Different rental prices among Hanoi districts reflect evolving consumer clusters, infrastructure development, and lifestyle preferences.

24Feb2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

Hanoi’s retail leasing market has undergone a significant transformation over the past decade. In the 2010s, leasing activity was highly concentrated in the historic core—particularly Hoan Kiem and Ba Dinh—where strong occupancy rates and rising rental prices reflected robust retail demand and growing household consumption. By 2025, however, the market structure will have become more complex. District-level differences in rental pricing now reflect evolving consumer clusters, infrastructure development, and shifting lifestyle preferences. These shifts, together with urban development and regulatory standardization, signal a more selective but opportunity-rich environment for foreign F&B investors entering or expanding in Hanoi.

Hanoi Leasing Market Overview: District-Level Differences and Structural Shifts

Historical Pricing Context and Market Framework

In the mid-to-late 2010s (around 2017), Hanoi’s retail leasing market reached its highest occupancy rate (at 95%) and rental prices were up from 7USD to 45USD per sqm compared with the previous five years. The main reason for the rise of Hanoi’s retail leasing market is due to the strong retail sales growth, with 8.1% rise year – on – year (2017) in retail sales revenue, along with a fast-paced growing personal consumption in Vietnam. These macroeconomic fundamentals have strongly reinforced the retail demand, especially in core districts, where landlords can concentrate in commercial activity to maintain high occupancy rates and rental prices [1].

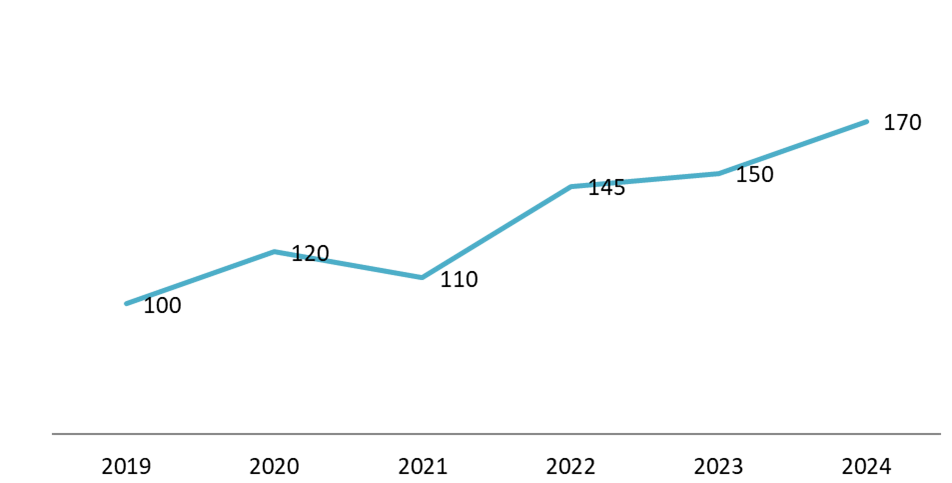

By 2025, Hanoi’s retail leasing landscape has become more structurally differentiated compared to the pre-pandemic period. Between 2019 and 2024, prime retail rents in Hanoi’s CBD increased significantly, rising from approximately USD 100 per sqm per month in 2019 to around USD 170 per sqm per month in 2024. While the market experienced temporary pressure during 2020–2021 due to COVID-19 disruptions, rental levels stabilized and gradually recovered from 2022 onward, supported by improving retail sales performance and renewed expansion from F&B and convenience store operators. Transactional evidence from brokerage reports and listing platforms such as Batdongsan indicates widening rent dispersion across districts, with premium CBD properties exceeding 150USD/sqm/month, while other areas remain lower. These differences show that by 2025, Hanoi’s retail leasing market will be defined by multiple pricing tiers shaped by criteria like infrastructure development, demographic clustering, and shifting consumer patterns [2].

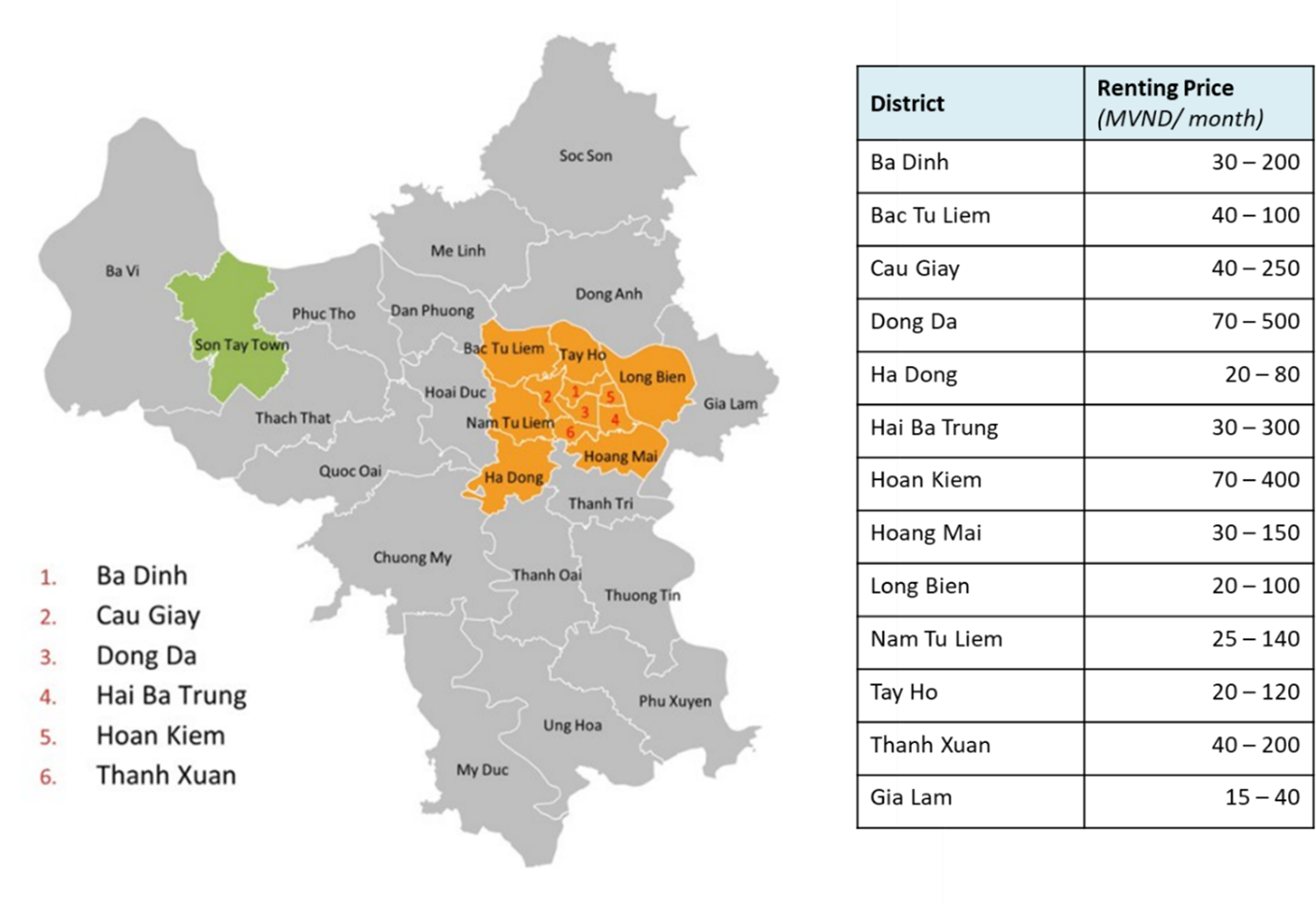

Estimated Retail Leasing Price Ranges in Hanoi

Unit: USD/sqm/month

Rental Price Map for District in Hanoi, 2025

(old districts before the merger)

Source: hanoidep.vn/

Hoan Kiem continues to record the highest retail leasing levels in Hanoi due to its concentration of tourism, historic commercial streets, and limited supply of high-street frontage. According to CBRE’s 2024 market figures, average CBD retail rents in Hanoi reached approximately USD 170 per sqm/month, reflecting strong year-on-year growth and sustained premium positioning. Street-level listings for F&B premises in Hoan Kiem further indicate that prime ground-floor units commonly range between USD 120–180 per sqm/month, particularly along Old Quarter corridors and Hoan Kiem Lake frontage [3].

Ba Dinh, located adjacent to Hoan Kiem, forms part of the extended CBD and remains one of the city’s highest-priced submarkets. Based on market listings and brokerage commentary, F&B-suitable properties in Ba Dinh generally range between USD 90–140 per sqm/month, supported by embassy clusters, government offices, and affluent residential communities that sustain stable consumption demand. Although slightly below Hoan Kiem’s peak levels, Ba Dinh consistently ranks among Hanoi’s premium leasing districts.

In contrast, Hai Ba Trung and Dong Da—historically strong commercial districts with dense populations and university clusters—demonstrate comparatively moderate rental levels in 2025. Retail listings show typical ground-floor F&B rents in these districts ranging from USD 55–90 per sqm/month, depending on frontage quality and street hierarchy. While these areas continue to benefit from high pedestrian volumes, rent growth has been more restrained relative to emerging lifestyle districts.

Tay Ho has experienced one of the most notable upward adjustments over the past decade. Originally priced below traditional inner districts in the early 2010s, Tay Ho now records F&B rental levels between USD 70–120 per sqm/month, particularly in areas with strong expatriate concentration and boutique commercial streets. This upward shift reflects demographic changes, higher disposable income among foreign residents, and increased competition for lifestyle-oriented retail assets. Savills’ commentary on rising consumer confidence and expanding retail formats in Hanoi supports the broader trend of pricing escalation in such lifestyle-driven submarkets.

Meanwhile, districts located further from the historic core—such as Cau Giay, Nam Tu Liem, and Long Bien—exhibit lower rental ranges but show measurable growth potential. Market listings indicate typical F&B rental levels of approximately USD 40–75 per sqm/month in Cau Giay and Nam Tu Liem, and USD 30–55 per sqm/month in Long Bien, depending on accessibility and mixed-use development proximity. These districts benefit from urban expansion, improved transport connectivity, and new residential-commercial complexes. Such patterns are consistent with CBRE’s national retail outlook, which projects continued rent escalation in secondary submarkets alongside sustained premiums in prime high-street locations [4]

How District-Level Leasing Differences Create Opportunities for F&B Business

The widening rental dispersion across Hanoi’s districts has created a clearer segmentation of F&B market entry strategies. As prime CBD rents reached approximately USD 170 per sqm/month in 2024, while citywide ground-floor averages remained around USD 50 per sqm/month in H1/2025, operators are increasingly forced to match format and capital intensity with district-level economics. Importantly, despite upward rent adjustments, the overall market remains resilient. In H1/2025, Hanoi’s retail occupancy rate stood at approximately 86%, supported primarily by F&B and convenience store expansion [6]. This indicates that tenant demand has remained stable even as rental levels increased. At the national level, Vietnam’s retail sales growth and continued household consumption expansion in 2024–2025 further reinforce leasing activity across both prime and secondary submarkets [7]

Premium and experiential F&B concepts that rely on brand visibility and tourist attraction can justify higher occupancy costs in Hoan Kiem and Ba Dinh. In contrast, mid-tier chains and scalable café formats benefit from the relative affordability of districts such as Cau Giay and Nam Tu Liem, where rents typically range between USD 40–75 per sqm/month, but residential and office density continues to expand. Tay Ho represents an intermediate opportunity: rising rental levels reflect stronger lifestyle demand, yet remain below the absolute peak of the historic CBD, allowing boutique and niche concepts to capture higher-income consumer segments at more manageable cost structures.

For foreign investors, this district-level differentiation implies that location strategy should be structured around format and context suitability rather than credibility alone. High-CAPEX flagship stores are best positioned in premium districts with demonstrated pricing power, while network expansion and multi-location rollouts are more economically sustainable in transitional western districts or emerging residential-commercial clusters. Surrounding districts, such as Long Bien, offer lower entry costs and neighborhood-focused potential, suitable for cost-efficient, catchment-based formats.

Given that retail rents continue to trend upward in prime areas while remaining competitive in secondary districts, F&B operators—especially foreign entrants—should prioritize effective rent analysis, incorporating projected revenue per sqm, lease terms, and district-level demand dynamics. In a structurally differentiated market like Hanoi in 2025, profitability depends less on centrality and more on the strategic alignment between brand positioning and district economics.

Read More

Optimal Location selection strategy for F&B businesses in HCMC in the new market context

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 900,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 28 3910 3913 |

References

- https://en.vietnamplus.vn/hanoi-retail-space-for-lease-records-best-results-in-five-years-post119353.vnp

- https://hanoitimes.vn/hanoi-retail-market-poised-for-continued-growth.780810.html

- https://mktgdocs.cbre.com/2299/2dc534ce-3500-49c8-aaa6-fef123aaa9e1-223401980/250109_CBRE_Vietnam_Market_Out.pdf

- https://batdongsan.com.vn/

- https://www.cbrevietnam.com/insights/books/nl-real-estate-market-outlook-2025/retail

- https://www.savills.com/research_articles/255800/223546-1

- https://www.savills.com.vn/insight-and-opinion/savills-news/220450/savills-host–viet-nam-retail-2025–opportunities-in-real-estate–event–exploring-market-potential-and-future-outlook

- https://hanoidep.vn/thue-mat-bang-kinh-doanh-an-uong-ha-noi/

- https://vn.savills.com.vn/blog/article/215146/vietnam-viet/tieu-chi-lua-chon-mat-bang-ban-le-cho-thuong-hieu-fb.aspx

Related article

Sidebar:

SUBSCRIBE NEWSLETTER