In 2025, the Vietnam National Assembly approved major revisions to both PIT and CIT Law, marking a significant milestone in income tax reform.

26Mar2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

As Vietnam’s economy continues to expand and deepen its integration into global markets, taxation is playing an increasingly important role not only as a source of public revenue but also as a mechanism to guide economic behavior and maintain fair competition. At the same time, the rapid development of digital business models is fundamentally changing how income is generated, reported, and managed within the economy.

Against this backdrop, Vietnam has accelerated efforts to modernize its tax system. In 2025, the National Assembly approved major revisions to both the Personal Income Tax (PIT) Law and the Corporate Income Tax (CIT) Law, marking a significant milestone in the country’s ongoing tax reform agenda. These changes are expected to have wide-ranging implications for individuals as well as for businesses operating across different sectors.

Overview

These developments form part of a broader effort to update Vietnam’s tax system, alongside adjustments to value-added tax and other related regulations.

Although the reforms include adjustments to tax thresholds and applicable rates, their broader significance lies in strengthening tax administration and improving income monitoring. In particular, the revised framework places greater emphasis on the digital economy and individual business activities, which have expanded rapidly but remain uneven in terms of compliance and reporting.

This reform is also a response to structural gaps in the current system. The rise of e-commerce, digital platforms, and freelance work has created new income streams that are not fully captured, while the large informal sector continues to create disparities in tax obligations and risks of revenue leakage.

More importantly, the reform signals a gradual transition from a system that relies heavily on self-declaration toward one that is increasingly supported by integrated data and digital monitoring. This shift aims to narrow the gap between reported and actual income, particularly in sectors where transactions are conducted through a combination of cash and digital channels, while also encouraging the transition from informal to formal business structures.

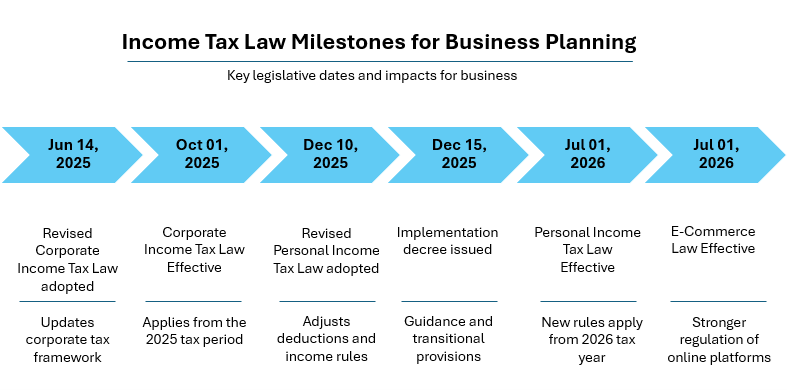

Income Tax Law milestones for business planning

Vietnam’s recent tax reforms follow a clear legislative timeline, reflecting a phased implementation approach that allows both businesses and individuals to adjust their strategies accordingly.

B&Company’s synthesis

This timeline highlights that the reforms are not implemented simultaneously but instead follow a staged process, which allows tax authorities to gradually build enforcement capacity while giving taxpayers time to adapt. adaptation.

The revised framework introduces changes across both personal and corporate taxation, primarily in thresholds, rate structures, and tax treatment.

Personal income tax thresholds are adjusted, with personal deduction increasing from VND 11 million to VND 15.5 million per month, dependent deduction from VND 4.4 million to VND 6.2 million per month, and the taxable revenue threshold for individual businesses from around VND 100 million to VND 500 million per year, along with an expanded scope of taxable income.

Personal Income Tax Deductions (Before vs. After Revision)

| Item | Previous regulation | Revised regulation |

| Personal deduction | VND 11 million/month | VND 15.5 million/month |

| Dependent deduction | VND 4.4 million/month | VND 6.2 million/month |

| Taxable revenue threshold for individual businesses | Around VND 100 million/year | VND 500 million/year |

| Scope of taxable income | Mainly traditional income sources | Expanded to include certain new asset types and income sources |

Corporate income tax structure shifts from a single standard rate of 20% to include additional revenue-based rates of 15% for businesses with revenue below VND 3 billion and 17% for those between VND 3 billion and VND 50 billion, while the 20% standard rate remains unchanged.

| Items | Previous regulation | Revised regulation |

| Preferential rates | No revenue-based tiering; standard CIT rate generally at 20% | 15% (< VND 3 billion); 17% (VND 3–50 billion) |

| Tax structure | Single standard rate | Tiered rates based on revenue |

Personal income tax and corporate income tax differ fundamentally in both structure and application, leading individuals to increasingly weigh the choice between operating as individuals or through a corporate entity. Personal income tax applies to a progressive rate system ranging from 5% to 35%, with relatively limited deductions and simpler compliance requirements, while corporate income tax applies fixed rates between 15% and 20% and allows for a broader range of deductible expenses and access to various tax incentives. At the same time, corporate structures require more formalized accounting and reporting obligations. As a result, individuals with stable or growing income streams may find the corporate model more advantageous in terms of tax efficiency and financial management, whereas those with smaller or less predictable income may prefer the simplicity of individual taxation.

Implications for the business environment

The revised tax framework is expected to reshape the business environment through both improved transparency and stricter compliance requirements. As monitoring mechanisms become more sophisticated and enforcement more predictable, businesses may face higher expectations in financial reporting and internal controls, particularly in sectors where informal practices have been prevalent.

Preferential tax rates for smaller enterprises create more favorable conditions during early growth stages, while a more transparent system may strengthen investor confidence. At the same time, stricter enforcement implies that both domestic and foreign firms will need to enhance their compliance capabilities and financial management systems.

Beyond firm-level impacts, the reform also influences broader economic behavior. As data integration reduces opportunities for underreporting, individuals are increasingly incentivized to formalize their activities. Freelancers, online sellers, and high-income earners may find corporate structures more suitable for managing taxes and finances, although this shift depends on their ability to meet higher compliance requirements.

Over time, these changes are likely to drive a gradual transition from informal to formal business operations, resulting in more consistent income reporting and a more structured and transparent economic environment.

Conclusion

Vietnam’s 2025 tax reforms represent a significant step toward a more modern, transparent, and equitable tax system. By combining tax relief measures with stronger income monitoring and support for businesses, the revised framework seeks to balance fiscal objectives with economic development goals.

In the longer term, the reforms are expected to drive a gradual shift toward formalization, contributing to a more structured and sustainable economic environment.

Read more

Vietnam Labor Market update: Regional minimum wage increase effective January 1, 2026

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 900,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 28 3910 3913 |

Related article

SUBSCRIBE NEWSLETTER