Japanese food producers have expanded production capacity, increasingly positioning Vietnam as a strategic food manufacturing and export base

13Jul2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

Abstract

This report analyzes the current state of Vietnam’s food processing industry, covering its market growth, structural challenges, and the investment drivers pulling Japanese manufacturers into the market. It also profiles Japanese companies already operating across the industry’s key growth segments such as fruit & vegetable, seafood, and milling & flour production, and closes with the opportunities and challenges new entrants should weigh. The report is intended for Japanese food companies and investors evaluating Vietnam as a production base for the Asian market.

Market overview

Japanese food manufacturers first entered Vietnam in the early 1990s to serve the growing domestic market. However, investment accelerated significantly from the late 2010s, driven by supply chain diversification, the China+1 strategy, and Vietnam’s expanding role as a regional manufacturing hub. Since then, many Japanese food producers have continued expanding production capacity, increasingly positioning Vietnam as a strategic food manufacturing and export base for both the domestic market and the broader ASEAN region.

Source: NSO

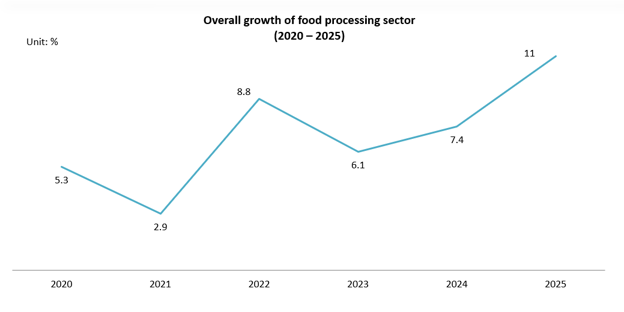

In recent years, Vietnam’s food processing industry has recorded solid results. After the disruption caused by Covid 19, industrial production recovered rapidly with growth accelerating from 2.9% in 2021 to 8.8% in 2022—an increase of nearly six percentage points. The industry then maintained a stable growth trajectory before regaining double-digit growth of 11% in 2025, which was backed by a domestic market of more than 100 million consumers, food and foodstuff retail sales of approximately VND 1,878 trillion, and an accommodation and food service sector valued at around VND 858 trillion[1]. Together, these factors highlight Vietnam’s growing potential as a regional food production hub and an increasingly attractive destination for long-term investment.

Source: NSO

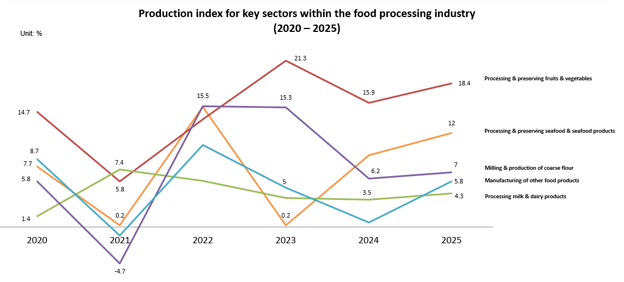

The market grows steadily with concentration in some high-potential segments. Among them, fruit and vegetable processing recorded the strongest performance. Due to the pandemic, it fell to 7.4% in 2021, then surged to 13.8% in 2022 and has stayed in double digits since, reaching 18.4% in 2025. This performance has been supported by abundant raw materials supply, rising agricultural exports, increasing investment in value-added processing, and improvements in food safety, traceability and cold-chain infrastructure, which have strengthened Vietnam’s capability to produce higher-value processed food for export markets[2].

Seafood processing shows the second strongest increasing trend; however, it fluctuated from 2020 to 2023 before it climbed sharply to 9.2% in 2024 and 12% in 2025, also entering double digits. The sector has benefited by improving export demand, a stable domestic seafood supply, and increasing investment in value-added processing to meet international market requirements[3]. Milling and coarse flour production rebounded strongly after the pandemic before returning to a more moderate growth path and reaching 7% (2025), supported by continued demand from downstream food manufacturing and domestic consumption.

However, Vietnam’s food processing industry still faces several structural challenges. In both fruit and vegetable processing and seafood processing, value-added products account for a relatively limited share of total output, while many enterprises continue to rely on primary processing and exports of raw or semi-processed products. In addition, differences in raw material quality, cold-chain infrastructure, and processing technology continue to affect product consistency and competitiveness in international markets. These gaps highlight the need for further investment in advanced processing technologies, quality management, and an integrated supply chain

Japanese investments’ drivers

Vietnam’s appeal to Japanese food manufacturers rests on three main pillars: a strategic shift in regional supply chains, the country’s own agricultural and processing strengths, and a supportive trade and policy environment.

The “China+1” supply chain shift

Since the COVID-19 pandemic and rising geopolitical uncertainties, many Japanese manufacturers have diversified production across Asia to reduce reliance on a single country. Vietnam has become one of the key beneficiaries of this shift due to its proximity to China, well-established manufacturing ecosystem, competitive operating costs, and political stability. Especially in the manufacturing sector, JETRO has highlighted the food and beverage sector as one of the most prominent manufacturing sectors attracting Japanese investment in Vietnam[5]. This reflects growing confidence in Vietnam not only as a cost-competitive production location but also as a long-term manufacturing base capable of serving both domestic and regional markets.

Strong agricultural resources and an expanding food processing industry

As one of the world’s leading producers and exporters of seafood, rice, tropical fruits, coffee, and cashew nuts, the country offers manufacturers reliable access to diverse raw materials. This enables food processors to locate production close to raw material sources, improving supply stability and reducing procurement and logistics costs.

At the same time, Vietnam’s food processing industry has continued to strengthen its production capabilities. As discussed, high-growth subsectors such as fruit and vegetable processing, seafood processing, and milling have expanded steadily, reflecting the country’s increasing capacity for food manufacturing. However, value-added processing remains underdeveloped in many segments; therefore, it creates a strong opportunity for Japanese companies to develop value-added processed foods, particularly in agricultural and aquatic products. Also, Japanese companies can leverage their strengths in advanced processing technologies, quality management, food safety, and product development to enhance productivity, improve product quality, and support Vietnam’s transition toward higher-value food manufacturing[6].

Trade agreements and supportive government policies

Vietnam’s extensive network of free trade agreements (FTAs) has strengthened its position as an export-oriented manufacturing hub. Long-standing agreements such as the Vietnam–Japan Economic Partnership Agreement (VJEPA), CPTPP, EVFTA, and RCEP provide preferential market access to major economies across Asia-Pacific and Europe. For food manufacturers, these agreements reduce tariff barriers and facilitate exports of processed food products, improving the competitiveness of products manufactured in Vietnam.

At the domestic level, Vietnam has also introduced policies to promote higher-value food processing. Directive No. 25/CT-TTg (2020)[7] encourages the development of agricultural, forestry, and fisheries processing industries by promoting deep processing, modern processing technologies, and stronger linkages between processing facilities and raw material areas. In parallel, Decree No. 57/2018/NĐ-CP[8] provides incentives for enterprises investing in agriculture and rural areas, including support for agricultural processing facilities, post-harvest infrastructure, cold storage, and production equipment. In addition, under the Law on Investment 2020[9], the cultivation and processing of agricultural, forestry, and aquaculture products are designated as sectors eligible for investment incentives. Depending on the project, investors may benefit from preferential corporate income tax rates, tax exemptions and reductions, import duty exemptions for machinery and equipment, as well as land-related incentives, particularly in industrial parks and economic zones. Together, these international agreements and domestic policies create a favorable environment for Japanese companies to establish or expand food manufacturing operations in Vietnam while supporting the country’s transition toward higher-value food production.

Competitive landscape

The table below profiles some key players who are already operating across Vietnam’s three fastest-growing food processing segments, showing how deep their presence runs and what each is producing.

| Growth segment | Name | Nationality/Year | Main products | Profile / Achievements |

| Fruit & vegetable processing

(VSIC code: 1030) |

Nafoods Group | Vietnam (1995) | Fruit juice concentrates, NFC juice, IQF fruits & vegetables, dried fruits | One of Vietnam’s leading fruit processors with exports to over 70 countries. Operates modern processing plants and focuses on value-added fruit products[10]. |

| Yasaka Fruit Processing Vietnam | Japan (2008) | Processed fresh tropical fruits | Japanese-invested company specializing in post-harvest treatment and preservation of tropical fruits using Hot Vapor Heat Treatment (VHT). The company helps Vietnamese fruits meet phytosanitary requirements for export to high-standard markets such as Japan, Australia and New Zealand, strengthening the fruit value chain and export capability[11]. | |

| Kagome Vietnam | Japan (2016) | Tomato puree, tomato juice, ketchup, processed tomato products, processed vegetable products | Subsidiary of Kagome Co., Ltd., one of Japan’s leading vegetable food companies. Kagome Vietnam develops a sustainable vegetable value chain through contract farming with local growers and applies Japanese cultivation techniques, quality management, and food processing technologies to manufacture high-quality tomato and vegetable products for the Vietnamese market and regional expansion[12]. | |

| Seafood processing

(VSIC code: 1020) |

Umios Vietnam (previously Maruha Nichiro Vietnam) | Japan (2004) | Frozen seafood, processed seafood | Subsidiary of Umios Co., Ltd, one of the world’s largest seafood companies, sourcing and expanding seafood processing partnerships in Vietnam to strengthen its global supply chain[13]. |

| Kyokuyo Vina Foods | Japan (2025) | Frozen shrimp, value-added seafood products | Subsidiary of Kyokuyo Co., Ltd., one of Japan’s leading seafood companies. The facility produces value-added seafood products for export, primarily to Japan, supporting Kyokuyo’s global seafood supply chain and reinforcing Vietnam’s role as a regional seafood processing base[14]. | |

| NIGICO | Japan (2000) | Frozen shrimp, breaded shrimp, sushi shrimp (Nobashi Ebi), tempura shrimp, value-added seafood | Wholly owned by Nissui Corporation, one of Japan’s largest seafood companies. Located in Ca Mau, NIGICO operates an integrated seafood processing plant with internationally recognized certifications including BRCGS, ASC CoC, MSC CoC, HALAL, BAP, and SEDEX, supplying high-value seafood products mainly to Japan, North America and Europe[15]. | |

| Milling & coarse flour production

(VSIC code: 1610) |

CJ-SC Global Milling | South Korea × Japan (2013) | Wheat flour, premixes | Joint venture between CJ CheilJedang Corporation, Sumitomo Corporation and Chiba Flour Milling Ltd. One of Vietnam’s largest modern flour mills serving industrial food manufacturers[16]. |

| Showa Sangyo International Vietnam | Japan (2025) | Premixed flour, tempura batter mix, karaage mix | A subsidiary of Showa Sangyo Co., Ltd. Invested US$21 million in its first Vietnam manufacturing plant. The factory began operation in 2026 and is positioned as Showa Sangyo’s key premixed flour production hub for ASEAN, supplying both Vietnam and regional export markets[17]. | |

| Vietnam Nisshin Technomic | Japan (2018) | Premixes, breader, batter mix, bakery mix | Manufacturing subsidiary of Nisshin Seifun Group producing value-added flour products. Certified FSSC 22000 and HALAL, supporting food manufacturers in Vietnam and regional markets[18]. |

B&Company’s synthesis

Japanese companies are present in all three growth segments, including fruit and vegetable processing, seafood processing, and milling & flour production. Their presence ranges from long-established manufacturers such as Umios and NIGICO to recent investments like Showa Sangyo, indicating sustained confidence in Vietnam as a manufacturing location. However, the investment is unevenly distributed across the Vietnamese market as seafood processing has attracted the strongest presence of Japanese manufacturers, while only a limited number of Japanese companies are active in fruit and vegetable processing

In addition, these companies mainly use Vietnam as a production base for export markets rather than serving only domestic demand. Yasaka processes tropical fruits for international markets, Kyokuyo supplies seafood primarily to Japan, NIGICO exports to Japan, North America and Europe, while Showa Sangyo positions its Vietnam factory as an ASEAN production hub. Therefore, highlighting Vietnam’s growing role in regional and global food supply chains.

Implications for investors

Opportunities

The clearest opportunity lies in the gap between fast subsector growth and limited value-added capacity. Fruit and vegetable processing is the fastest-growing segment of the industry, yet Japanese presence there remains limited to just two companies (Yasaka, Kagome) against a market still dominated by domestic players such as Nafoods — this is the segment with promising room for new Japanese entrants. Seafood processing, by contrast, already has a strong Japanese presence (Umios, Kyokuyo, NIGICO) and shows how quickly a value-added ecosystem can be built when technology and quality management are brought in, offering a model that could be replicated in fruit & vegetable processing. The milling and coarse flour segment shows a similar opening with many Japanese and Japanese-linked companies, such as recent entrants like Showa Sangyo, positioning Vietnam not just as a domestic supplier but as a production hub for the wider ASEAN market — a model other Japanese processors could follow. Underpinning all three segments is Vietnam’s FTA network (VJEPA, CPTPP, EVFTA, RCEP) and domestic incentive framework (Directive 25/CT-TTg, Decree 57/2018/NĐ-CP, Law on Investment 2020), which together lower the cost of exporting processed food from Vietnam and support investment specifically in processing facilities, cold storage, and production equipment.

Challenges

The same structural gap that creates opportunity also represents a real barrier to entry. Across fruit & vegetable and seafood processing, value-added products still account for a relatively limited share of total output, with many enterprises still exporting raw or semi-processed goods — meaning new entrants face an industry-wide shortfall in processing sophistication, not just a company-specific one. Differences in raw material quality, cold-chain infrastructure, and processing technology continue to affect product consistency, which directly limits competitiveness in the demanding international markets that most Japanese-invested companies (Kyokuyo, NIGICO, Yasaka, Showa Sangyo) are targeting. In fruit and vegetable processing specifically, the challenge is competitive rather than purely technical: domestic firms such as Nafoods already have an established position, meaning a new Japanese entrant would compete against experienced local players rather than enter an empty field.

Actionable implications

First, any new investment should be structured to capture Vietnam’s existing incentive framework — the preferential corporate income tax rates, import duty exemptions on machinery, and land incentives available under the Law on Investment 2020 for agricultural, forestry, and aquaculture processing.

Second, new entrants can consider following the export-hub model already proven by Kyokuyo, NIGICO, and Showa Sangyo — building Vietnam-based capacity aimed at Japan, ASEAN, and global markets rather than the domestic market alone, in order to make full use of Vietnam’s FTA network.

Finally, companies should direct investment specifically toward the value-added and infrastructure gaps the industry itself has identified — cold-chain capacity, processing technology, and quality management systems — since these are the same capabilities Japanese firms are already recognized for bringing into the market.

Read more

Fresh meat in Vietnam: Market characteristics and consumer trend

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 1,000,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 24 3978 5165 |

[1] https://dms.gov.vn/documents/d/guest/bc-ttnd-2025-tieng-viet-pdf

[2] https://tapchikinhtetaichinh.vn/cong-nghiep-che-bien-nong-san-but-pha-tao-nen-tang-cho-nong-nghiep-viet-nam-hien-dai-va-ben-vung-102932.html

[3] https://b-company.jp/vi/vietnams-seafood-processing-market-and-opportunities-for-foreign-investors/

[4] https://kinhte.congthuong.vn/thao-go-diem-nghen-dua-cong-nghe-thuc-pham-ra-thi-truong-hieu-qua-450776.html ; https://nghiencuu.tapchikinhtetaichinh.vn/phat-trien-chuoi-cung-ung-lanh-de-nang-cao-gia-tri-thuy-san-tai-dong-bang-song-cuu-long-149413.html

[5] https://vir.com.vn/japanese-players-take-domestic-demand-into-account-114160.html

[6] https://vasep.com.vn/san-pham-xuat-khau/tin-tong-hop/chinh-sach/nganh-thuy-san-viet-nam-truoc-thach-thuc-cua-mo-hinh-kinh-te-moi-bai-toan-gia-tri-gia-tang-va-con-duong-but-pha-34889.html

[7] https://chinhphu.vn/default.aspx?docid=200164&pageid=27160

[8] https://chinhphu.vn/default.aspx?docid=193514&pageid=27160

[9] https://vanban.chinhphu.vn/?pageid=27160&docid=200449&classid=1&typegroupid=3

[10] https://www.nafoods.com/introduction

[11] https://yasaka.vn/gioi-thieu.html

[12] https://sulforaphane.com.vn/pages/ve-kagome

[13] https://www.umios.com/en/

[14] https://vasep.com.vn/san-pham-xuat-khau/tin-tong-hop/san-xuat/cong-ty-che-bien-thuy-san-thuoc-top-3-nhat-ban-mo-nha-may-tai-viet-nam-32220.html

[15] https://www.nigico.vn/?_fsi=8xqS6NCh

[16] https://botmicjsc.wordpress.com/gioi-thieu-cj-sc/

[17] https://vir.com.vn/japanese-food-giant-chooses-vietnam-for-ready-mix-flour-production-151397.html

Related article

SUBSCRIBE NEWSLETTER