ベトナムの再生可能エネルギー市場は、急速な経済成長と政府の強力なコミットメントに牽引され、東南アジアで最も活力のある市場の一つです。再生可能エネルギーは既にベトナムの設置電力容量の約271億トン(TP3T)を占めています。

2025年10月13日

最新ニュースとレポート / ベトナムブリーフィング

コメント: コメントはまだありません.

ベトナムの再生可能エネルギー市場は、急速な経済成長と政府の強力なコミットメントに牽引され、東南アジアで最も活力のある市場の一つとなっています。再生可能エネルギーは既にベトナムの設備発電容量の約27%を占めています。第8次電力開発計画(PDP8)に基づく最近の政策は、この数値をさらに引き上げ、2030年までに再生可能エネルギーによる発電量を2800万~36%にすることを目標としています。これは、ベトナムの再生可能エネルギー市場への参入を目指す外国投資家にとって、大きなチャンスがあることを示唆しています。

ベトナムの再生可能エネルギー市場の概況

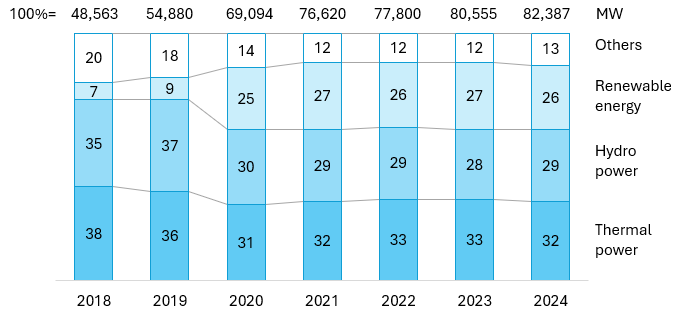

ベトナムは過去10年間で再生可能エネルギーのブームを経験し、小規模なプレイヤーから地域のリーダーへと変貌を遂げました。2023年末までに、ベトナムの太陽光発電容量は東南アジア最大(18.6GW)となりました。[1]再生可能エネルギー(主に太陽光と風力)は現在、国の設備発電容量の約27%を占めています。[2]この目覚ましい増加は、支援政策とベトナムの有利な地理条件(豊富な太陽光と強風が吹く 3,000 km の海岸線)によって推進されています。

ベトナムの設置電力容量

出典: B&Company 編集

政府は、エネルギー安全保障と気候変動対策への取り組みを背景に、再生可能エネルギーを強く推進しています。新たに承認されたPDP8(2023年)では、ベトナムは2030年までに再生可能エネルギーによる電力供給量を28~36%、2050年までに74~75%に増加させることを目標としています。[3] これまでの石炭と水力発電への依存からの抜本的な転換です。ベトナムは、再生可能エネルギー、特に太陽光と風力による発電の最大化を目指しています。

2030年と2050年に向けたベトナムの電源構成

| 電源 | 2030年の電力容量 | 電力容量2050 | ||

| MW | % | MW | % | |

| 太陽 | 46,459~73,416 | 25-31 | 293,088 – 295,646 | 35-38 |

| 水力発電 | 33,294~34,667 | 15-18 | 40,624 | 5 |

| 陸上および沿岸風力 | 26,066~38,029 | 14-16 | 84,696~91,400 | 11 |

| 石炭火力発電 | 31,055 | 13-17 | 0 | 0 |

| 蓄電電源 | 10,000~16,300 | 5-7 | 95,983 – 96,120 | 11-12 |

| 洋上風力 | 6,000~17,032 | 3-7 | 113,503~139,097 | 15-17 |

| Nuclear power | 4,000~6,400 | 2-3 | 10,500~14,000 | 1-2 |

| バイオマス | 1,523~2,699 | 1 | 4,829 – 6,960 | 1 |

| 廃棄物発電 | 1,441 – 2,137 | 1 | 1,784 -2,137 | 0.2-0.3 |

| その他の電源 | 14,628-23,453 | 6-13 | 129,496-152,697 | 17-18 |

| 全体 | 183,291 – 236,363 | 100 | 774,503~838,681 | 100 |

出典:決定768/QĐ-TTg

ベトナムは当初、2019年から2021年にかけて、太陽光発電と風力発電の活性化を図るため、大幅な固定価格買い取り制度(FiT)を導入しました。風力発電容量は、2013年の53MWから2023年には約5,888MWに増加しました。その後、系統のボトルネックにより、2022年には太陽光発電が約13億kWh抑制されました。現在、政策は系統のアップグレード、2024年までの大口需要家向け直接電力購入契約(DPA)、蓄電池の推進、系統のデジタル化、屋上太陽光発電の促進を通じた持続可能な成長へと軸足を移しており、2030年までに建物の50%に屋上太陽光発電を普及させることを目標としています。制度は固定価格買い取り制度から競争入札へと移行しつつありますが、税制優遇措置や輸入関税の免除といった優遇措置は、外国資本や専門知識の誘致に引き続き活用されます。

ベトナムの再生可能エネルギー市場の主要プレーヤー

歴史的に、ベトナムの再生可能エネルギー導入は外国投資家が主導してきました。タイ、シンガポール、日本などの企業が資本と技術を持ち込み、初期の太陽光発電所や風力発電所を建設しました。しかし、同時に、大規模プロジェクトにおける国内企業の役割について疑問が生じました。現在、ベトナムの有力企業が台頭するにつれ、この傾向は変わりつつあります。複数の地元コングロマリット(Vingroup、Trungnam、TTC、BIMなど)がクリーンエネルギー分野で積極的に事業を拡大しています。

関連記事

ログイン / 新規登録

アカウントなしで続ける

ログイン / 新規登録

ニュースレターを購読する