

Source: Mtsinsights

(*) The index is normalized around its historical average. A value of 0 indicates supply chain pressure is at its average level; a value above 0 indicates pressure is higher than normal; and a value below 0 indicates pressure is lower than normal. The further the index rises above 0, the greater the disruption and cost pressure across supply chains; conversely, the further it falls below 0, the more easing and normalization in supply chain conditions it generally suggests.

Why China is the central transmission point

If the Middle East conflict has revealed how a shock can spread from the Strait of Hormuz into energy prices, transportation, and production costs, then China is the most important transmission point through which that shock is passed on. This is because China is not only a massive energy consumer, but also heavily dependent on oil flows from the Middle East. According to the IEA, China is currently the largest Asian buyer of Middle Eastern crude passing through Hormuz, accounting for 37 percent of total exports through the strait, equivalent to more than 5.2 million barrels per day. Oil from the Gulf alone represents more than half of China’s seaborne oil imports[6].

China’s total oil demand is also expected to continue rising, from 14.2 million barrels per day in 2019 to a projected 17 million barrels per day in 2026. Importantly, this growth is not being driven primarily by conventional gasoline demand, but increasingly by naphtha, a key feedstock for petrochemicals and industrial production. This suggests that when turmoil in the Middle East unsettles energy markets, the pressure is likely to be transmitted not only through oil prices but directly into China’s manufacturing base and industrial supply chains.

However, China stands at the center of the domino effect not only because it imports large volumes of energy, but also because it remains the world’s central manufacturing hub. The WTO reports that China’s merchandise exports reached USD 3.77 trillion in 2025, accounting for 14.4 percent of global merchandise trade and contributing roughly 30 percent of global export growth. China also remains a leading supplier of electronics and intermediate goods for regional production networks[7].

This central role is further reinforced in strategic industries. In 2025, China’s exports of high-tech products rose by 13.2 percent year on year. Exports of specialized equipment, high-end machine tools, and industrial robots increased by 20.6 percent, 21.5 percent, and 48.7 percent, respectively. In green industries, exports of lithium batteries and wind turbines surged by 26.2 percent and 48.7 percent, while exports of electric motorcycles and electric bicycles rose by 18.1 percent[8].

In sectors such as electric vehicle batteries and solar power, concentration is even more pronounced. The IEA notes that China accounts for nearly 80 percent of global EV battery production, close to 85 percent of cathode materials, more than 90 percent of anode materials, and over 80 percent of manufacturing capacity across all major stages of the solar PV supply chain. As a result, shocks passing through China rarely stop at its borders; they are often transmitted outward through higher input costs, longer lead times, and heightened risks of supply shortages in industries that depend heavily on Chinese output[9].[10]

How the domino effect from China spreads across global supply chains

The domino effect from China does not usually begin with immediate product shortages. It tends to emerge first through rising costs and mounting delays across supply chains. When the Middle East conflict drives up energy prices, freight rates, and insurance premiums, those pressures feed into China’s production costs and are then transmitted into export prices and global supply networks. At the same time, greater transport risk lengthens delivery times, disrupts production planning, and forces firms to maintain higher safety inventories. Given China’s role as one of the world’s largest supply hubs, any change in cost structures or lead times within China can quickly trigger ripple effects across industries deeply dependent on Chinese supply, including electronics, machinery, automobiles, batteries, and solar energy.

There are already visible signs that cost pressures in China are moving beyond raw material markets and into firms themselves. In electronics, Kingboard Laminates, the world’s largest producer of copper-clad laminates, raised prices three times in just three months, with increases of around 10 percent for both materials and processing[11]. In the automotive sector, electric vehicle maker NIO stated that memory chip shortages and higher raw material prices could increase EV production costs by 6,000 to 10,000 yuan per vehicle[12]. In the battery supply chain, pressure has become evident as Chinese cathode material suppliers have sought price adjustments, with discounts relative to spot cobalt sulfate narrowing from around 10 percent to 5 percent, while cobalt prices rose from roughly USD 10 per pound to nearly USD 24 per pound during 2025[13]. In solar energy, a roughly 130 percent increase in silver prices over 12 months has driven solar panel production costs up by 7 to 15 percent.[14]

Which markets are likely to be most affected?

ASEAN is likely to be the first region to feel the impact of the domino effect from China, as it is currently China’s largest trading partner and is deeply integrated with China in manufacturing supply chains. If production, energy, or logistics costs rise in China, economies such as Vietnam, Thailand, and Malaysia are likely to face higher component prices, longer delivery times, and greater risks for assembly-based industries, especially electronics and industrial equipment[15] .

In Vietnam, China is currently the country’s largest import market. In the first quarter of 2026, Vietnam’s imports from China reached USD 50.1 billion, up 34.4 percent year on year, mainly consisting of intermediate goods and capital goods, particularly machinery, equipment, and spare parts[16]. Therefore, any disruption affecting the flow of exports from China to Vietnam is unlikely to primarily reduce consumer goods imports; rather, it would first increase both costs and uncertainty surrounding the supply of components, machinery, and raw materials used by factories in Vietnam, thereby putting pressure on production planning, delivery reliability, and export competitiveness.

Northeast Asia, particularly South Korea and Japan, is also highly vulnerable because both economies are closely linked to China in technology supply chains while remaining dependent on strategic inputs that China controls. If the shock is transmitted through China, South Korea is likely to be more exposed in semiconductors, batteries, and petrochemicals, while Japan may face greater pressure in automobiles, high-tech components, and strategic materials such as rare earths.[17] [18]

Europe, especially Germany, is another market likely to be significantly affected at the high-value industrial level. China continues to play a major role in supplying electronics, intermediate goods, and a wide range of strategic products to the European market. As a result, any increase in costs or delivery times in China could affect Europe not only through higher import prices but also through direct disruptions to core manufacturing sectors such as machinery, automobiles, chemicals, and industrial equipment.[19] [20]

Conclusion

The Middle East conflict demonstrates how a regional geopolitical crisis can rapidly evolve into a global supply chain shock when it strikes key energy and transport corridors. Yet the full scale of that shock becomes visible only when it passes through China, where rising energy costs and logistics risks are transformed into higher production costs, longer lead times, and broader instability across industrial networks. In this sense, China is not the source of the crisis, but the central channel through which a regional disruption can become a global domino effect.

Read more

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 900,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 28 3910 3913 |

[1] https://www.iea.org/about/oil-security-and-emergency-response/strait-of-hormuz

[2] https://unctad.org/system/files/official-document/osgttinf2026d1_en.pdf

[3] https://www.reuters.com/world/middle-east/war-middle-east-will-lead-slower-growth-higher-inflation-imf-chief-tells-reuters-2026-04-06/

[4] https://unctad.org/news/hormuz-disruption-deepens-global-economic-strain-across-trade-prices-and-finance

[5] https://www.mtsinsights.com/events/4091/

[6] https://iea.blob.core.windows.net/assets/a25ddf53-cd6c-4910-ac90-16bfd28399e7/-12MAR2026_OilMarketReport.pdf

[7] https://www.wto.org/english/res_e/booksp_e/gtos0326_e.pdf

[8] https://english.www.gov.cn/archive/statistics/202601/15/content_WS6968cbfac6d00ca5f9a08969.html

[9] https://iea.blob.core.windows.net/assets/4eedd256-b3db-4bc6-b5aa-2711ddfc1f90/SpecialReportonSolarPVGlobalSupplyChains.pdf

[10] https://iea.blob.core.windows.net/assets/7ea38b60-3033-42a6-9589-71134f4229f4/GlobalEVOutlook2025.pdf

[11] https://vnbusiness.vn/gia-linh-kien-tang-gay-hieu-ung-domino-tren-thi-truong-dien-tu.html

[12] https://www.reuters.com/world/asia-pacific/chinas-nio-targets-overseas-sales-thousands-cars-this-year-2026-03-11/

[13] https://www.reuters.com/world/asia-pacific/chinese-battery-material-makers-push-higher-prices-cobalt-rally-hits-supply-2025-11-14/

[14] https://www.reuters.com/sustainability/climate-energy/solar-industry-accelerates-shift-silver-costs-soar-2026-02-19/

[15] https://english.www.gov.cn/archive/statistics/202601/15/content_WS6968cbfac6d00ca5f9a08969.html

[16] https://www.nso.gov.vn/du-lieu-va-so-lieu-thong-ke/2026/04/xuat-nhap-khau-viet-nam-tang-truong-truoc-bien-dong-toan-cau/

[17] https://www.reuters.com/world/asia-pacific/japan-says-chinas-dual-use-export-ban-unacceptable-rare-earths-crosshairs-2026-01-07/

[18] https://www.reuters.com/world/asia-pacific/south-korea-seeks-closer-china-cooperation-secure-critical-mineral-supply-chains-2026-02-05/

[19] https://tradingeconomics.com/germany/imports/china/electrical-electronic-equipment

[20] https://www.destatis.de/EN/Press/2026/02/PE26_056_51.html

Related article

SUBSCRIBE NEWSLETTER