This article analyzes the import and sales of Japanese processed and packaged food in Vietnam, based on trade data and market observations.

01Apr2026

Highlight content / Industry Reviews / Latest News & Report

Comments: No Comments.

This report analyzes the import and sale of Japanese processed and packaged food in Vietnam, based on HS Code classifications, trade data, and market observations. Japanese food imports have grown strongly over the past decade, driven by rising urbanization, premiumization, and demand for convenience and health-oriented products. Import sales are concentrated in categories such as convenience foods, seasonings, and beverages. Japanese processed food has high potential to continue growing in Vietnam, yet market expansion can be challenged with price sensitivity, limited brand awareness, and logistical burdens.

Overview of the import situation of Japan’s processed and packaged food

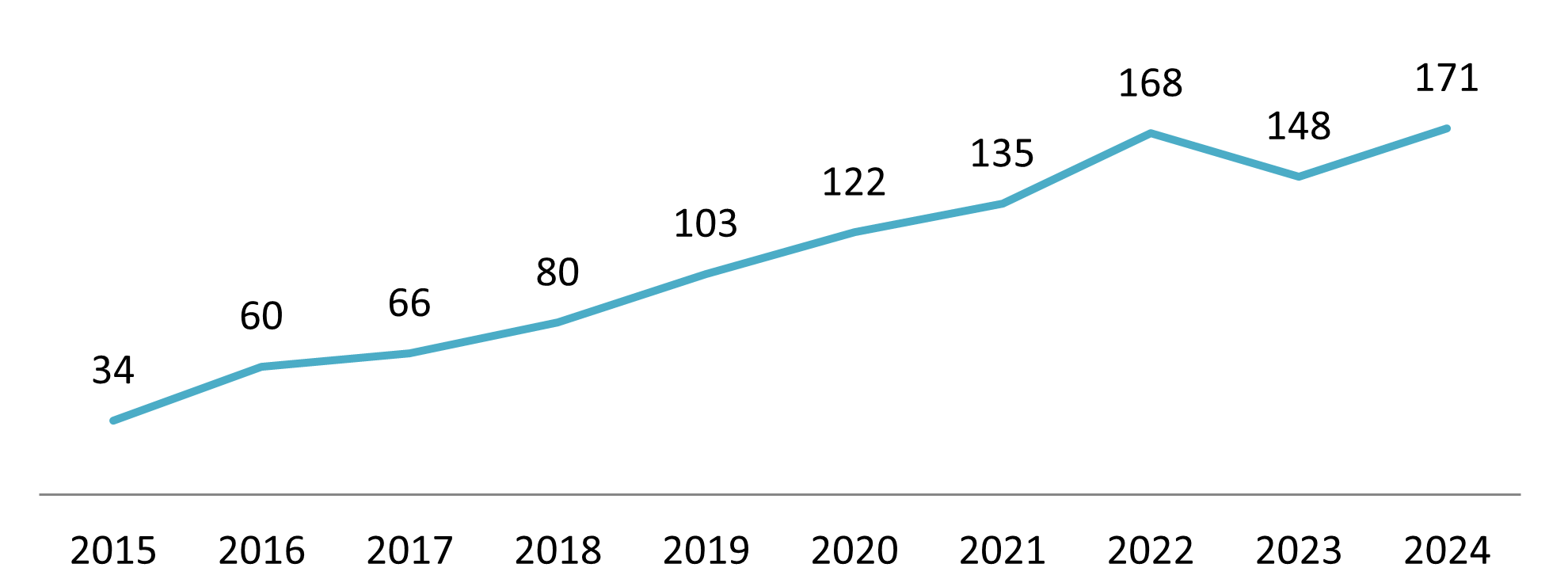

Imports of Japanese processed and packaged food into Vietnam have shown steady and long-term growth over the past decade, despite the drop in 2023, reflecting deepening bilateral trade relations and changing Vietnamese consumption patterns. Total import value increased from USD 34 million in 2015 to USD 171 million in 2024 (CAGR of 19.4%)[1]. This upward trend shows growing acceptance of Japanese food products in Vietnam, particularly among urban and middle-income consumers[2]. The growth trajectory also aligns with broader Vietnam–Japan trade expansion, as Japan remains one of Vietnam’s key economic partners in Asia.

Import value of processed and packaged food from Japan to Vietnam

Unit: USD Million

Source: ITC Trade Map

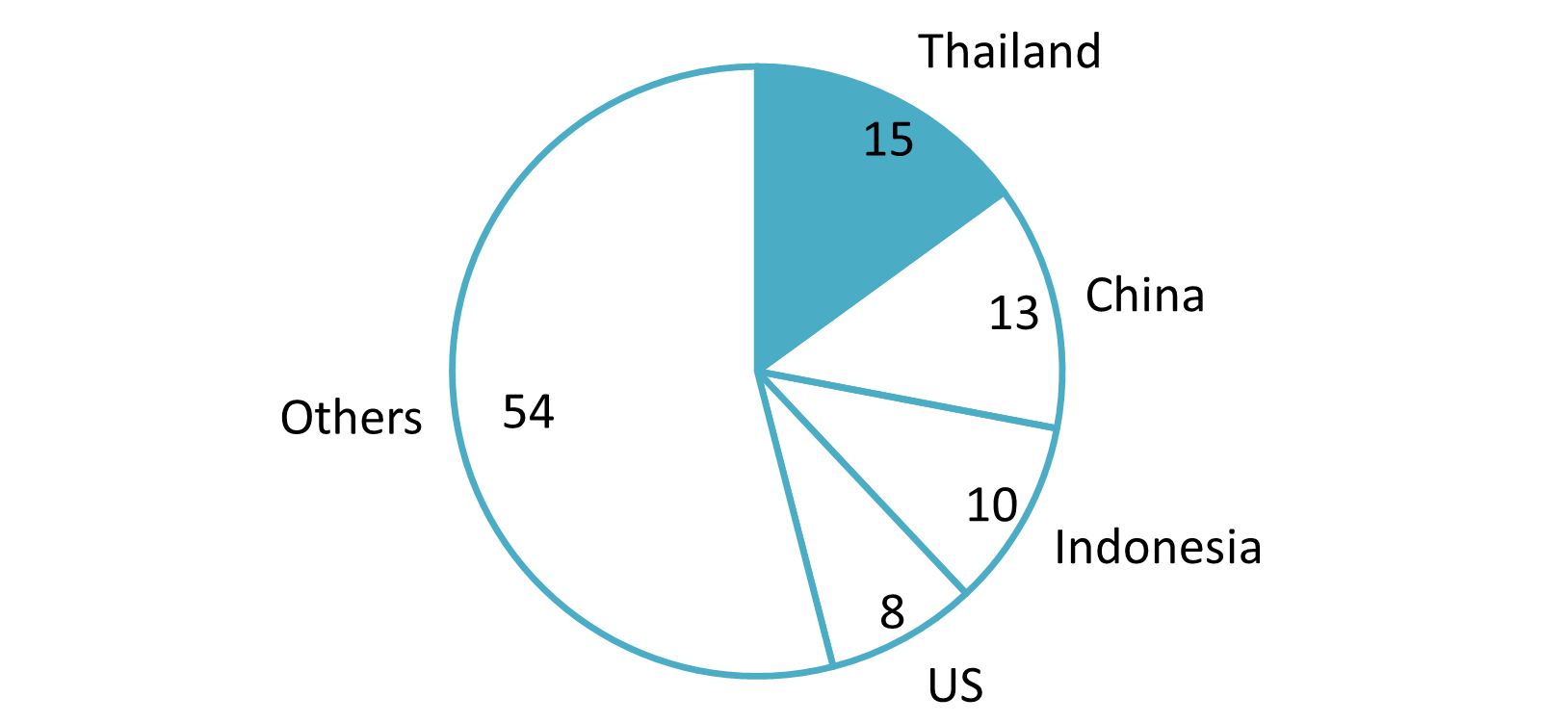

Despite this growth, Japanese processed food imports still account for a relatively small share of Vietnam’s overall imports (USD 6 billion in 2024). Japanese products represent around 3% of total imports, far behind major suppliers such as Thailand, China, Indonesia, and the United States. These countries benefit from geographical proximity, lower production costs, and a strong presence in mass-market food categories. In contrast, Japanese exports to Vietnam tend to concentrate on higher-value, premium, and specialized food segments[3].

Import value of processed and packaged food to Vietnam by countries in 2024

100% = USD 6.0 billion

Source: ITC Trade Map

Popular product lines

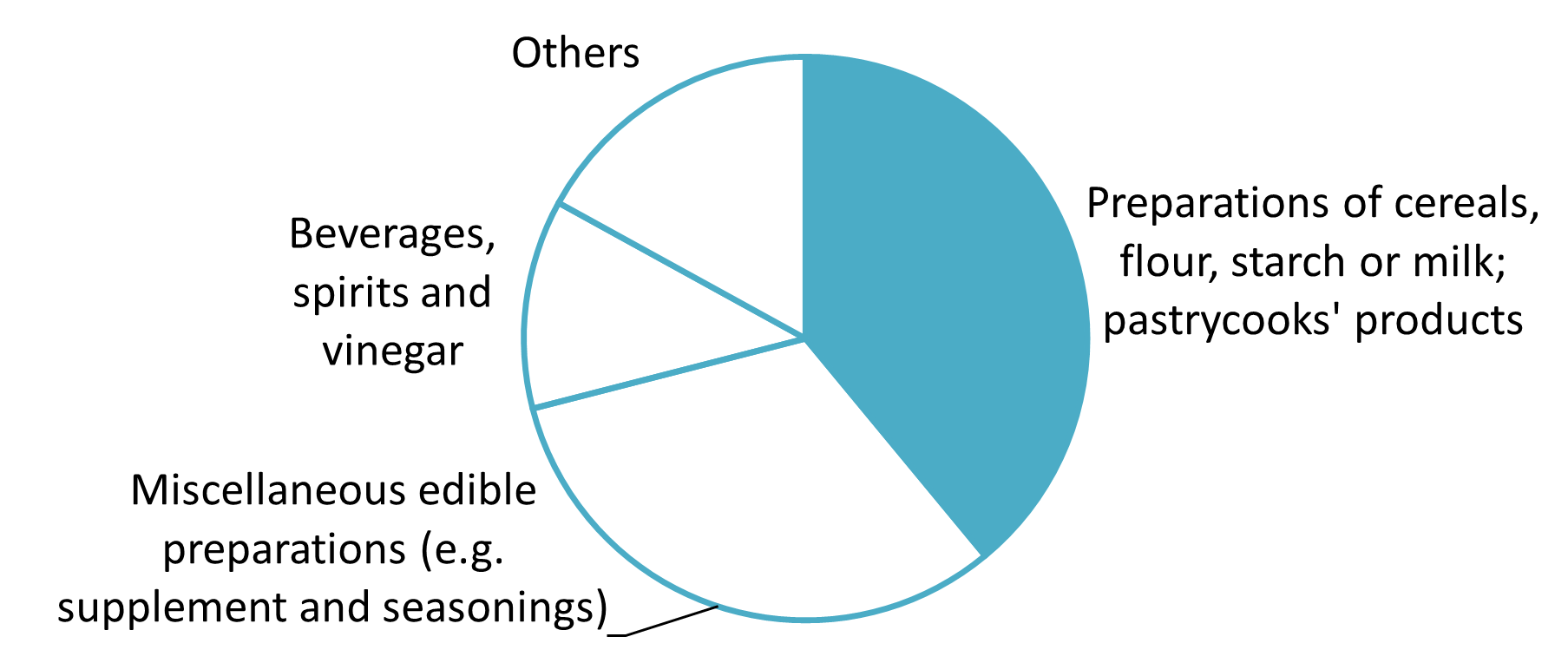

The import value of processed and packaged food from Japan to Vietnam in 2024 is contributed mostly by HS19 – starch, cereals, flour-based products, and HS21 (including food supplement, sauce, and seasoning). HS22 concerning beverages also takes up a large proportion.

Import value of processed and packaged food from Japan to Vietnam (2024)

100% = USD 171 million

Source: ITC Trade Map

Convenience & Bakery Foods

One of the most prominent product lines is convenience and bakery/prepared foods, including onigiri rice balls, sandwiches, cereals, sweet and savory snacks, and instant noodles. These products are widely distributed through supermarkets, specialty Japanese stores, and convenience chains (e.g., FamilyMart, Ministop). Vietnamese consumers, particularly urban millennials and Gen Z, are increasingly seeking easy, quick meal options that fit busy lifestyles.

Example products of Convenience & Bakery Foods

B&Company’s synthesis

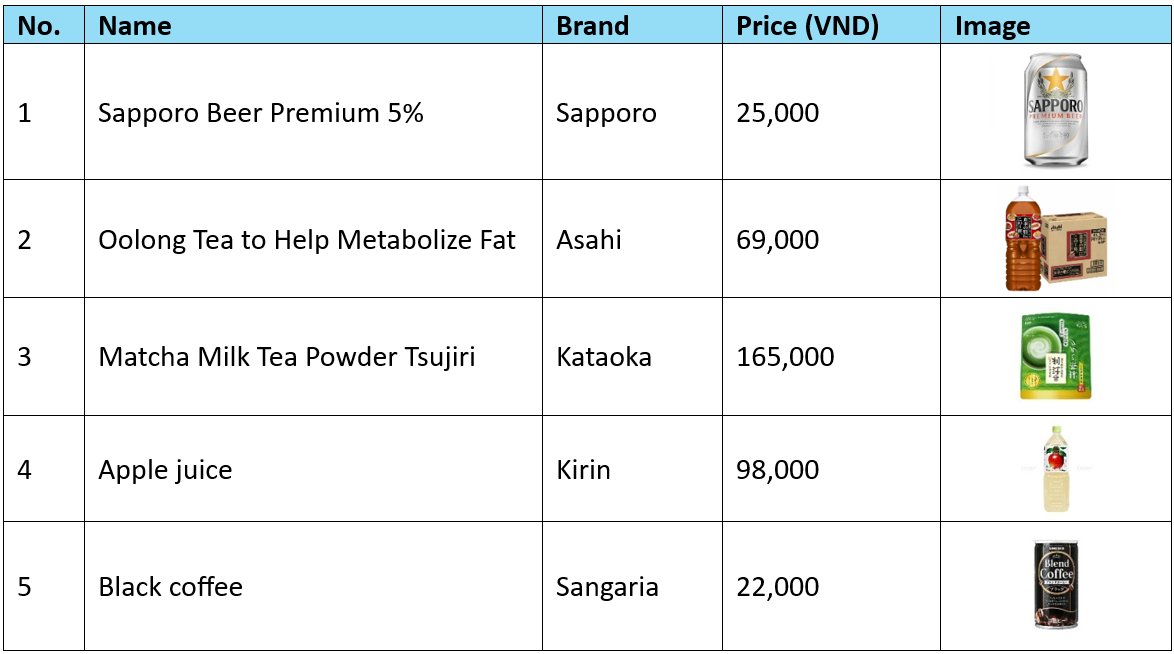

Beverages and Drinks

Imported beverages from Japan, such as ready-to-drink teas, craft juices, premium coffee beverages, and traditional drinks, represent another key line. These items are appealing to both younger consumers and health-oriented buyers looking for alternatives to local sodas and sugary drinks. The Vietnamese beverage market is expanding rapidly with diversification towards functional, imported, and premium products[4]. Retail formats such as supermarkets and convenience stores contribute to this trend by dedicating shelf space to imported beverages.

Example products of Beverages and Drinks

B&Company’s synthesis

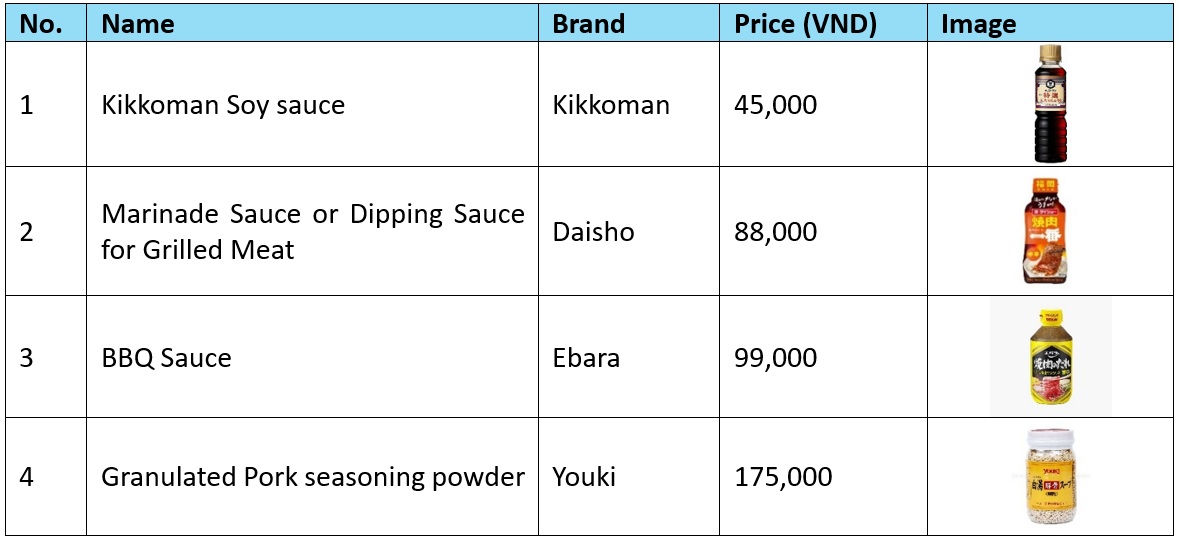

Seasonings and Sauces

Vietnamese cooking is inherently flavor-driven, and Japanese sauces, seasonings, condiments, miso pastes, dressings, and ready sauces have found appeal among urban home cooks and foodservice operators[5]. These products are often positioned as premium condiments that add unique umami or flavor profiles to dishes and are commonly used in modern fusion cuisines. Consumers increasingly experiment with global cooking styles, boosting demand for such products beyond traditional Vietnamese spices.

Example products of Seasonings and Sauces

B&Company’s synthesis

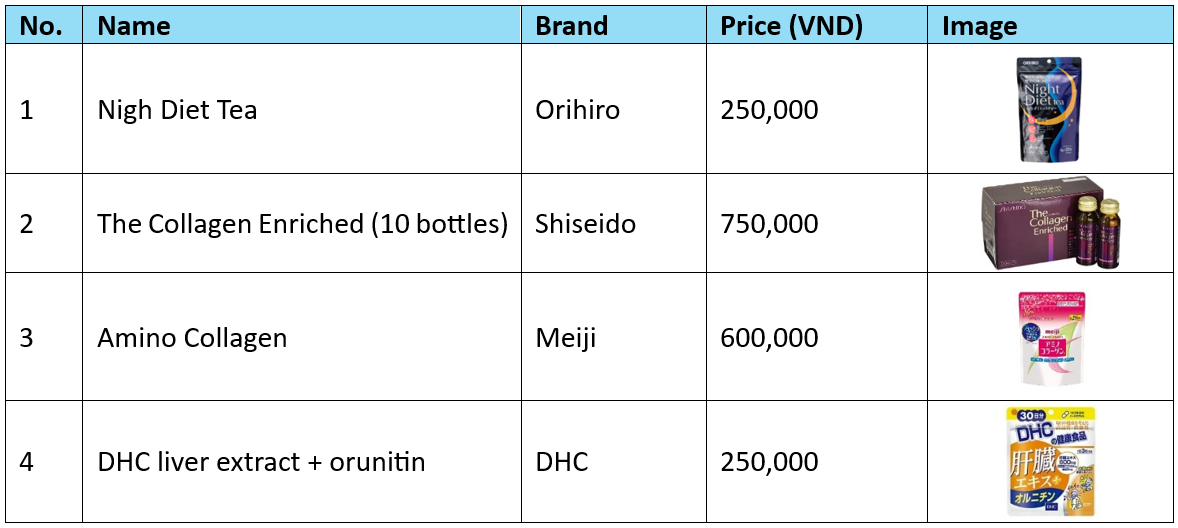

Health & Functional Foods

Vietnam’s rising health consciousness is reflected in the growing demand for functional foods and dietary supplements imported from Japan[6]. Japanese health food products such as collagen drinks, digestive health supplements, fortified teas, and nutraceutical snacks appeal to Vietnamese consumers focused on wellness and preventative health, particularly among middle-income consumers.

Example products of Health & Functional Foods

B&Company’s synthesis

Food consumption trend in Vietnam

– Convenience-driven food consumption: Vietnam’s rapid urbanization and evolving lifestyle behaviors are a major driver. As more consumers relocate to cities and adopt busier schedules, demand for ready-to-eat, ready-to-cook, and convenience foods has increased sharply[7]. This trend is further supported by the expansion of convenience retail chains and food delivery platforms across urban centers.

– Premiumization and rising demand for quality: Vietnam’s middle class has been expanding steadily, supported by rising incomes and increasing consumer purchasing power. This economic shift has led to growing demand for premium and imported food products that are perceived to offer higher quality[8].

– Health and wellness: Health and wellness have become central to food consumption decisions in Vietnam. Many Vietnamese consumers are now prioritizing products that support nutritious, balanced, and health-oriented diets, especially after the COVID-19 pandemic.

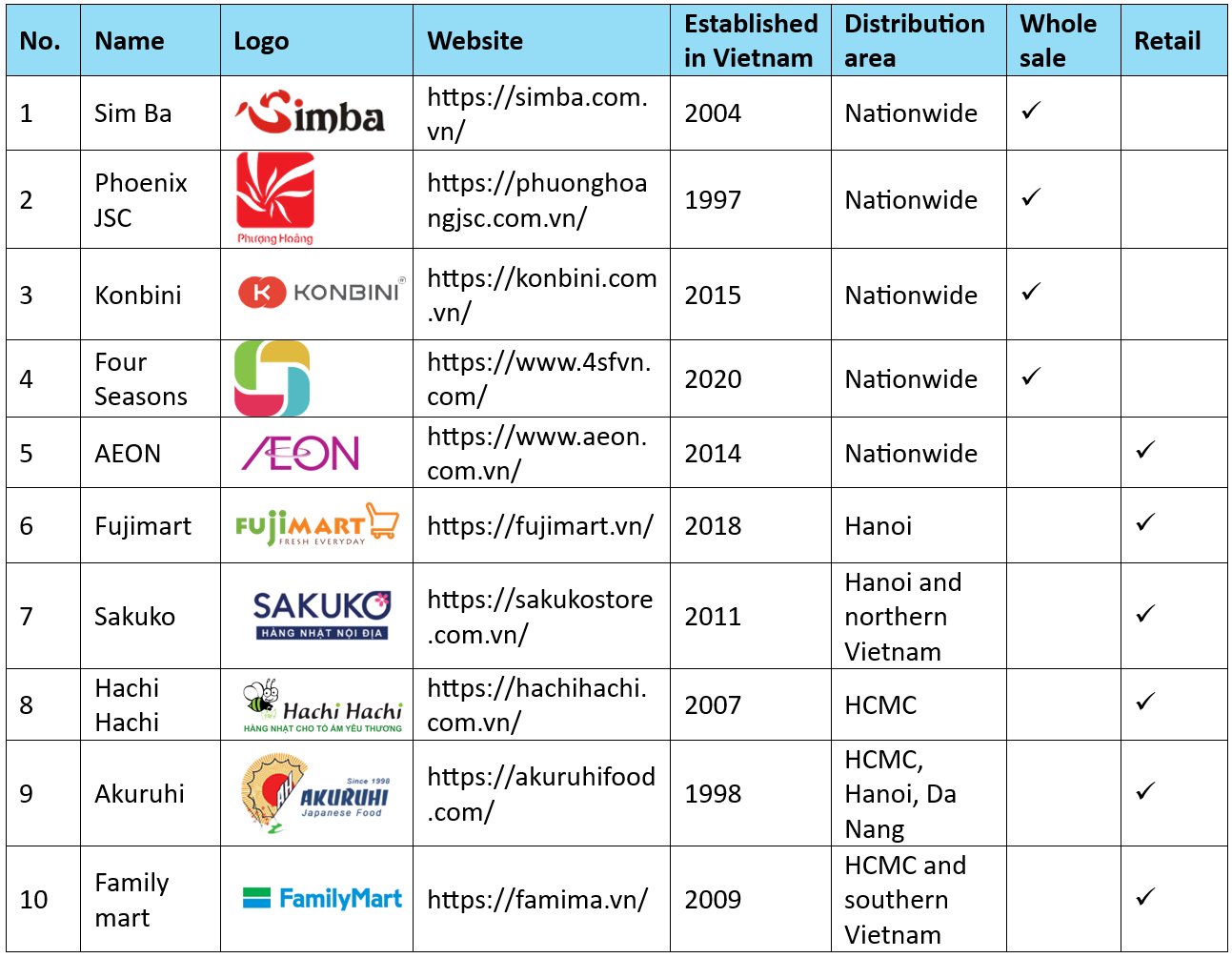

Distributors of Japanese food product

There are some distributors claiming to import and provide wholesale services for hyper supermarkets, supermarkets, specialty stores, and shops nationwide. The distribution of Japanese processed and prepared food in Vietnam is more notable in retail brands, which can also import directly from Japan. The market witnesses the active participants of Japanese-owned brands such as AEON, Fujimart, and Family Mart. Across retail formats, Japanese processed food offerings typically include packaged dry foods (such as snacks, confectionery, instant noodles, cereals, seasonings, and sauces), refrigerated and frozen items (ready meals, dumplings, processed meat and seafood), and prepared foods (bento boxes, sushi, onigiri, bakery products). Besides chains specializing in distributing Japanese products that are listed below, Japanese processed food can be found in general retail chains such as WinMart.

Some notable distributors of Japanese processed food

B&Company’s synthesis

Opportunities for selling Japanese processed food in Vietnam

Positive country image

Vietnamese people have familiarity with Japanese culture and highly perceive Japanese products as high quality. Japanese cuisine is already popular through media, sushi restaurants, ramen shops, and Japanese dining chains. The positive brand perception of “Made in Japan” provides a foundation for expanding processed food sales further.

Growth of modern retail and E-commerce

Vietnam’s retail landscape witnesses increasing penetration of supermarkets, hypermarkets, specialty stores, and convenience chains, with the active participation of Japanese chains, making Japanese products more accessible to customers. In addition, e-commerce platforms allow consumers outside major cities to access imported goods.

Trade agreements and regional integration

Vietnam’s participation in major trade agreements such as the CPTPP and RCEP strengthens economic integration with Japan. This bilateral cooperation gradually reduces tariff barriers for certain food categories. Vietnam can be considered a supportive environment for Japanese exporters seeking stable growth in Southeast Asia

Challenges in selling Japanese processed food products in Vietnam

Price sensitivity and strong competition

Vietnam’s retail market features a wide array of international food imports, such as products from China and Thailand, many of which are priced more competitively. Japanese products, although perceived as high-quality, often carry higher price points, which can limit appeal among broader consumer segments who prioritize affordability.

Limited consumer awareness

Japanese processed foods are often positioned as premium or niche products, which requires consumer education and brand-building efforts. For example, with the case of instant noodles, many Vietnamese consumers are still more familiar with traditional local products such as Hao Hao, Omachi, and Cung Dinh[9]. Korea’s instant noodles can make an impression among Vietnamese customers thanks to their spiciness, with prominent names such as SamYang and Nongshim appearing in media and hotspot restaurants.

Complex supply chain and logistical costs

Japan lacks the proximity advantage comparing to other competitors such as China, Thailand, and Indonesia, causing logistical challenges including higher shipping costs. Vietnam’s import regulations for food, particularly safety and hygiene inspections, can result in delays and increased costs, especially when documentation and standards vary across products. These challenges can make it harder to maintain competitive pricing and consistent inventory in the market.

Read more

Japanese Functional Foods in Vietnam: Overview and Market Trends

The rise of ‘officially sourced’ goods: Opportunities for B2B suppliers with VAT invoices

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 900,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 28 3910 3913 |

[1] HS Code for processed food: HS4, HS9, HS16, HS17, HS18, HS19, HS20, HS21, HS22

[2] The Saigon Times, Vietnam is becoming a major consumer market for Japanese goods (https://thesaigontimes.vn/viet-nam-dang-tro-thanh-thi-truong-tieu-thu-lon-hang-nhat/)

[3] Hanoi Times, Japanese food companies step up focus on Vietnam market (https://hanoitimes.vn/japanese-food-companies-step-up-focus-on-vietnam-market.971971.html)

[4] VnEconomy, Potential for cooperation and investment in the Vietnamese-Japanese food industry (https://vneconomy.vn/du-dia-hop-tac-dau-tu-nganh-thuc-pham-viet-nam-nhat-ban.htm)

[5] Nguoi Lao Dong, Japanese flavors attract Vietnamese consumers (https://nld.com.vn/huong-vi-nhat-ban-thu-hut-khach-viet-196250308161551786.htm)

[6] VN Express, Reasons why DHC nut ritional supplements ‘score points’ with users (https://vnexpress.net/ly-do-thuc-pham-chuc-nang-dhc-ghi-diem-voi-nguoi-dung-4887589.html)

[7] Statista, Convenience Food – Vietnam (https://www.statista.com/outlook/cmo/food/convenience-food/vietnam)

[8] PwC, Voice of Consumer 2025 (https://www.pwc.com/vn/vn/publications/vietnam-publications/voice-of-consumer-2025.html)

[9] Coc Coc Ad Platform, Decoding the packaged food purchasing habits of Vietnamese consumers (https://qc.coccoc.com/vn/news/giai-ma-thoi-quen-mua-thuc-pham-dong-goi-cua-nguoi-tieu-dung-viet)

Related article

Sidebar:

SUBSCRIBE NEWSLETTER