This article analyzes the import and sales of Japanese processed and packaged food in Vietnam, based on trade data and market observations.

01Apr2026

Highlight content / Industry Reviews / Latest News & Report

Comments: No Comments.

This report analyzes the import and sale of Japanese processed and packaged food in Vietnam, based on HS Code classifications, trade data, and market observations. Japanese food imports have grown strongly over the past decade, driven by rising urbanization, premiumization, and demand for convenience and health-oriented products. Import sales are concentrated in categories such as convenience foods, seasonings, and beverages. Japanese processed food has high potential to continue growing in Vietnam, yet market expansion can be challenged with price sensitivity, limited brand awareness, and logistical burdens.

Overview of the import situation of Japan’s processed and packaged food

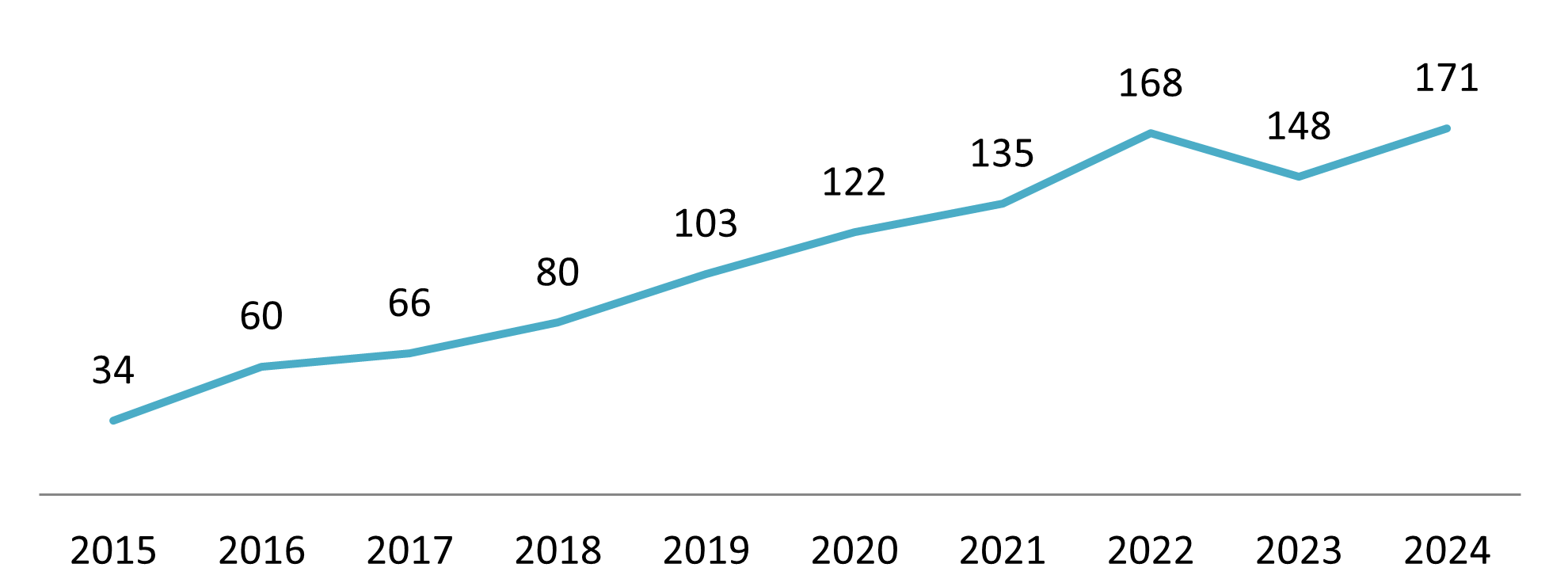

Imports of Japanese processed and packaged food into Vietnam have shown steady and long-term growth over the past decade, despite the drop in 2023, reflecting deepening bilateral trade relations and changing Vietnamese consumption patterns. Total import value increased from USD 34 million in 2015 to USD 171 million in 2024 (CAGR of 19.4%)[1]. This upward trend shows growing acceptance of Japanese food products in Vietnam, particularly among urban and middle-income consumers[2]. The growth trajectory also aligns with broader Vietnam–Japan trade expansion, as Japan remains one of Vietnam’s key economic partners in Asia.

Import value of processed and packaged food from Japan to Vietnam

Unit: USD Million

Source: ITC Trade Map

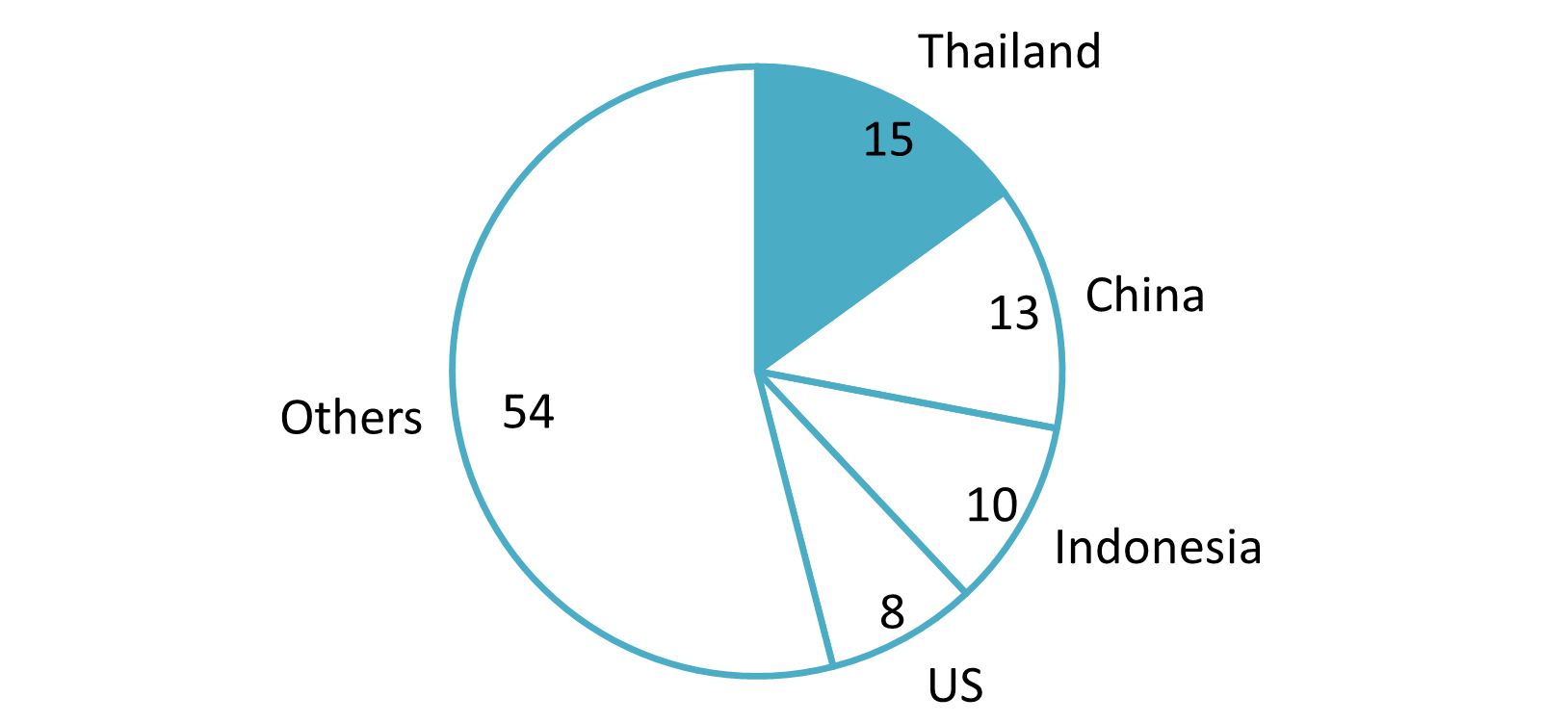

Despite this growth, Japanese processed food imports still account for a relatively small share of Vietnam’s overall imports (USD 6 billion in 2024). Japanese products represent around 3% of total imports, far behind major suppliers such as Thailand, China, Indonesia, and the United States. These countries benefit from geographical proximity, lower production costs, and a strong presence in mass-market food categories. In contrast, Japanese exports to Vietnam tend to concentrate on higher-value, premium, and specialized food segments[3].

Import value of processed and packaged food to Vietnam by countries in 2024

100% = USD 6.0 billion

Source: ITC Trade Map

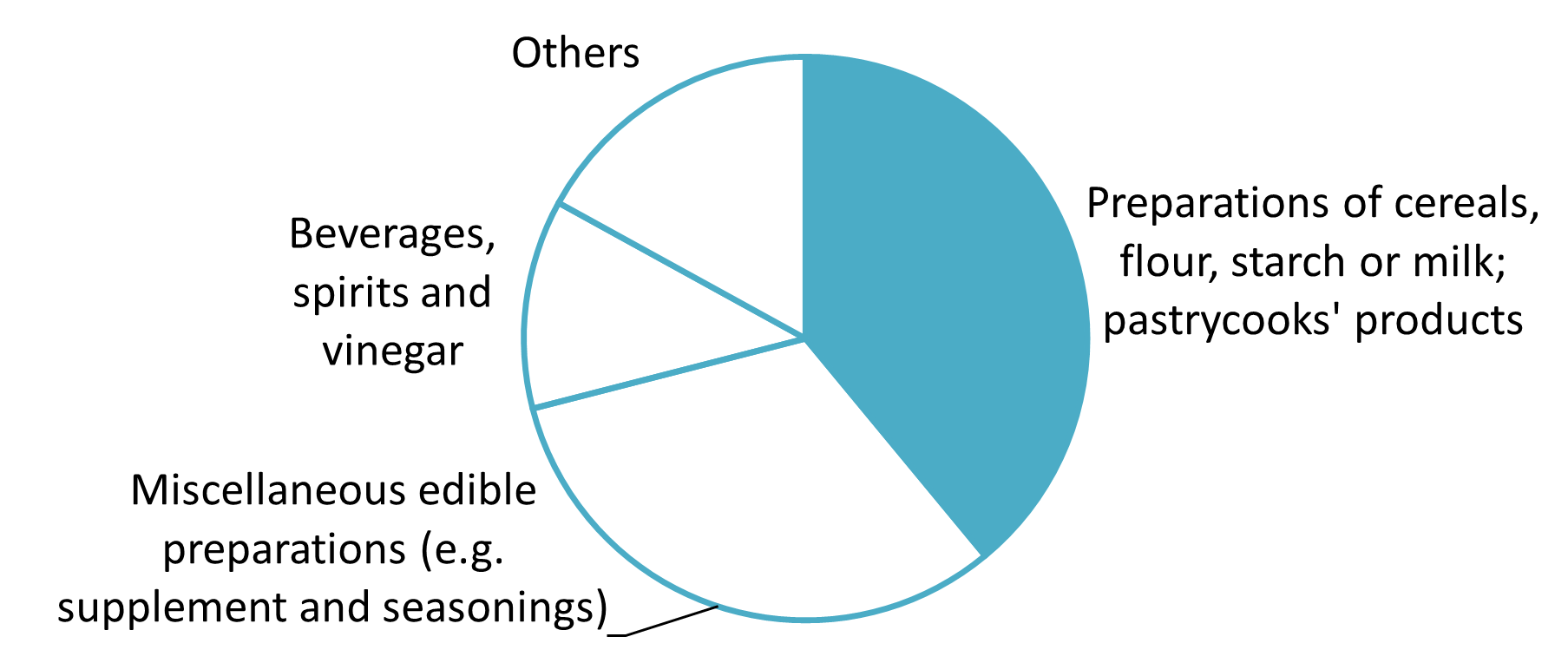

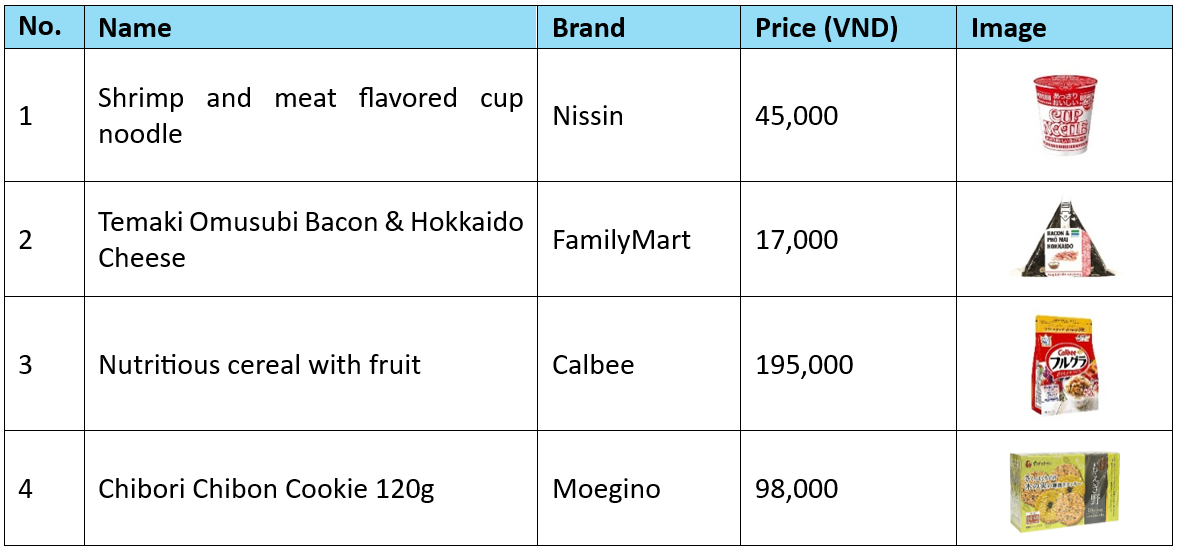

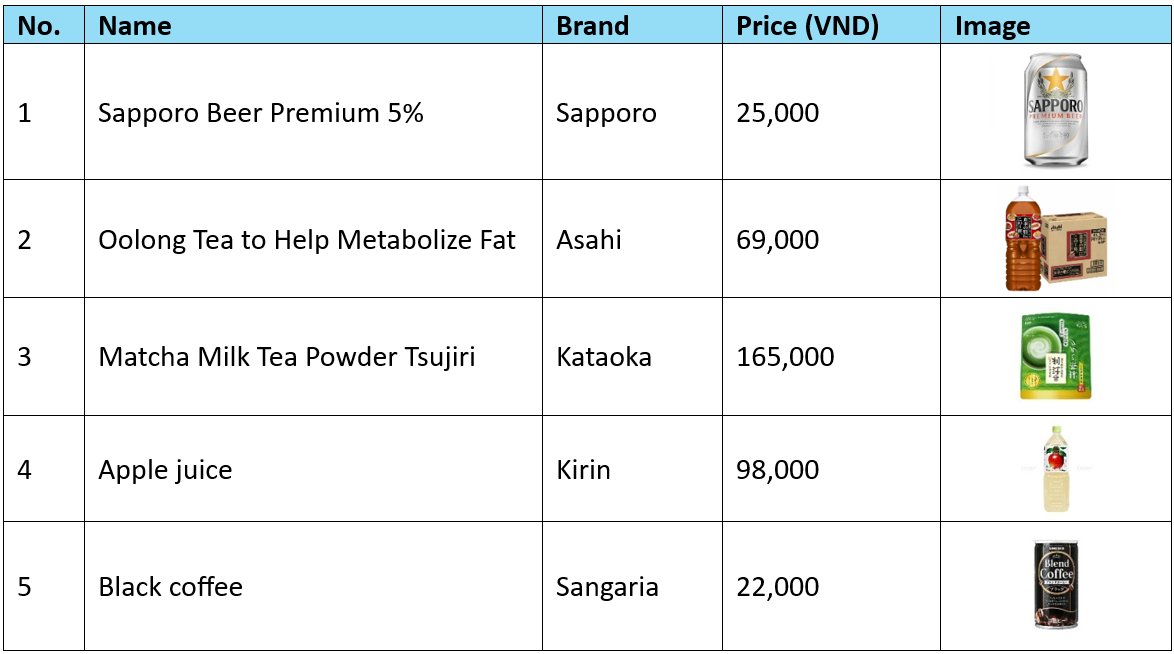

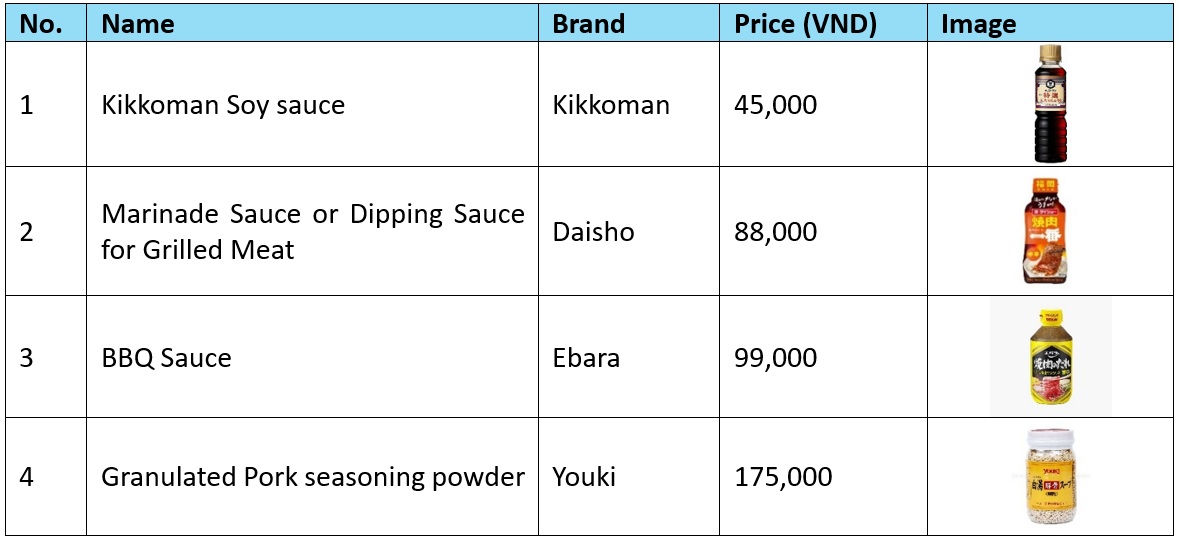

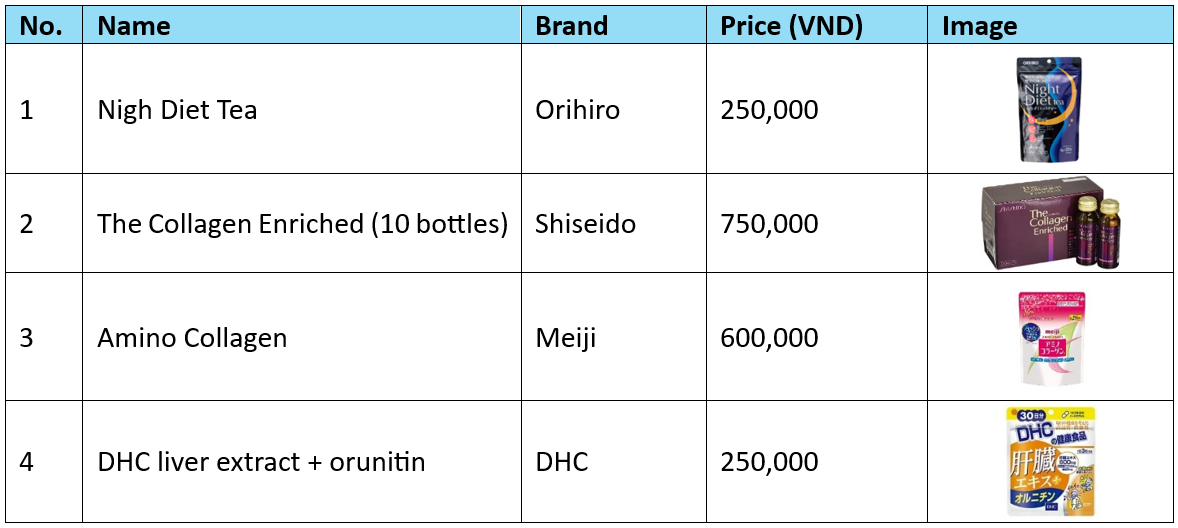

Popular product lines

Related article

Log in / Register

Continue without an account

Log in / Register

SUBSCRIBE NEWSLETTER