This reviews the global logistics implications of the Middle East crisis and assesses its current impact on transportation in Vietnam.

25Mar2026

Latest News & Report / Vietnam Briefing

Comments: No Comments.

Abstract

The current Middle East conflict is creating a global logistics shock through fuel volatility, route disruption, and war-risk pricing. For Vietnam, the impact is uneven but increasingly visible: domestic transport operators face higher fuel costs, while exporters, freight forwarders, airlines, and businesses linked to Gulf, Red Sea, and Mediterranean routes face deeper operational disruption. This article reviews the global logistics implications of the crisis, assesses its current impact on Vietnam, and outlines practical risk-management priorities for affected businesses.

A global crisis with logistics consequences far beyond the Middle East

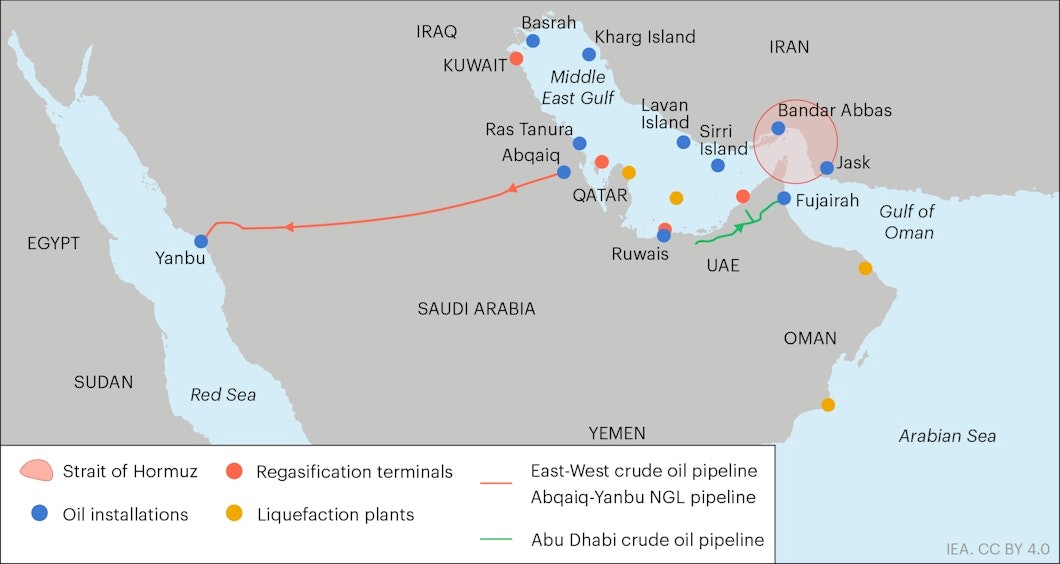

The current conflict should not be viewed only as a regional geopolitical event. From a logistics perspective, it is a global shock transmitted through three closely linked channels: higher energy prices, transport-route disruption, and risk-based pricing through war-risk insurance and emergency surcharges. The Strait of Hormuz remains central because the IEA estimates that around 20 million barrels per day of crude oil and oil products transited the strait in 2025, equal to around one quarter of the world’s seaborne oil trade, while alternative bypass capacity remains limited[1]. In practical terms, this means that any prolonged disruption in the Gulf can quickly translate into higher fuel costs and wider supply-chain instability far beyond the Middle East.

Alternative routes

Source: IEA

The impact extends across geographies, but not in the same way. In Gulf economies, the shock reaches beyond transport into sectors such as aviation, tourism, real estate, finance, and digital infrastructure. For the wider global economy, however, the first-round effect is felt most clearly in shipping, air freight, energy-intensive manufacturing, and any business reliant on stable Asia–Europe or Asia–Middle East corridors. VnEconomy, citing Vietnam Logistics Business Association representatives, describes the current episode as unusually severe because it simultaneously affects the Strait of Hormuz, the Persian Gulf, and the Red Sea/Suez corridor.

Major carriers have already translated this geopolitical risk into operational changes. Maersk paused future Trans-Suez sailings on key services and rerouted them around the Cape of Good Hope[2], while Hapag-Lloyd also shifted selected sailings away from the Trans-Suez corridor under Red Sea constraints[3]. DHL notes that such diversions can add roughly 20–50% to transit times, or around 7–10 extra days into Europe and 10–14 days into the Mediterranean from Asia[4]. In practical terms, a security shock becomes “logistics math”: longer voyages, higher bunker consumption, tighter vessel capacity, less predictable schedules, and more inventory tied up in transit.

Current impact on Vietnam logistics and transportation: uneven, but increasingly visible

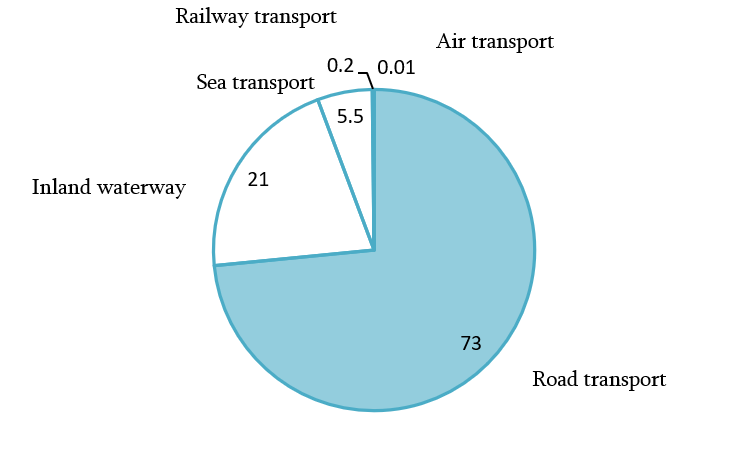

Vietnam is structurally exposed to this kind of external shock, although the degree of exposure varies across the sector. Logistics costs remain high at around 16.5–17% of GDP, road freight still accounts for over 70% of domestic cargo volume, and more than 90% of logistics firms are SMEs[5], limiting their ability to absorb sudden increases in fuel, insurance, and transport costs. As a result, even firms with no direct exposure to Middle East routes can face margin pressure through higher diesel costs and more expensive domestic distribution.

Structure of freight transportation modes in Vietnam (Q1 2025)

Unit: % ; 100% = 715.8 million tonnes

Source: General Statistics Office of Vietnam

At the same time, the impact is not uniform across the industry. According to VLA’s recent survey results, 89.8% of Vietnamese logistics firms have been affected to some degree[6], while only 10.2% remain largely unaffected, mainly domestic operators or firms with limited exposure to the affected shipping lanes. In practice, the scale and nature of the impact depend largely on route exposure and business model:

For domestic transport and logistics providers, the main effect is cost inflation rather than route disruption. Trucking, last-mile delivery, and warehousing are not directly exposed to global rerouting decisions, but they remain highly sensitive to diesel prices. As a result, responses have been largely defensive, including fuel surcharges, quotation revisions, tighter dispatch planning, and efforts to reduce empty mileage. In rail, this cost pass-through has become more explicit: Railway Transport Joint Stock Company raised passenger fares by 10% and freight rates by 15% in early March[7], showing how operators are increasingly aligning tariffs with fuel volatility rather than absorbing the pressure internally.

For exporters, freight forwarders, and maritime logistics firms not directly serving Middle East, Persian Gulf, or Mediterranean routes, the impact is indirect but still significant. They are affected mainly by higher fuel and insurance costs, weaker schedule reliability, tighter vessel capacity, and wider network congestion. Spillover effects are already visible: some export shipments from Ho Chi Minh City have reportedly been delayed by 7–10 days as shipping lines revised services and added surcharges[8]. For these firms, the main challenge is rising logistics costs and lower delivery predictability rather than direct route disruption.

The disruption is more severe for Vietnamese firms directly linked to the Middle East, Persian Gulf, and Mediterranean routes. In these cases, the problem is not only higher costs but also the limited ability of local businesses to influence upstream decisions made by global carriers, insurers, and international shipping networks. VnEconomy, citing the VLA, described the Middle East route as being in a state of “partial paralysis” in some segments, while the Europe-facing side has been affected by rerouting around the Cape of Good Hope, adding roughly 10–14 days each way. The same report cited Phaata data showing that freight from Ho Chi Minh City to Northern Europe rose 9% month on month, while freight to Dubai surged 388%, with some shipping lines suspending Middle East bookings altogether. In such cases, Vietnamese firms have limited room to respond beyond renegotiating delivery terms, absorbing extra storage and transshipment costs, switching markets, or postponing shipments.

For manufacturers and exporters, these logistics disruptions quickly become production and commercial risks. Longer transit times, container imbalances, and less reliable shipping schedules make inventory planning harder and increase the likelihood of missed delivery windows, especially in sectors with seasonal orders, cold-chain requirements, or time-sensitive export commitments. Ho Chi Minh City authorities have already warned that at least eight major manufacturing and export sectors are being affected to varying degrees, with electronics, textiles, and footwear among the most exposed because of their dependence on global supply chains and delivery schedules.[9]

For airlines and air cargo, the exposure is the most acute because both fuel prices and fuel availability are under pressure. Rising Jet A1 prices are increasing airline costs, while warnings of possible shortages from early April raise the risk of flight cuts and tighter cargo capacity[10]. This is particularly critical for time-sensitive shipments on routes linking Vietnam with Europe, North America, and the Middle East through Gulf hubs.

The Government’s response has focused on limiting the speed at which the external shock feeds into domestic business disruption. Vietnam established a national energy-security task force, proposed activation of petroleum price-stabilization measures if retail prices rise by 20% or more within a month, and temporarily cut import tariffs on several fuel products, including diesel and aviation fuel, to 0% through April 30. Sector-specific guidance has also been issued: maritime authorities told shipowners and shipping firms to monitor international warnings and prepare alternative routing plans, while the Ministry of Industry and Trade urged import-export and logistics firms to diversify markets, supply sources, and transport options.[11] [12] [13] [14]

Risk-management implications for affected logistics businesses

For logistics businesses in Vietnam, the first priority is clearer risk identification and segmentation. The current Middle East conflict is not affecting all operators in the same way; therefore, responses need to reflect actual exposure rather than broad sector labels. Domestic transport providers are primarily exposed to fuel-cost inflation, while freight forwarders and carriers involved in international routes face additional pressure from insurance surcharges, schedule disruption, rerouting, and booking uncertainty. For higher-tier logistics service providers such as 3PL, 4PL, and 5PL firms, the key challenge lies in maintaining service reliability and coordinating alternatives across increasingly volatile transport networks.

The second priority is stronger operational risk management. This requires tighter contract discipline, particularly in relation to fuel-adjustment clauses, surcharge pass-through terms, insurance responsibilities, force-majeure provisions, and delivery obligations. At the same time, logistics firms need more adaptive planning practices, including closer coordination with carriers and overseas partners, more frequent route reassessment, and clearer contingency plans for delays, rerouting, and sudden cost escalation. In the current environment, resilience depends not only on contractual protection but also on the ability to respond quickly as conditions change.[15]

The third priority is selective strategic adaptation. The crisis does not create a broad-based growth opportunity for Vietnam’s logistics industry as a whole, but it does strengthen demand for a narrower set of services that help customers manage uncertainty more effectively. These include warehousing near ports and industrial zones, multimodal coordination, visibility tools, and digital transport-management systems. As B&Company’s recent market analysis suggests, these resilience-oriented capabilities are gaining traction mainly among larger and more technology-capable operators, rather than across the market as a whole.[16] [17]

Conclusion

The Middle East conflict is best understood not as a distant geopolitical event, but as a global logistics shock with uneven yet increasingly visible effects on Vietnam. The businesses most exposed are those linked to Gulf, Red Sea, and Mediterranean routes, together with airlines, air-cargo operators, exporters, and manufacturers dependent on timely international transport. Domestic transport operators are affected more indirectly, mainly through fuel inflation and tighter margins. For Vietnam, the central business message is therefore the need for clearer route-based risk management, stronger contract discipline, and more selective investment in resilience where it can genuinely reduce exposure and protect service reliability.

Read more

* If you wish to quote any information from this article, please kindly cite the source along with the link to the original article to respect copyright.

| B&Company

The first Japanese company specializing in market research in Vietnam since 2008. We provide a wide range of services including industry reports, industry interviews, consumer surveys, business matching. Additionally, we have recently developed a database of over 900,000 companies in Vietnam, which can be used to search for partners and analyze the market. Please do not hesitate to contact us if you have any queries. info@b-company.jp + (84) 28 3910 3913 |

[1] IEA (2026): Strait of Hormuz Factsheet <Access>

[2] Maersk (2026): Rerouting of ME11 and MECL Service around The Cape of Good Hope <Access>

[3] Hapag-Lloyd (2026): Update on Red Sea Transit and Temporary Route Adjustments <Access>

[4] DHL (2024): Red Sea Situation & Impact on Global Shipping <Access>

[5] Vietnam Logistics Association (VLA), Vietnam Logistics Report 2024 <Access>

[6] Among affected firms, 38.8% reported mainly margin pressure, 34.7% reported operational disruption and revenue decline, and 16.3% described the situation as especially severe, with a risk of business stagnation.

[7] LaoDong (2026): Railways increase ticket prices by 5% starting March 21st <Access>

[8] VnEconomy (2026): HCMC exports face 7-10 day delays and shipping surcharges amid Middle East conflict <Access>

[9] VnEconomy (2026): HCMC exports face 7-10 day delays and shipping surcharges amid Middle East conflict <Access>

[10] Tuoi Tre (2026): Vietnamese airlines and the pressure to cut operations <Access>

[11] VietnamPlus (2026): Vietnam forms task force to ensure energy security amid Middle East tensions <Access>

[12] VietnamPlus (2026): Vietnam takes urgent measures to ensure energy security amid Middle East conflict <Access>

[13] Government News (2026): Implement fuel price management in accordance with Government Resolution No. 36/NQ-CP. <Access>

[14] VietnamPlus (2026): Import tariffs on certain fuel products reduced to 0% <Access>

[15] VnEconomy (2026): Import-export and logistics firms advised to take proactive measures amid Middle East tensions <Access>

[16] B&Company (2025): Current application of domestic TMS, GPS tracking and AI in optimizing road transport routing in Vietnam <Access>

[17] B&Company (2025): Challenges and opportunities in Vietnam’s Logistics sector for foreign investors <Access>

Related article

Sidebar:

SUBSCRIBE NEWSLETTER